Weekly Roundup #1

Housing | Week of 9.15 - 9.21

Welcome to the first edition of Boyd’s weekly roundup. Here we will be running community polls, recapping the trailing week’s activities at Boyd, sharing relevant newsflow and research/analysis links, highlighting key charts and datapoints, and previewing the upcoming week’s agenda. Expect to receive these roundups in your inbox each Saturday morning moving forward.

The past week+ has been active at Boyd as we’ve turned the page on Drones & Autonomy and gotten started in earnest on this quarter’s sprint: Housing. A couple noteworthy things to call attention to:

We’re hosting an essay contest! Contest opens September 15th. Prompt: “What’s an actionable, outside-the-box solution to America’s housing crisis?”

We’ve brought on William Miller, a Substack-native with a background in financial markets and research, and a strong interest in tackling core issues that face the next generation of Americans.

So it’s an exciting time at Boyd. We’re turning it up a notch — leveraging the Substack network in doing so — in service of our mission to discover bold, asymmetric solutions to complex problems.

Community Poll

News/Media Links

Mortgage rates drop again, hitting 11-month low — Yahoo Finance

“Lower mortgage rates have drawn more borrowers to apply for loans. According to the Mortgage Bankers Association, applications to purchase a home jumped 7% from a week earlier and were 23% higher year-over-year. Refinance applications increased 12% from the previous week and were 34% higher than a year ago. ‘The downward rate movement spurred the strongest week of borrower demand since 2022, with both purchase and refinance applications moving higher,’ Joel Kan, MBA’s vice president and deputy chief economist, said in a statement.”

***

The right way to look at the housing crisis — Washington Post Opinion

“The ‘Yes in My Backyard’ movement, also known as YIMBY, which works to change zoning laws to increase housing, risks turning owned homes into perpetual rentals. That would benefit only real estate developers at the cost of community stability.

[…]

This is not simply a California story; it is a national one shaped by declining fertility, slower immigration and generational turnover. Sound housing policy should reflect that nuance and enable ownership through solutions such as tax credits, mortgage rate buydowns with subsidies, down payment support and starter home protections — not by building more houses.”

***

Even New York City's Wealthy Renters Can't Avoid the Housing Crisis — Bloomberg Wealth

“At least 65,000 households making between $100,000 and $300,000 a year pay a third or more of their gross income to landlords, according to NYC Housing and Vacancy Survey estimates. That’s tens of thousands more than just four years ago.”

***

Controversial bill that adds dense housing to transit stops passed by Assembly — LA Times

“The bill was introduced in March by Sen. Scott Wiener (D-San Francisco), who stresses that the state needs to take immediate action to address California’s housing shortage. It paves the way for taller, denser housing near transit corridors such as bus stops and train stations: up to nine stories for buildings adjacent to certain transit stops, seven stories for buildings within a quarter-mile, and six stories for buildings within a half-mile.

[…]

The bill has spurred multiple protests in Southern California communities, including Pacific Palisades and San Diego. Residents fear the zoning changes would alter single-family communities and force residents into competition with developers, who would be incentivized under the new rules to purchase properties near transit corridors.”

Research/Analysis Links

Immigration and House Prices in the UK by Filipa Sá (2011)

“Using data on immigration and house prices for 159 local authorities in England and Wales, I find that immigration has a negative effect on house prices. An in-flow of immigrants equal to 1% of the local population reduces house prices by 1.6%. A simple theoretical model and my empirical estimates on native population growth and mobility suggest that one explanation for this negative effect is the mobility response of natives. The estimates show that an immigrant in-flow equal to 1% of the local population leads to a native out-flow equal to 0.849% of the local population and increases the native out-migration rate by 0.132 percentage points.”

***

Bringing the Housing Shortage into Sharper Focus

“Our analysis also suggests that policymakers should focus more of their attention on the supply of housing in modest- and middle-income communities, where the shortfalls are most prevalent and tend to be deepest. With subsidies already providing some support for housing in low-income communities and the market in most places adequately serving upper-income communities, those in between are falling through the cracks.”

***

New Apartment Construction Tops 500K Units This Year, More Than Half in 1 Region

“Southern metros typically offer streamlined approval processes and fewer regulatory hurdles, making it easier to bring multifamily projects to market. At the same time, elevated home prices and a shortage of attainable for-sale housing are pushing more residents toward rentals. For many households, single-family (housing) ownership is simply out of reach — fueling demand for rental housing.”

