Austerity, Done Right

How (and when) you cut matters more than how much

Governments facing large budget deficits eventually confront a difficult question: how can public finances be restored without causing severe economic damage? The conventional Keynesian answer is straightforward. Fiscal consolidation, whether achieved through spending cuts or tax increases, reduces aggregate demand and slows economic activity, especially when the economy is operating below capacity. From this perspective, austerity is inherently contractionary, and attempts to reduce deficits during periods of weak growth risk deepening recessions and increasing unemployment.

Over the past three decades, however, a competing body of research has challenged this conclusion. Associated most prominently with Alberto Alesina and his collaborators, this literature argues that the economic effects of fiscal adjustment depend not only on its size but also on its composition. Spending-based consolidations, it contends, are generally less damaging to growth than tax-based consolidations and, under certain conditions, may even coincide with economic expansion. Fiscal policy affects the economy not only through its immediate impact on aggregate demand but also through expectations, investment decisions, and perceptions of future tax burdens.

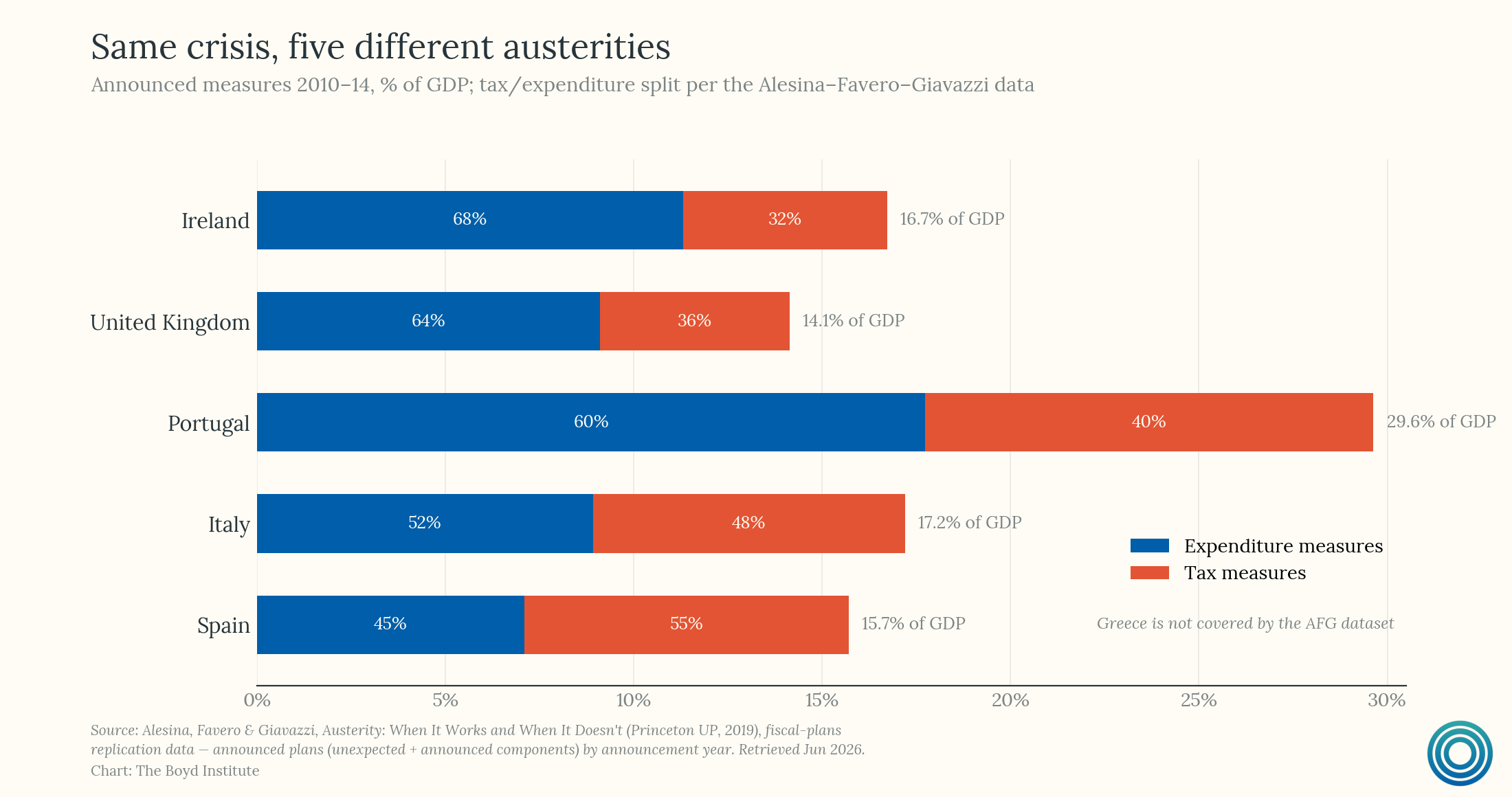

In Austerity: When It Works and When It Doesn’t, Alberto Alesina, Carlo Favero, and Francesco Giavazzi present the most comprehensive defense of this argument. Drawing on roughly 200 multi-year fiscal consolidation plans implemented across sixteen OECD countries between the late 1970s and 2014, they conclude that expenditure-based adjustments consistently outperform tax-based consolidations in both preserving economic growth and restoring fiscal stability. Their findings challenge one of the central assumptions of modern Keynesian macroeconomics: that spending cuts necessarily impose larger economic costs than tax increases.

The argument remains deeply contested. Critics have questioned the authors’ identification strategy, the role of monetary policy in successful consolidation episodes, and the size of the fiscal multipliers underlying their conclusions. Research following the eurozone debt crisis has suggested that austerity may be considerably more costly during recessions than earlier estimates implied. The debate is therefore not simply about whether austerity works. It concerns the mechanisms through which fiscal policy affects economic activity, the conditions under which fiscal adjustment succeeds, and the trade-offs governments face when attempting to restore fiscal balance.

This article evaluates those competing claims. It examines the Keynesian case against austerity, the evidence on fiscal multipliers, the historical episodes that underpin the expansionary-austerity literature, and the experience of the eurozone debt crisis. While the evidence suggests that spending-based consolidations are often less damaging than tax-based ones, outcomes depend heavily on monetary conditions, the credibility of the adjustment plan, and the specific categories of spending being reduced. Fiscal consolidation is not simply a question of how much governments cut. It also depends on what they cut, when they cut it, and under what economic circumstances.

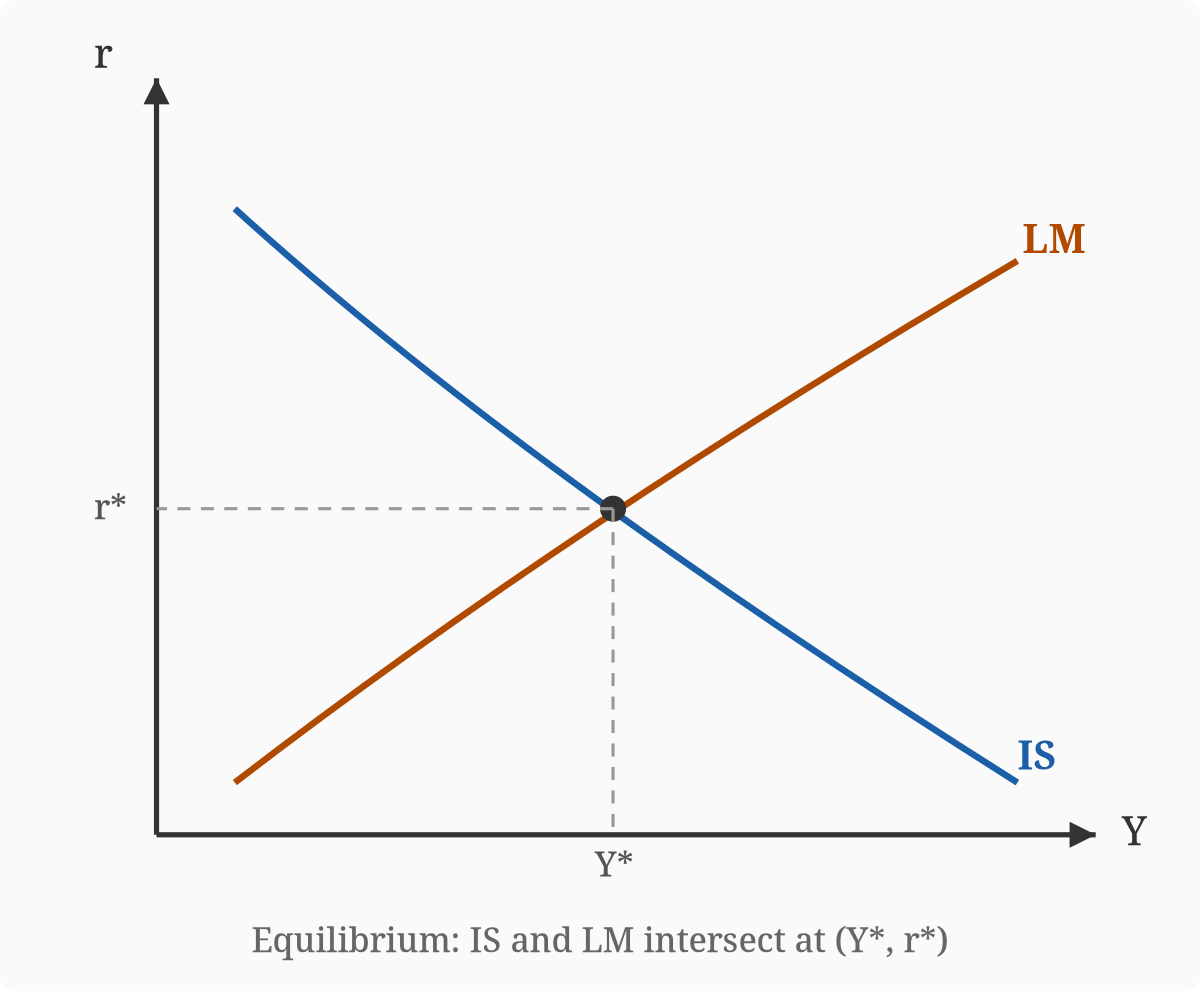

The IS-LM Model

To understand why austerity is so contested, it helps to begin with the theoretical framework that has shaped macroeconomic thinking on fiscal policy for nearly a century. The IS-LM model, developed by John Hicks in 1937 as a formalization of Keynes’s General Theory, maps the relationship between interest rates and real output across two equilibria: the goods market (the IS curve) and the money market (the LM curve).

From this framework flow three conclusions that form the backbone of the Keynesian case against austerity.

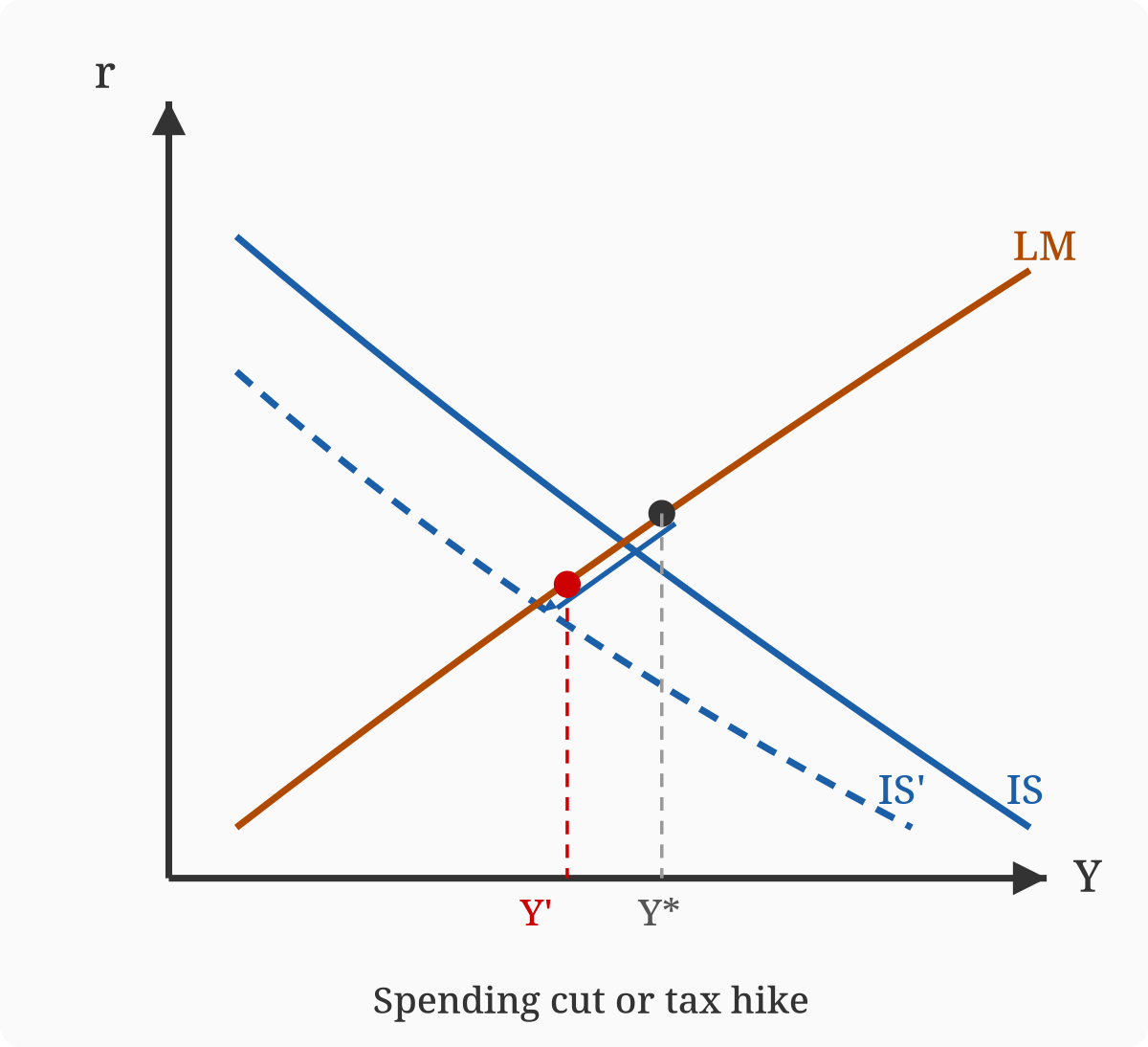

The first is that fiscal contraction shrinks output. When the government cuts spending or raises taxes, it withdraws demand from the economy. Firms sell less, hire less, and invest less. The IS curve shifts left, reducing equilibrium GDP.1

The second is that spending cuts reduce output and employment more than tax hikes. A cut in government spending directly removes demand from the economy, dollar for dollar; the government simply stops buying goods and services, and GDP falls by the full amount before any multiplier effects. A tax increase is one step removed: the government raises taxes, households have less disposable income, and they reduce consumption by the amount of the tax increase multiplied by the marginal propensity to consume (MPC). This response reflects primarily an income effect: households feel poorer because their after-tax income has fallen, so they reduce spending. There may also be a wealth effect, since higher taxes can lower the present value of households’ future resources and make them feel less financially secure, further discouraging consumption. However, because households save some fraction of their income rather than spending it all, a one-dollar tax increase reduces consumption by something less than one dollar. The tax multiplier is therefore smaller in absolute value than the spending multiplier. In the textbook Keynesian model, if the MPC is 0.8, the spending multiplier is 5 and the tax multiplier is 4. This distinction is central to the austerity debate: both instruments are contractionary, but a government that must close a given deficit gap by some combination of the two will do less short-run damage by raising taxes than by cutting spending by the same amount.

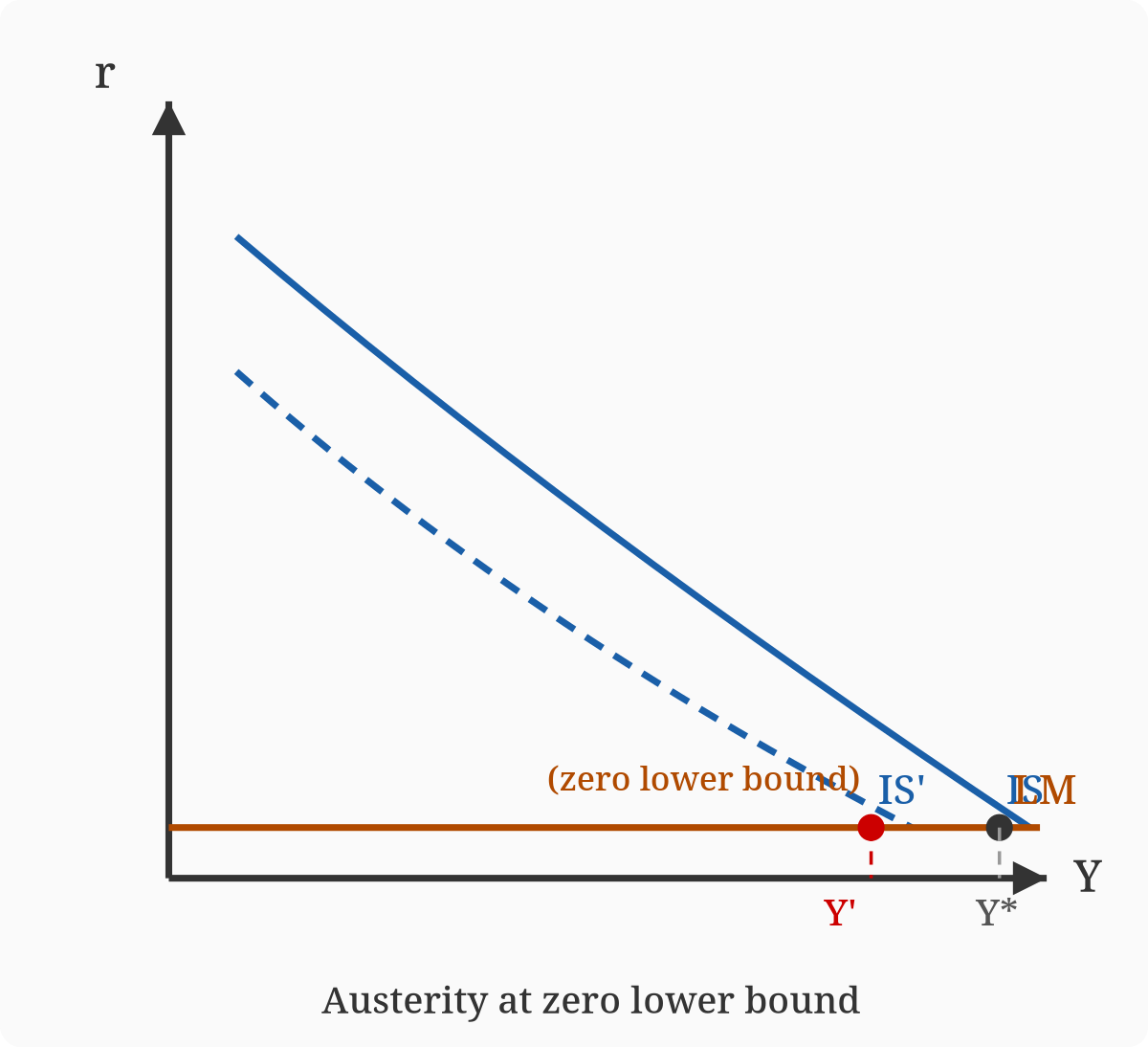

The third conclusion is that fiscal contraction is especially severe during recessions. When the economy is already operating below potential and interest rates are near zero, monetary policy loses traction: the central bank cannot meaningfully offset fiscal drag by cutting rates further.2 Austerity applied at the trough of a business cycle therefore bears much of its contractionary weight without the same countervailing force that conventional monetary easing might provide in normal times.

These conclusions are internally coherent, but the IS-LM model rests on assumptions that do not always hold. It treats expectations as largely static, overlooking the possibility that credible fiscal consolidation can boost consumer and investor confidence, lower sovereign risk premiums, and crowd in private investment. It also assumes that government spending multipliers are consistently positive and large, an assumption that a substantial empirical literature has called into question. Finally, the model is largely silent on the composition of fiscal adjustment: whether deficits are reduced through tax increases or spending cuts. It is precisely this omission that Alesina, Favero, and Giavazzi seek to address.

Multiplier Madness

Central to every argument about fiscal policy is the size of the fiscal multiplier: the change in output produced by a one-unit change in government spending or taxation.

The Keynesian Model

In the simple Keynesian model, this number is unambiguously greater than one. A dollar of government spending enters the economy, is earned as income, a fraction of which is saved and the remainder spent again, generating a cascade of demand that exceeds the original injection.