Charts/Graphs

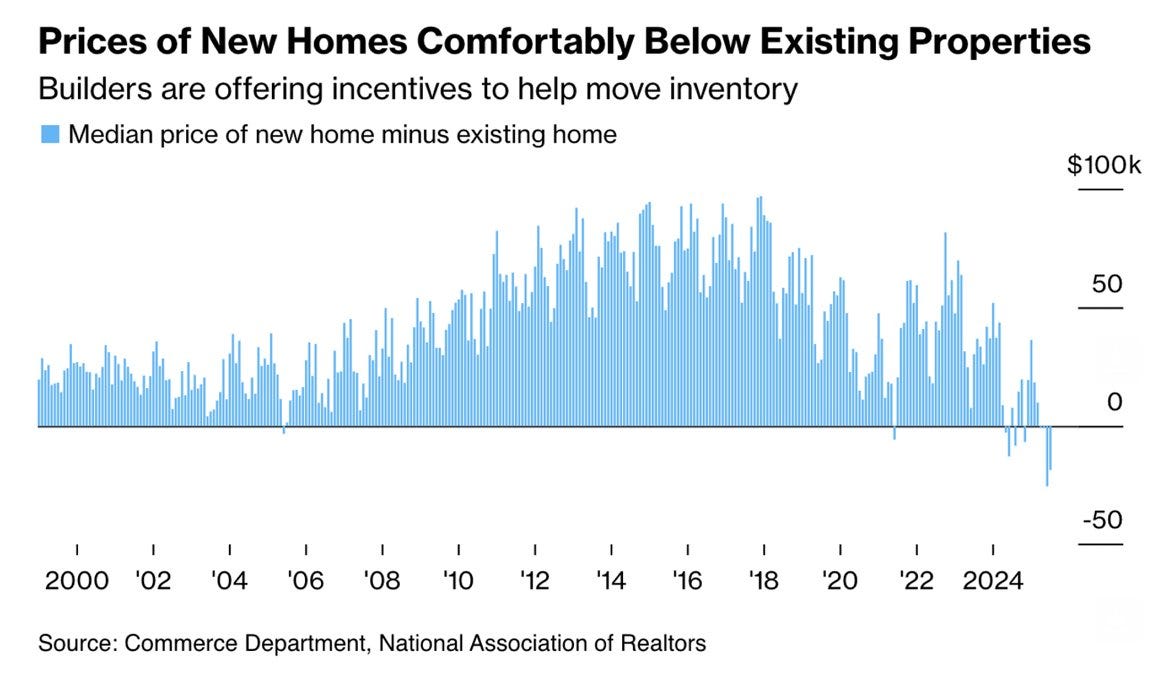

We're likely seeing the impact of "rate-locked" housing supply, whereby would-be sellers locked in to ZIRP-era mortgage rates are reluctant to list their homes or are even de-listing in lieu of decreasing the asking price — while on the other hand, newly-constructed homes are listed immediately and exchange hands at the market price.

Additionally, there’s likely a selection bias: when homeowners with ZIRP mortgages don’t sell, the existing-for-sale pool isn’t representative. The homes that do turn up for sale today are likely more often:

Larger, recently renovated, or located in higher-value neighborhoods (owners who move are often trading up or relocating for well-paid jobs); and/or

Belonging to cohorts unconcerned with mortgage rates (wealthier sellers with cash or very low remaining balances).

A very curious phenomenon, which could certainly also be explained in part by builder incentives and effective discounting, new builds being pushed to cheaper land, and quality/amenity/value drift in the existing stock as many existing houses sold now have been upgraded over the previous decade (and those improvements are capitalized into prices):