Keynesian theory draws a sharp distinction between the spending multiplier and the tax multiplier, and the difference has direct consequences for austerity policy. The government spending multiplier works through a direct injection: when the government spends a dollar, that dollar becomes someone’s income immediately. With a marginal propensity to consume of 0.8, the recipient spends 80 cents, which becomes someone else’s income, 64 cents of which gets spent, and so on. The total increase in output is 1 / (1 - MPC), or 5 in this example.

The tax multiplier, alternatively, operates indirectly. A one-dollar tax cut raises household disposable income by one dollar, but households save some portion of it; if MPC is 0.8, they spend 80 cents, and the multiplier chain proceeds from there. The tax multiplier is thus MPC / (1 - MPC), or 4 with the same assumptions. A tax increase of $1 billion therefore shrinks output by $4 billion in this model, while a $1 billion spending cut shrinks it by $5 billion. This gap is the theoretical basis for the claim that spending cuts are the more destructive form of austerity, dollar for dollar.

In practice, the gap between the two multipliers has important policy implications. If a government needs to close a $100 billion fiscal gap, it can do so through spending cuts, tax increases, or a blend. The simple Keynesian model says tax increases inflict less short-run output damage per dollar of deficit reduction. Alesina and his co-authors do not dispute this arithmetic but argue that the model misses the longer-run dynamics: tax increases suppress private investment and business formation in ways that compound over years, while spending cuts, if credible and well-targeted, can actually improve confidence and crowd in private activity.

The debate is therefore not solely about the magnitude of the multipliers but about their persistence and about the channels through which fiscal policy affects business expectations.

The More Recent Literature

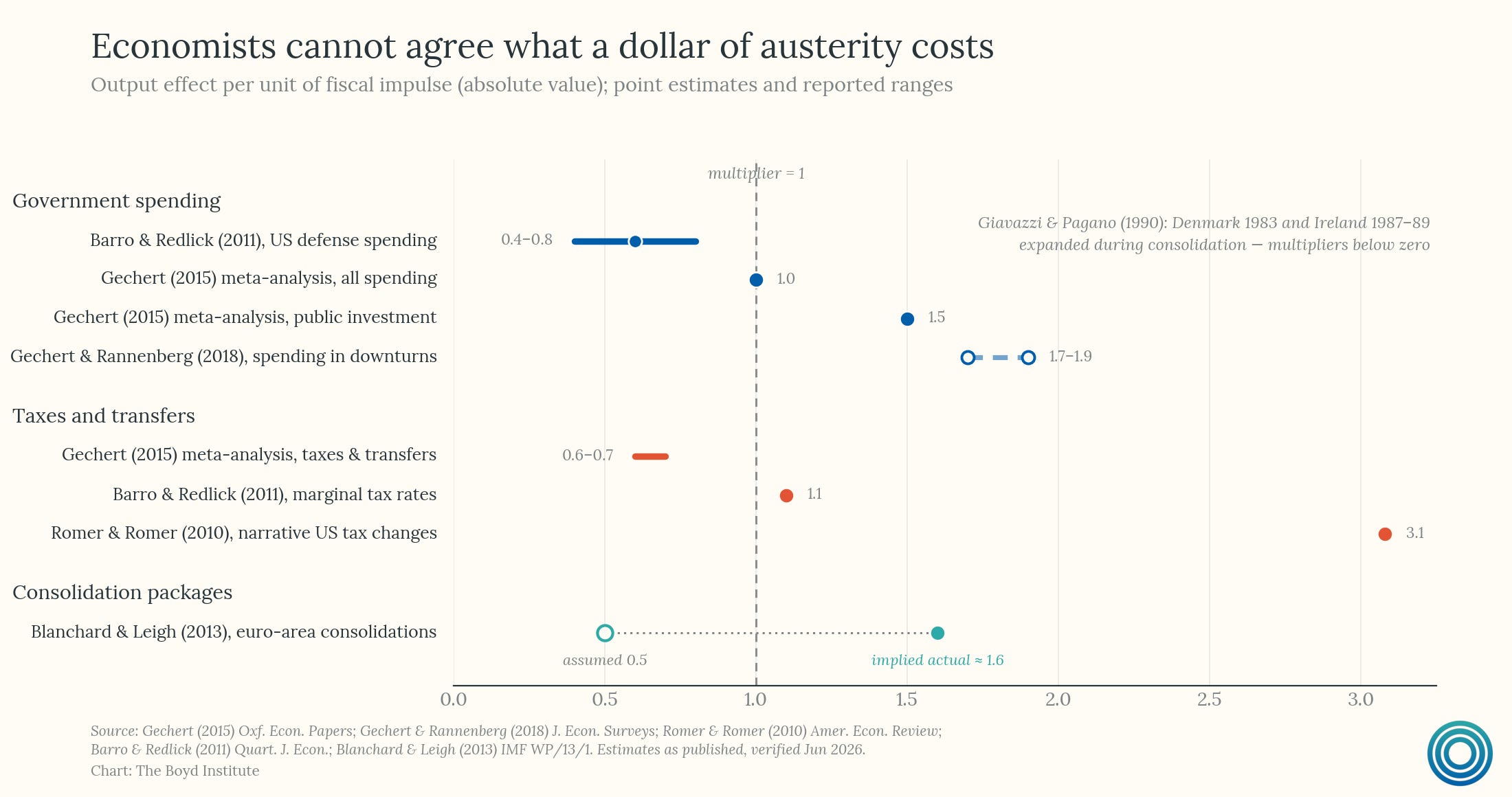

Empirical research over the past three decades has told a far messier story. Estimates of the fiscal multiplier vary so widely across studies and economic contexts that extracting a reliable consensus figure is essentially impossible.3

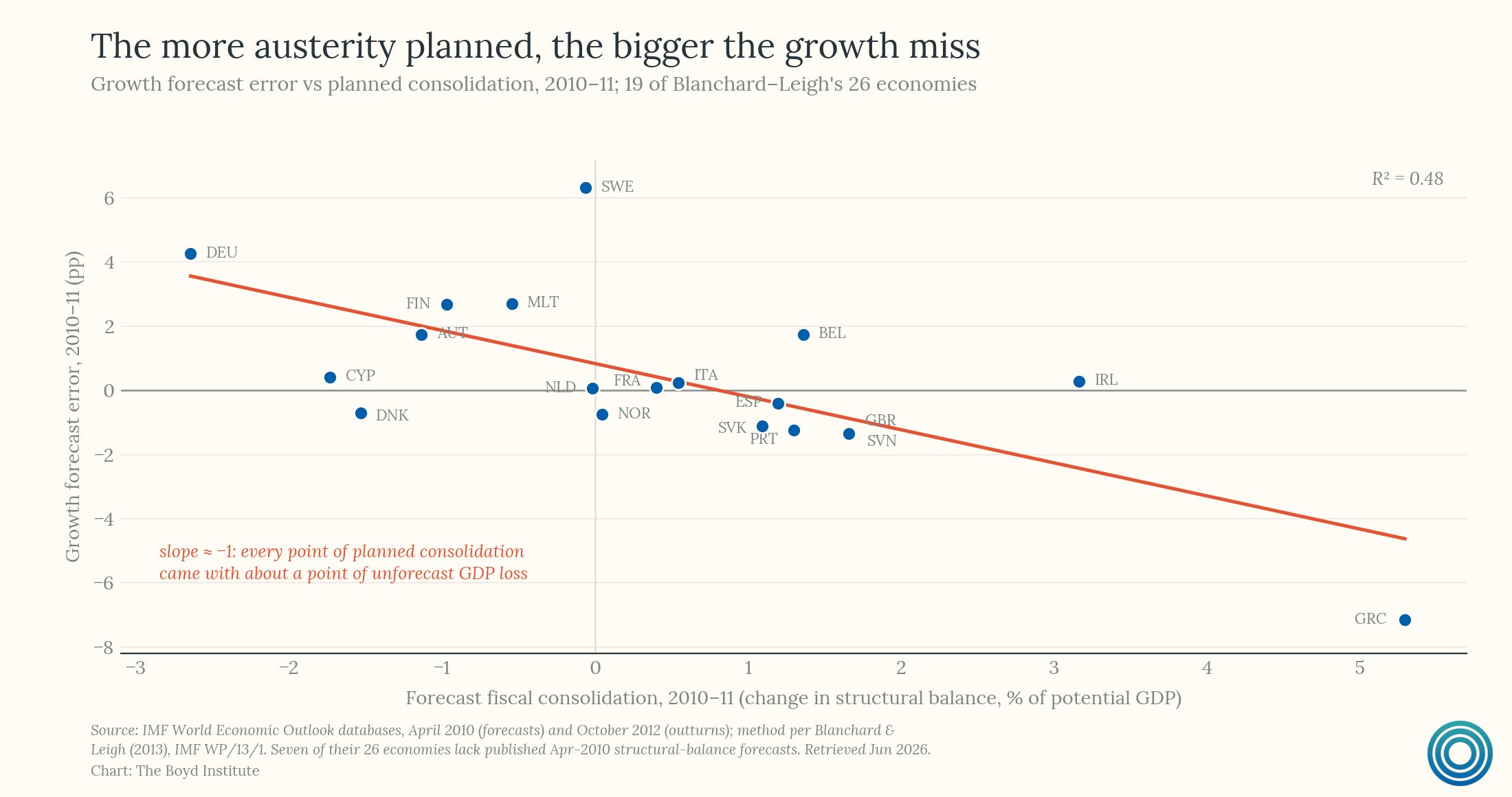

The disagreement is partly methodological. Identifying the multiplier requires isolating changes in fiscal policy that are genuinely exogenous, not driven by the state of the economy itself, and this is exceedingly difficult. Governments typically cut spending during booms and expand it during recessions, which means a naive regression of output growth on spending changes will underestimate the multiplier, since high spending is observed alongside weak output. Different studies correct for this problem in different ways, using instrumental variables, narrative records of policy decisions, or structural VAR models, and arrive at different answers. The IMF’s 2010 World Economic Outlook used one approach and found multipliers of around 0.5; a follow-up paper by Olivier Blanchard and Daniel Leigh, examining the same consolidation episodes, found that the IMF’s models had systematically underestimated the multiplier during the post-2008 period, with true values closer to 1.5.

The difference was not trivial: it implied that the austerity programs applied across Europe in the early 2010s had done roughly three times as much economic damage as the institutions overseeing them had projected.4

But the disagreement is also substantive. The multiplier appears to vary significantly with economic conditions: larger when the economy is in recession than at full employment, larger when interest rates are at the zero lower bound5, larger in closed economies than open ones, and larger for direct government consumption than for transfers or tax cuts.

These differences matter enormously for policy, because they mean that a multiplier estimated from one context may not generalize to another. The Keynesian case that fiscal policy is reliably stimulative in downturns is better supported than the crude version that multipliers are uniformly large and stable. But the corollary — that spending cuts in a depressed economy are reliably catastrophic — is also too strong. The experience of the 1990s in particular generated a set of counterexamples that the simple model struggles to accommodate.

What the multiplier debate also leaves out is any account of the long-run fiscal trajectory. A government that sustains primary deficits for long enough will eventually face a reckoning, through rising interest costs, loss of market access, or some form of forced (and often ill-timed) adjustment. In that context, the relevant counterfactual to austerity is not indefinitely sustained stimulus but eventual, possibly disorderly, consolidation under less favorable conditions. The expected cost of postponing adjustment must be weighed against the certain cost of undertaking it now, and the multiplier literature, focused as it is on short-run output dynamics, has relatively little to say about how that calculation should be made.

The empirical debate over multiplier size is, in this sense, somewhat beside the point: even a large multiplier does not tell you whether to consolidate, only what it will cost in the short run. The historical cases of countries that consolidated successfully, and some that did so while growing, are therefore where the real analytical weight lies.

Expansionary Austerity

The cases that most sharply challenge the Keynesian framework are those in which fiscal consolidation was followed not by recession but by acceleration, episodes where the contractionary arithmetic of the IS-LM model simply failed to materialize. The historical record contains enough such cases that they cannot be dismissed as flukes, even if each one can be contested on its own terms.

Denmark

Denmark in the mid-1980s offers one of the earliest and clearest examples. Facing a large current account deficit and rising public debt, the Danish government implemented a multi-year consolidation plan beginning in 1983 that combined spending restraint with a currency peg to the Deutsche Mark. Rather than tipping the economy into recession, the adjustment coincided with a sharp acceleration in private consumption and investment.

The standard interpretation, advanced by Giavazzi and Pagano in their 1990 paper, is that the credibility of the fiscal adjustment, signaled by the exchange rate anchor6 and the durability of the spending cuts, shifted household expectations about future taxes downward, boosting current consumption through the wealth effect.

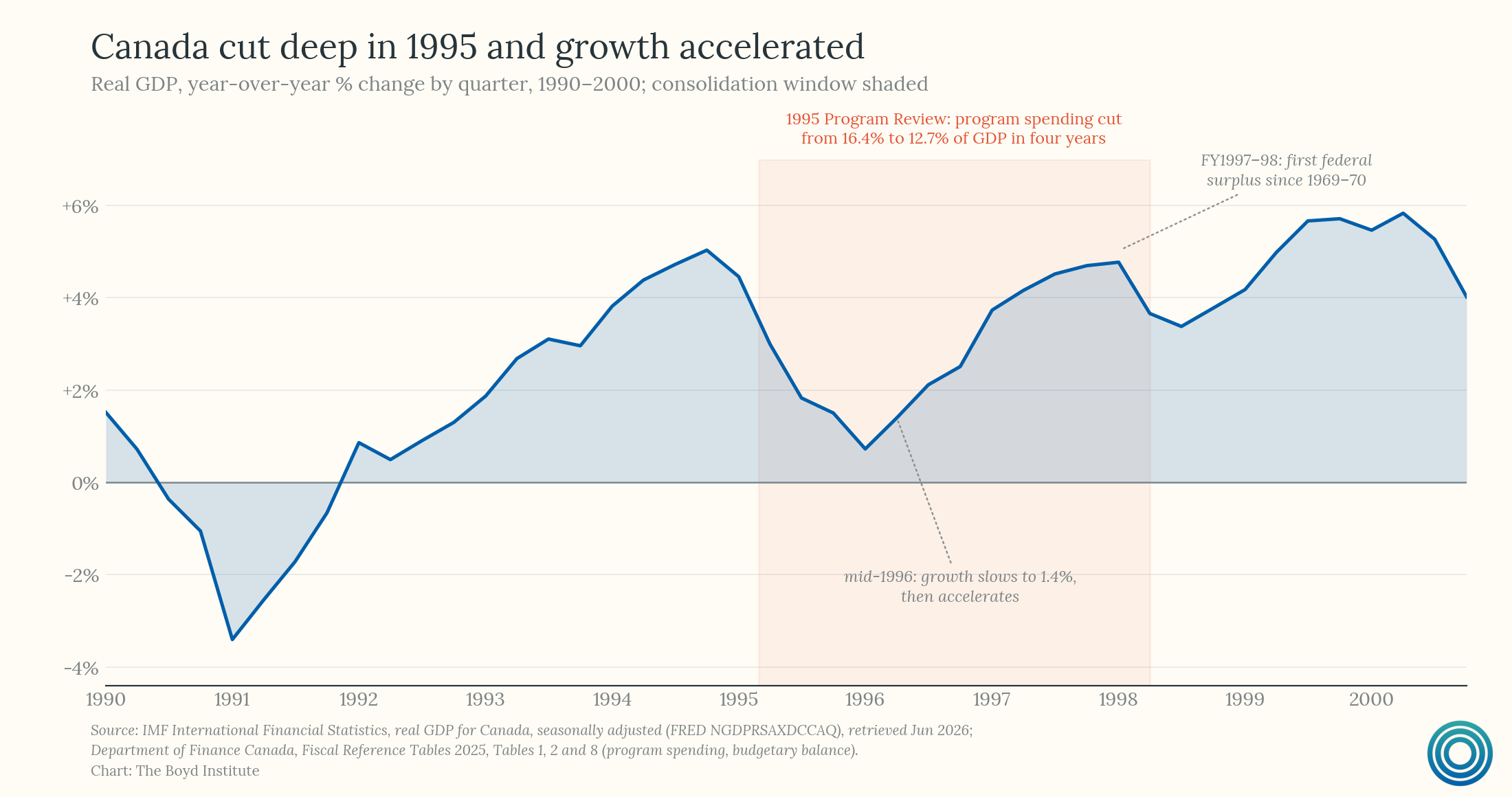

Canada

Canada’s adjustment in the mid-1990s is particularly instructive because it was larger in scale and implemented without an exchange rate anchor. By 1995, Canada’s federal debt-to-GDP ratio had reached 70 percent and its sovereign credit rating was under threat. The Liberal government of Jean Chrétien, working with Finance Minister Paul Martin, implemented a consolidation plan that reduced program spending by roughly 20 percent ($25 billion) over three years (about four points of GDP), a pace of adjustment more aggressive than almost anything attempted in Europe two decades later. The cuts fell heavily on transfers to provinces, public sector employment, and subsidies to crown corporations, while tax increases played a marginal role.

Growth slowed modestly in the first year and then rebounded strongly; by the late 1990s, Canada was running primary surpluses and its debt ratio was in rapid decline.

The Canadian case is difficult to fully disentangle from the concurrent boom in global commodity prices and the depreciation of the Canadian dollar, both of which provided external tailwinds to its energy and lumber exporting sectors, but the speed and durability of the fiscal turnaround remains remarkable.

Ireland

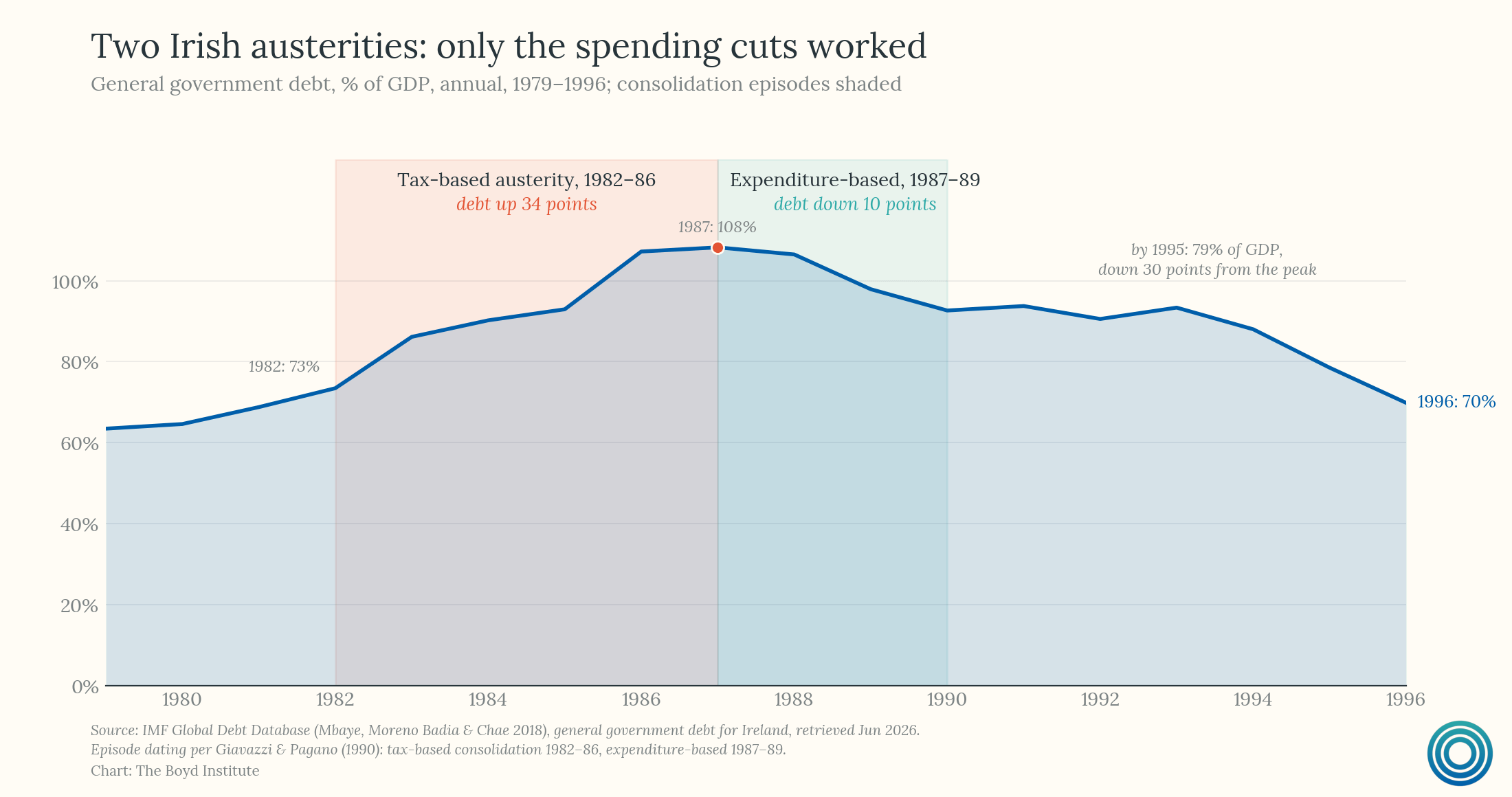

Ireland’s experience prior to the euro crisis provides the sharpest internal contrast in the austerity literature. Between 1982 and 1986, Ireland attempted to close a yawning fiscal deficit primarily through successive rounds of tax increases. Income tax rates were already high and were raised further, VAT was increased, and new levies were introduced across the tax code. The effort failed comprehensively. Output stagnated, unemployment climbed to 17 percent, emigration accelerated, and the debt-to-GDP ratio continued rising despite the fiscal drag. By 1986, the deficit was barely smaller than it had been four years earlier, and the economy was mired in a low-growth equilibrium that showed no sign of self-correction.