***

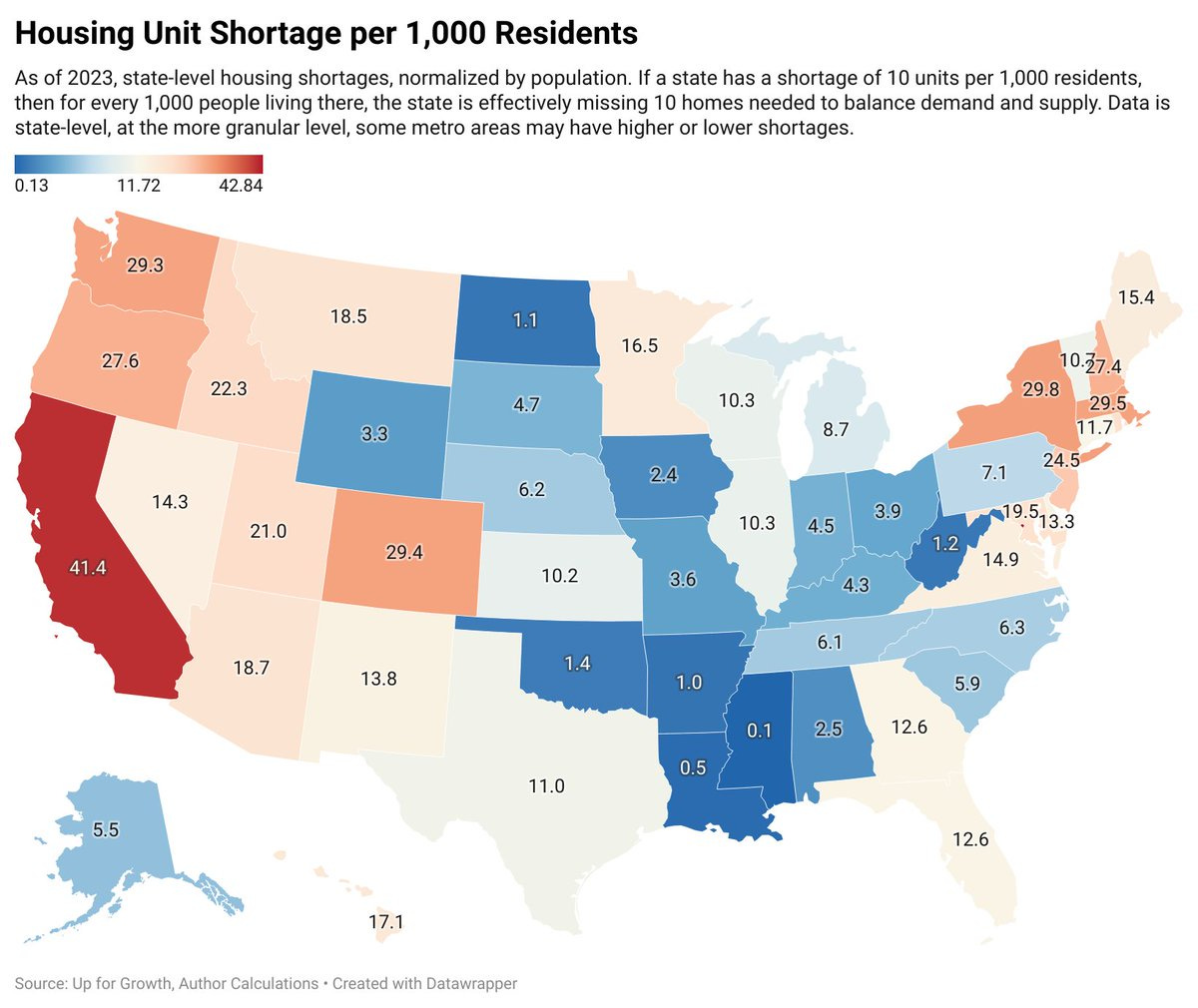

This map of the estimated housing unit shortage by state, in absolute terms, had to be done in natural log form so as to accomodate the gulf between California’s shortage and the rest of the states’.

Here’s the same chart with a linear scale:

And then here’s the housing unit shortage on a per-capita basis:

When considering intra-US population flows, it really is remarkable, the extent to which California and New York — both of which have seen significant population outflows — are nevertheless facing a housing supply crisis:

Agenda for the Upcoming Week

he root of our housing crisis isn’t zoning, interest rates, or immigration. It’s a distorted view of equity—and by extension, of what counts as “real” housing.

In America equity is treated as valid only when tied to a suburban three-bedroom, two-bath home. That model is already in place with Habitat and other organizations. It works for families. It even works for multi-generational households. But it fails the far larger group: singles and couples who need an affordable foothold.

The answer is starter-scale equity. Think small units—even kitchenette-style spaces—recognized as legitimate investments. Equity shouldn’t require a mortgage-sized leap.

A co-op framework can make this work. Residents buy in, maintain their unit and community, and sell their share back to the co-op when they move on. They carry forward their equity to the next step.

This reframes ownership: equity as a ladder, not a leap. It opens the door that the suburban model keeps locked.

Yes, zoning and finance matter. But the bigger barrier is mindset—the idea that only a house with a yard builds “real” wealth. Until we challenge that assumption, millions will remain shut out of ownership.

My vote for the root cause of the housing affordability crisis is monetary policy. Zoning and regulatory hurdles aid and abet the housing distortions. Housing as an asset market enables corruptions. Tax policy is complicit. Quality land is a finite asset. Housing is unaffordable because of the way we treat land (the economic and political rules of the property game). Our current methods to incentivize affordable housing reward the rich with even more spoils—how generous!

Monetary policy is the root cause—an exploding monetary base and finite land. Monetary policy is the root cause—cheap credit to stimulate borrowing which favors asset owners over wage earners (the spoils of productivity). Monetary policy is the game that sets the monopoly board in motion. Once all the squares on the board are owned by rent-seekers, earning your inflation-adjusted $200 each time you pass go is barely enough to keep you in the game as rent-to-income ratios squeeze higher. Good luck accumulating the capital from wages to earn the down payment necessary to buy back the land from the landlord.

Landlord is a funny word dating back to at least the 14th century. Monetary policy…