The adjustment after 1987 took a fundamentally different form. The incoming Fianna Fáil government, working under a national social partnership agreement on secured wage moderation in exchange for tax reform, front-loaded deep cuts to public expenditure, particularly the public sector wage bill, capital spending, and social transfers, while holding and eventually reducing tax rates. Corporate tax policy was made more favorable to foreign investment.

The results defied the predictions of the simple Keynesian model: growth accelerated sharply, private investment rose, unemployment began a long decline, and the debt-to-GDP ratio fell throughout the consolidation. Ireland’s two consolidation episodes, separated by only a few years and applied to the same economy with similar initial conditions, constitute something close to a natural experiment in the authors’ central thesis.

The composition of the adjustment, tax-heavy in the first instance, expenditure-based in the second, appears to account for most of the difference in outcomes.

None of these cases are clean. Each can be contested on the grounds that external conditions were favorable, that monetary policy was accommodative, or that country-specific factors — a flexible exchange rate, a particular institutional arrangement, a fortuitous alignment with the global cycle — explain the outcomes as much as the composition of the fiscal adjustment does.

Alesina and his co-authors are aware of these objections and address them through their econometric framework, attempting to control for cyclical conditions and monetary policy stances. Their conclusion is that the composition effect survives these controls. But whether the controls are fully adequate remains an open question, and the eurozone crisis provided a set of test cases that put the framework under considerable stress.

The Eurozone Crisis

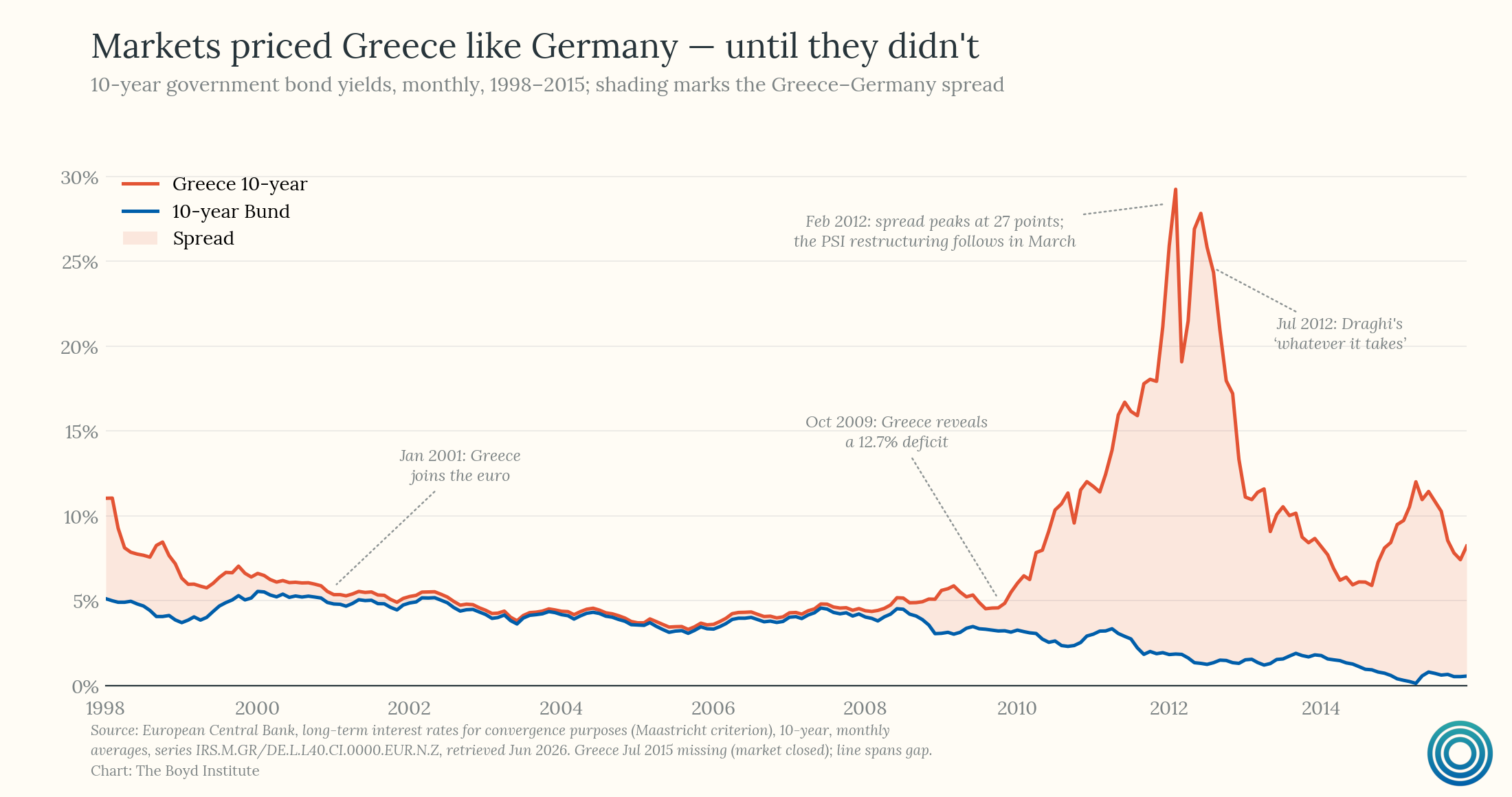

The sovereign debt crises that swept through the eurozone periphery after 2010 became the most closely watched natural experiment in fiscal policy in decades. The trigger was a sudden repricing of sovereign risk: bond markets, which had treated eurozone debt as near-interchangeable through most of the 2000s, began demanding sharply higher yields to hold the obligations of weaker member states. Greek ten-year yields eventually reached an all time high of ~37% in March 2012, shutting Athens out of private capital markets entirely; Portuguese and Irish debt followed, while Spanish and Italian yields backed up to levels that raised serious questions about debt sustainability in the eurozone’s third and fourth largest economies. Greece restructured its sovereign debt in 2012, imposing roughly 50 percent losses on private creditors in what was then the largest such restructuring in history.

The underlying vulnerabilities differed by country but shared a common architecture. Eurozone membership had compressed borrowing costs across the periphery through the 2000s, enabling fiscal looseness in Greece, construction-driven credit booms in Spain and Ireland, and persistent current account deficits across the bloc. When the 2008 financial crisis exposed those imbalances, investors reconsidered the implicit assumption that membership constituted a joint guarantee — and the ECB’s explicit mandate against monetary financing of sovereigns meant there was no institutional backstop against self-fulfilling runs on even solvent governments.

Four countries, Greece, Portugal, Spain, and Italy, were thus forced into large-scale fiscal consolidations under varying degrees of external pressure. Greece and Portugal (as well as Ireland) accepted formal troika programs — administered jointly by the European Commission, the ECB, and the IMF — with disbursements conditional on fiscal targets and structural reforms. Spain and Italy, too large to bail out under existing facilities, faced market pressure without formal programs.

All operated within a monetary union that precluded exchange rate adjustment, concentrating the full burden of rebalancing on wages, prices, and fiscal retrenchment. We’ll begin with Greece.

Greece

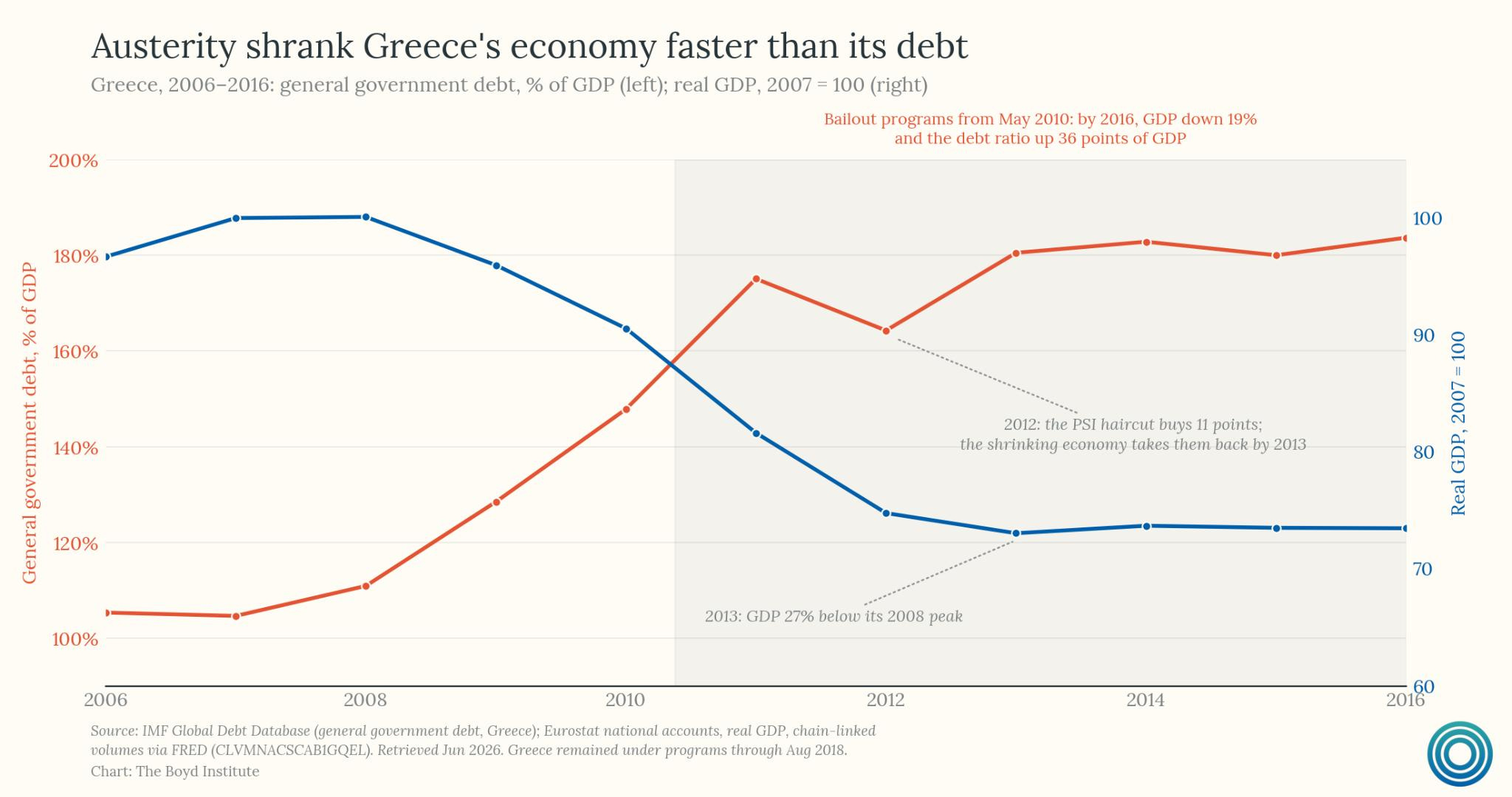

This is the hardest case for any framework to accommodate. The scale of the required adjustment was without modern peacetime precedent: a primary deficit that peaked above 10 percent of GDP had to be eliminated within a few years under troika conditionality. The composition was mixed, combining deep cuts to public sector wages and pensions with large increases in VAT, income taxes, and a succession of emergency levies.

Because the Greek state had limited capacity to cut the kinds of transfers and discretionary spending that the expenditure-based template requires — much of Greek public spending was constitutionally protected or practically impossible to reduce quickly7 — the adjustment was inevitably more tax-heavy than the Alesina framework would recommend. GDP fell by more than 25 percent over five years, unemployment peaked above 27 percent, and the debt-to-GDP ratio rose throughout the consolidation, as collapsing output overwhelmed the primary surplus that was eventually achieved.

Whether a purely expenditure-based adjustment would have produced better outcomes is genuinely unclear. It is not obvious that such an adjustment was available: the Greek state’s institutional capacity to implement spending cuts was limited, and the social and political constraints on the size of the adjustment were severe regardless of its composition.8

Portugal

Portugal’s experience is more amenable to the authors’ framework. Its adjustment program, initially front-loaded with tax increases, pivoted toward expenditure restraint in its later years. The painful early phase produced a sharp recession. As the composition shifted, with reductions in public sector wages, transfers, and subsidies taking on a larger share of the adjustment, the pace of contraction moderated. Portugal exited its bailout program in 2014 without a debt restructuring, achieved a primary surplus, and subsequently posted some of the stronger growth rates in the eurozone.

The Portuguese case does not unambiguously vindicate the spending-cut thesis — the recovery also benefited from the ECB’s more activist posture after Mario Draghi’s 2012 “whatever it takes” intervention and from strong export growth — but its trajectory is broadly consistent with the prediction that shifting the composition of adjustment toward expenditure produces better outcomes over time.

Spain

Spain’s consolidation is perhaps the most complex. Its post-2010 adjustment combined tax increases, regional spending cuts, and significant structural labor market reforms that reduced the cost of hiring and firing and moderated wage growth in the tradable sector. The labor market reforms were arguably as important as the fiscal measures in restoring Spanish competitiveness and eventually driving the recovery. Unemployment reached 26 percent at its peak, but Spain’s recovery was more durable and more broad-based than Greece’s, aided by a more diversified economic structure and stronger institutional capacity.

Spain suggests that the composition of structural reform matters alongside the composition of fiscal adjustment, and that the two interact in ways the Alesina framework does not fully capture.

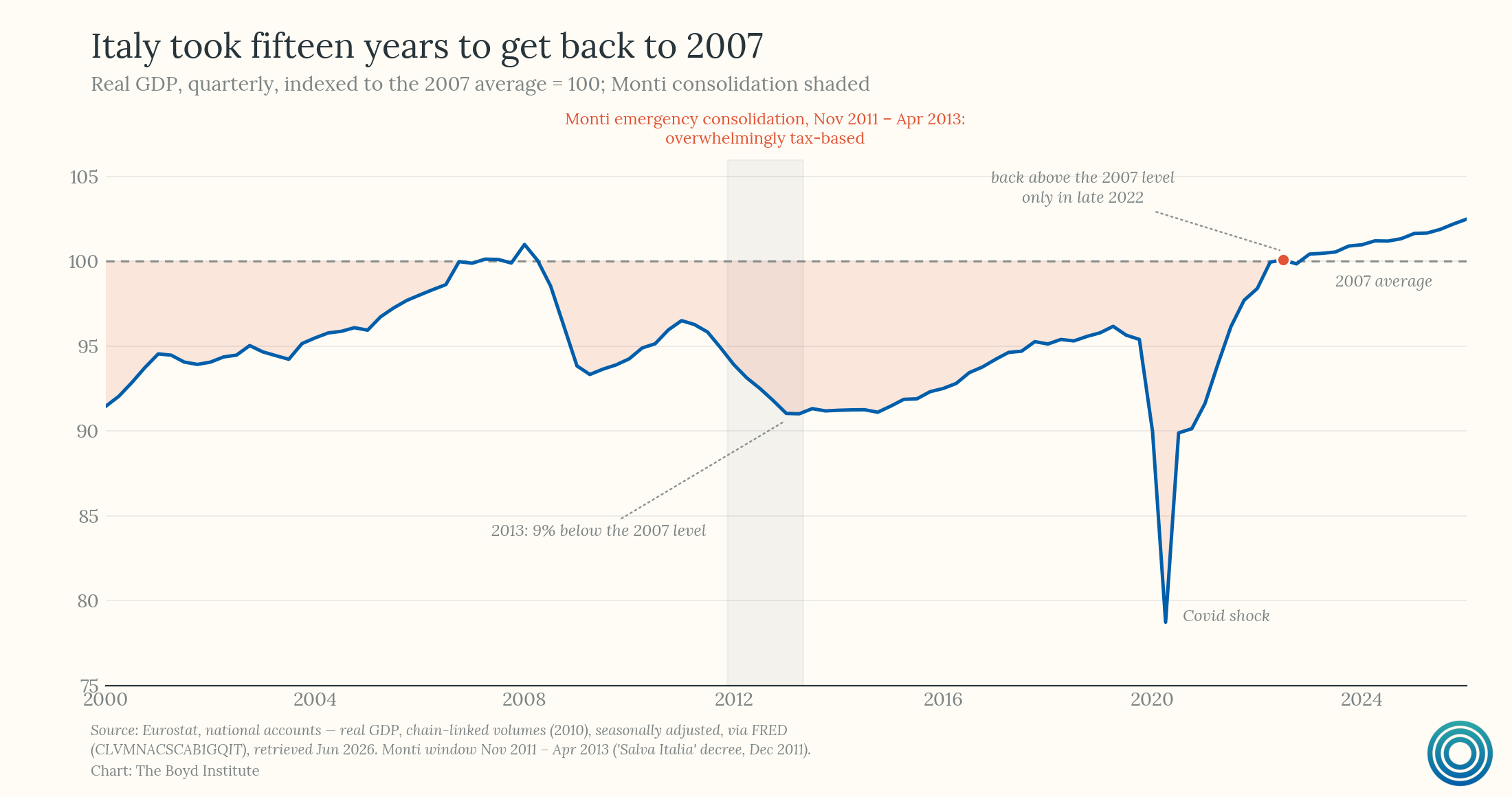

Italy

Italy presents the most uncomfortable case for the book’s thesis, not because it disproves the composition argument, but because it illustrates how binding the political constraints can be. The Monti government’s emergency consolidation of 2011 and 2012 relied overwhelmingly on tax increases: a major revival of the property tax, a sharp rise in fuel duties, increases in VAT, and a surcharge on high incomes. Meaningful spending restraint was essentially off the table in a country with deep clientelistic networks and constitutionally protected entitlements. The result was a double-dip recession that pushed Italian GDP more than 9 percent below its 2007 peak by 2013, from which the country had still not fully recovered a decade later.

The composition was wrong in precisely the way Alesina predicts, and the outcomes were correspondingly bad. But the lesson Italy teaches is not simply that you should cut spending instead of raising taxes. It is that when cutting spending is institutionally unavailable, the theoretical optimum offers no practical guidance. The framework tells you what works; Italy shows that what works is not always what is possible.

Britain

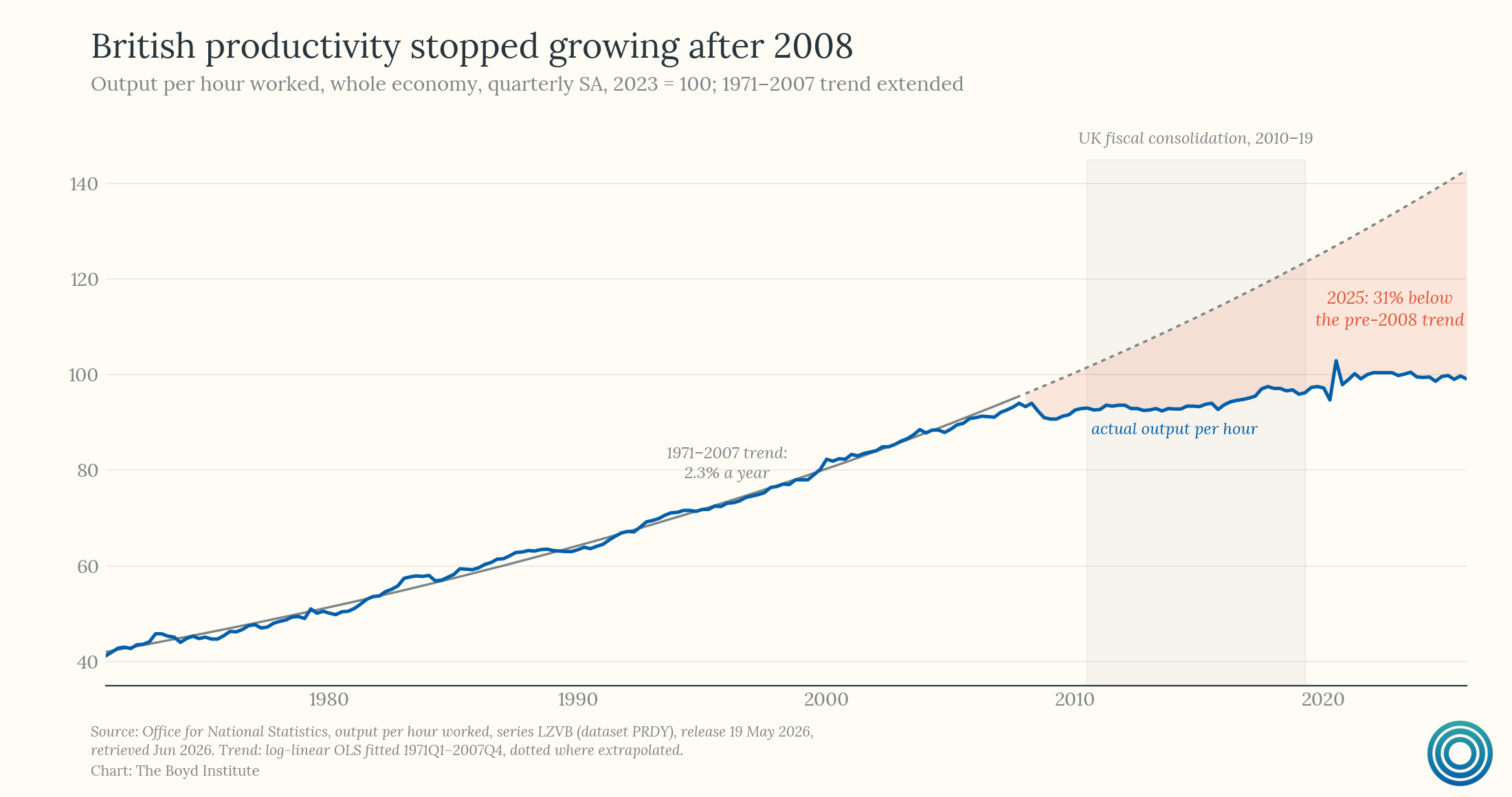

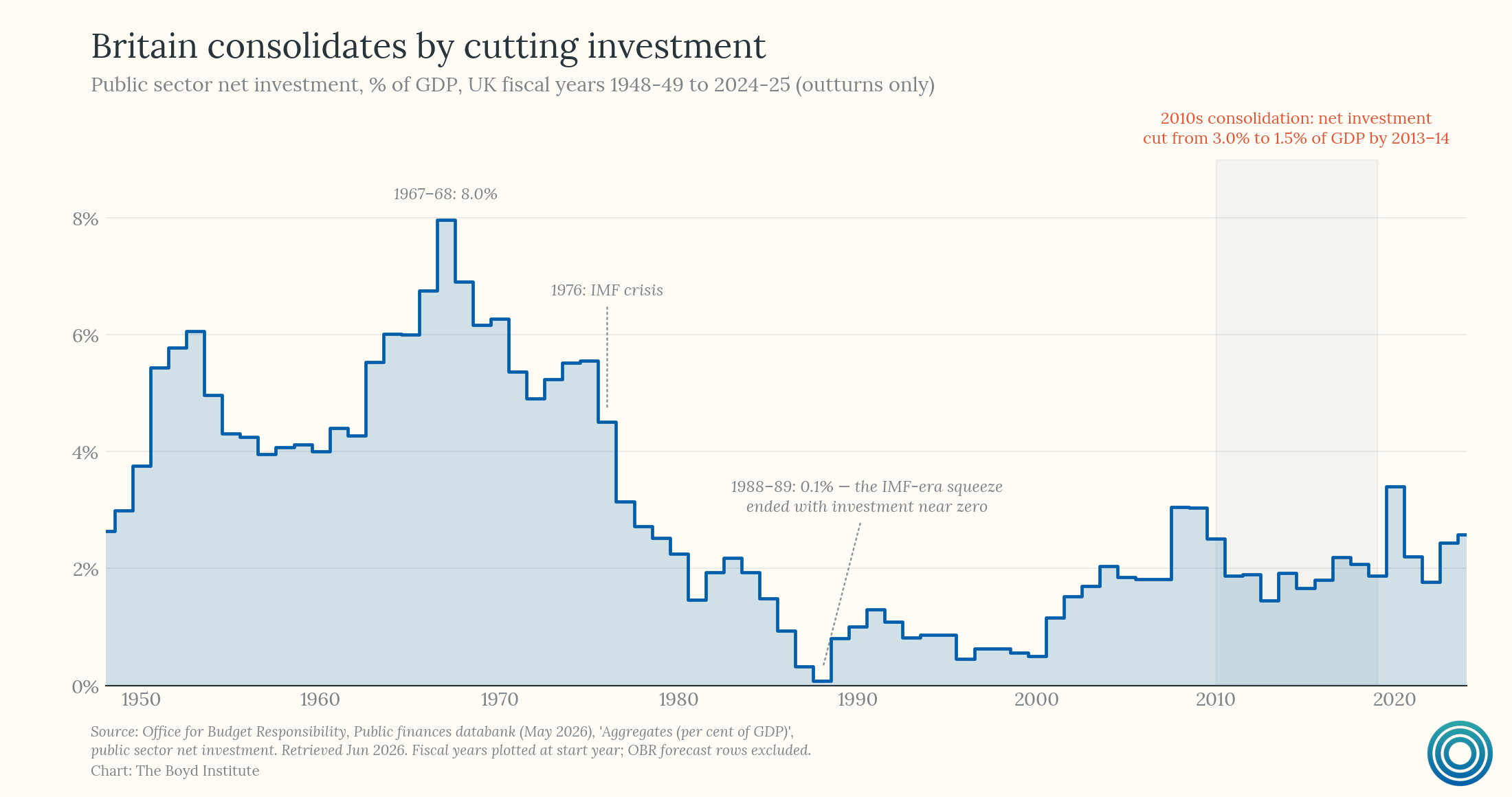

The authors cite Britain’s post-2010 consolidation under George Osborne as a qualified success for the spending-cut approach, and the initial evidence appeared to support this reading: the deficit fell, the sovereign credit rating was preserved, and growth returned by 2013. In retrospect, this verdict looks considerably less secure. British productivity growth was exceptionally weak throughout the austerity decade, with output per hour flatlining in a way that had no precedent in postwar data.

Public investment, which bore a disproportionate share of the cuts, fell sharply and stayed low, and may have depressed the economy’s long-run supply capacity in ways that do not show up in short-run output statistics.9 The National Health Service and local government services were compressed to the point where the structural damage is still being counted.

Britain’s consolidation may have succeeded in narrow fiscal terms while imposing large, diffuse costs that were slow to materialize and difficult to attribute to any single policy decision. This possibility points toward a refinement the Alesina framework needs but does not fully provide.

Not All Spending Cuts Are Equivalent

Cuts to government consumption, public sector wages, administrative overhead, and procurement are likely to have different long-run consequences than cuts to public investment in infrastructure, research, and human capital, which generate returns that persist for decades. The framework treats these as broadly equivalent, and this aggregation obscures an important distinction.

The evidence from a range of empirical studies suggests that the multiplier on public investment is substantially higher than the multiplier on government consumption, meaning investment cuts impose larger output losses per dollar saved. More importantly, sustained underinvestment operates on a timescale beyond the five year horizon over which the book’s analysis is conducted. An austerity program that achieves its fiscal targets by gutting public investment may look successful in the medium run while quietly eroding the supply-side foundations of future growth.

An Updated Model

Taken together, these cases suggest that the Alesina framework needs to be embedded within a broader set of conditions rather than applied as a free-standing rule. The core insight — that composition matters, and that tax-heavy consolidation is reliably more damaging than expenditure-based adjustment — survives scrutiny.

But it operates against a background of contingencies and countervailing factors that are also determinants as to whether even a well-designed austerity plan will succeed.

The most important contextual factor is the monetary policy environment. Expenditure-based austerity works best when it can be accompanied by monetary easing or, for countries with independent currencies, exchange rate depreciation. The crowding-in effects that Alesina’s successful cases illustrate depend partly on the central bank’s ability to cut rates in response to fiscal tightening, and on the exchange rate’s capacity to shift demand toward the tradable sector as domestic demand contracts. When interest rates are at the zero lower bound, the conventional monetary offset is unavailable and the fiscal multiplier on spending cuts rises — though this constraint is not absolute. Unconventional tools such as quantitative easing can provide some offsetting stimulus even at the lower bound, and the degree to which QE substitutes for conventional rate cuts remains contested. The evidence suggests it is a partial, and often insufficient, substitute: it operates through different transmission channels, is harder to calibrate, and its effectiveness varies significantly with financial market conditions and central bank credibility.

Countries in a currency union face this constraint in an amplified form. They cannot depreciate and must instead rely on internal devaluation — cuts to wages and prices — to restore competitiveness. That process is slow, painful, and politically destabilizing. This is not an argument against austerity within a currency union; it is an argument that the required composition of the adjustment becomes even more critical, and the tolerance band for error even narrower, than in countries that retain monetary autonomy.

Equally important is what gets cut. A consolidation plan that identifies savings in transfers, subsidies, public sector wages, and administrative overhead is likely to produce better long run outcomes than one that achieves the same headline number through cuts to infrastructure investment, education, or preventive health care. This is not simply a Keynesian argument about demand, it is a supply-side argument about the economy’s long-run productive capacity. Britain is the cautionary example here: a consolidation that front-loads cuts to public investment in order to protect current consumption may look fiscally responsible in the near term while imposing costs that compound quietly over years and decades. Protecting public investment should be a near-inviolable constraint on any consolidation plan, even at the expense of a slower pace of overall adjustment.

Harder to manufacture than it is to describe, credibility may matter most of all. The expansionary consolidations in the historical record share a common feature: they were undertaken in a way that made forward-looking households and firms willing to revise their expectations about future tax burdens downward. When a consolidation is perceived as durable and well-designed — i.e., when the spending cuts are seen as warranted and permanent, rather than temporary — and when the institutional framework supports that perception, the expectation of a lighter future tax burden can offset some or all of the immediate demand drag. When it is perceived as half-hearted, performative, or reversible, this mechanism does not operate, and the contractionary arithmetic of the IS-LM model reasserts itself. Credibility cannot be willed into existence; it is earned through specificity, political durability, and the track record of the institutions implementing the plan. A government that has repeatedly announced and then retreated from consolidation plans will find that the confidence channel is closed to it, regardless of how well-designed its latest proposal is.

Conclusion

Alesina, Favero, and Giavazzi have produced the most empirically rigorous examination of fiscal consolidation available, and their central finding — that composition matters, and that tax-based austerity is reliably more damaging than expenditure-based adjustment — is well-supported by the evidence.

But the framework is not without its limitations. It underweights the role of monetary conditions in determining fiscal multipliers, aggregates government spending in ways that obscure the critical distinction between consumption and investment, and draws on a set of historical success cases whose favorable conditions are not always replicable. The British example, now with a longer run of data, is a warning against premature declarations of vindication.

For the United States, the framework offers guidance that is directionally correct but requires significant elaboration. The federal government’s long-run fiscal challenge is primarily a function of mandatory spending — Social Security, Medicare, and Medicaid, growing faster than revenues. Any durable consolidation plan will need to address the expenditure side of the budget, and the Alesina evidence strongly supports the conclusion that doing so will be less damaging than attempting to close the gap through tax increases alone. But the framework’s silence on public investment is a genuine gap. A consolidation that preserves or increases investment in infrastructure, clean energy, and scientific research while achieving savings through reforms to entitlement growth, procurement, and transfers would be consistent with the book’s core thesis while avoiding the long-run supply-side damage that indiscriminate spending cuts risk.

The deeper challenge is political rather than economic. The spending cuts most likely to achieve durable fiscal consolidation — reforms to entitlement growth, reductions in transfers, restraint of the public sector wage bill — are precisely the cuts most difficult to sustain politically. The historical success cases Alesina identifies were often implemented under conditions of acute fiscal crisis, where the normal political constraints were temporarily suspended by the sheer urgency of the situation. That is a poor model for deliberate reform. Getting the composition right is necessary but not sufficient. Timing, credibility, and political durability are the conditions under which composition does its work, and assembling all three, in a political environment where the costs of adjustment are concentrated and the benefits are diffuse, is the hardest part of the problem that no economic framework can solve.

This is precisely why the current moment matters. When labor markets are firm, output is expanding, and private capital is flowing into productivity-enhancing investment at scale, the political costs of entitlement reform are lower, the credibility of consolidation is easier to establish, and the risk that fiscal tightening tips into a self-reinforcing downturn is diminished. The case for preserving targeted public investment in R&D and infrastructure is also strongest in this environment — not as a concession to spending interests, but because a government that consolidates intelligently now can remain a complement to private dynamism rather than a drag on it. The window is not permanent. Consolidations undertaken by choice, in favorable conditions, on well-designed terms, have a historical record worth taking seriously. Those forced by crisis do not.

In a closed economy with a fixed money supply, this effect is dampened somewhat by a fall in interest rates, the crowding-in effect, but the net result is still contractionary.

To be sure, unconventional monetary policy can still operate through other channels. As the former chairman of the Federal Reserve Ben Bernanke argued in defense of quantitative easing, higher asset prices can generate a wealth effect that encourages households to spend more, thereby supporting aggregate demand. Yet this channel is indirect and may be weaker than the income effect associated with changes in current earnings and disposable income. If households base spending decisions primarily on current income rather than increases in paper wealth, monetary stimulus transmitted through asset prices will provide only a limited offset to fiscal contraction.

There is a substantial meta-analytic literature attempting to extract signal from this noise. Sebastian Gechert’s meta-regression analysis of 104 studies finds that public spending multipliers cluster around 1, and are roughly 0.3 to 0.4 units larger than tax and transfer multipliers, with public investment multipliers larger still. The regime-dependent meta-analysis by Gechert and Rannenberg (2018), drawing on 98 empirical studies, finds that spending multipliers are substantially higher during downturns — by roughly 0.7 to 0.9 units — while tax multipliers show less sensitivity to the economic cycle. These meta-analyses represent the closest thing the literature has to a synthesis verdict, though they are themselves contested on methodological grounds. At the individual-study level, the spread remains dramatic: Christina Romer and David Romer, working from narrative identification of postwar U.S. tax changes, found multipliers on tax cuts exceeding three, consistent with the Keynesian prediction. Robert Barro and Charles Redlick, analyzing wartime spending episodes, arrived at multipliers close to zero or slightly negative for peacetime periods. Francesco Giavazzi and Marco Pagano produced cases where spending cuts appeared to be expansionary on net — a finding so heterodox that it gave rise to the phrase “expansionary austerity,” and provoked a debate that has yet to be fully resolved.

The eurozone consolidations of 2011–13 have become something of a natural experiment for the multiplier debate, and the retrospective verdict has been harsh. Fiscal tightening across the eurozone accumulated to roughly 4% of annual GDP between 2011 and 2013, and was associated with a return to recession. The Blanchard-Leigh finding — that the IMF had used a multiplier of around 0.5 when the true value was closer to 1.5 — implied that the damage inflicted was approximately three times what policymakers had forecast. Antonio Fatás and Lawrence Summers subsequently extended this analysis to longer time horizons, finding strong evidence of hysteresis: fiscal consolidations in this period appear to have permanently lowered the path of GDP, and in some cases the attempts to reduce debt ratios via austerity likely resulted in higher debt-to-GDP ratios through the long-run destruction of output. The case against the prevailing policy was being made in real time.

The zero lower bound point deserves elaboration beyond its role in multiplier arithmetic. Once the policy rate hits zero, conventional monetary policy loses its ability to offset fiscal contraction — the central bank cannot cut rates to cushion the blow of spending cuts. This creates the conditions under which fiscal multipliers are theoretically largest, since there is no monetary “crowding out” to dampen the effect. The implication cuts in both directions: fiscal stimulus is maximally powerful, and fiscal austerity is maximally destructive. This is also part of the case against treating quantitative easing as a full substitute for fiscal expansion during the 2010s U.S. recovery. With the Fed already at the zero lower bound, fiscal policy had an unusually high-leverage window to act — the multiplier was at or near its peak, and monetary policy could not undo the contractionary effect of premature consolidation. Instead, fiscal policy tightened (particularly at the state and local level, and after the 2011 debt ceiling standoff at the federal level), leaving the Fed as the dominant macroeconomic actor through successive rounds of QE. Whether QE provided comparable stimulus to fiscal expansion in that environment remains disputed, but the structural substitution of unconventional monetary for fiscal policy meant the economy operated inside its stabilization frontier during what was, by the multiplier literature’s own terms, the period of maximum fiscal leverage.

On the regime-switching question: Auerbach and Gorodnichenko (2012) provide the canonical econometric treatment, using smooth-transition VAR models to estimate state-dependent multipliers. They find large differences between recession and expansion regimes, with fiscal policy considerably more effective in downturns. DSGE models incorporating zero-lower-bound constraints suggest spending multipliers in that regime could range from 3 to 5 — substantially above any linear-model estimate.

A fixed exchange rate operates as a credible commitment device because it binds the hands of monetary authorities in ways that are costly to reverse, thereby anchoring private-sector expectations. When a government pegs its currency — whether unilaterally or within a formal arrangement such as the European Exchange Rate Mechanism (ERM) — it effectively surrenders discretionary control over monetary policy. Interest rates must be set to defend the peg rather than to smooth domestic cycles, and any resort to inflationary financing of deficits becomes immediately visible and punishable through speculative pressure on the currency. This constraint transforms fiscal consolidation from a mere policy announcement into a verifiable pledge: markets understand that the government cannot inflate away its obligations or engineer a competitive devaluation as an easy exit from adjustment.

Greece entered the crisis with a public sector characterised by weak administrative capacity, fragmented payroll systems across hundreds of entities, and a pension architecture spread across dozens of funds with independent legal bases. Constitutional protections for certain categories of public employment and court rulings striking down earlier wage cuts further constrained the pace of retrenchment. The practical difficulty was not simply political resistance but the state's limited ability to identify, measure, and execute cuts with any precision.

This points to a structural limitation in using any of the Eurozone consolidation episodes — Greece, Portugal, Ireland, Spain — as tests of the Alesina hypothesis. The canonical cases on which that framework was built (Denmark in the 1980s, Ireland in the late 1980s, and Canada in the 1990s) involved countries with their own currencies and independent central banks. Exchange rate depreciation played a meaningful role in each: export competitiveness improved as fiscal contraction compressed domestic demand, cushioning the output cost and providing an alternative mechanism for adjustment. Eurozone members under troika programmes had no such channel. The European Central Bank set monetary policy for the currency area as a whole, and the exchange rate was fixed relative to their main trading partners.

Mario Draghi’s 2024 report on European competitiveness argues that sustained underinvestment in infrastructure, innovation, and energy systems has become a significant constraint on European growth. The concern raised here for Britain therefore applies more broadly: fiscal adjustments that protect current spending at the expense of public investment may achieve fiscal consolidation while eroding long-run productive capacity.

I remember being ~8-9 years old, sitting at the dinner table in the late 1990’s, and openly wondering why the government wasn’t making big cuts and reforms because everything was roaring and booming and it seemed insane to wait until a crisis to make cuts which would be easy to make when everything was so good. I think this ultimately made events 10 years later more shocking to my young mind.

"Their findings challenge one of the central assumptions of modern Keynesian macroeconomics: that spending cuts necessarily impose larger economic costs than tax increases."

OK, I'm not a macroeconomist, but I never overhed this idea, much less that it is "central." A priori eiher could be the case. It woud depend on the initial conditions Where are the margins? what is the DWL of the marginal tax increase vs the DLW of the marginal expenditure to be cut? I can't see how looking cross country could address this.

Take the US for example. Consolidation by substituting a VAT for FICA and a progressive consumption tax for the personal and business income tax would reduce DWL. Reducing expenditures on farm and ethanol and most "green" subidies would reduce DWL, reducing social insurance benefits very little and on science and technology loss would increase.

"Tax" vs "Expenditure" seem far to crude to do much good.