Debt for Dummies

And why YOU should care about the national debt

People talk a lot about debt in vague technocratic language that is both needlessly confusing and obfuscatory. So today I want to explain how the US debt actually works in layman’s terms and why paying so much in interest is bad.

How the national debt works

When the federal government spends more than it collects in taxes, it covers the gap (deficit) by issuing Treasury securities. Mechanically, the buyer of these bond securities pay the face value of the bond and in turn receives a fixed dollar payment, called a coupon, usually twice a year. After a predetermined period, when the bond “matures,” the government returns the principal. The interest rate then is the ratio of annual coupon to face value.

The market for Treasury securities is the largest and most liquid bond market on the planet. In practice, though, almost no one transacts one bond at a time. The action starts with institutional bidding in the primary market, where the government auctions off new debt directly (wholesale) to a small group of primary dealers and other authorized bidders.

The secondary market — the main locus of liquidity — is where everyone else trades those securities afterward. It’s here where daily Treasury prices and yields are quoted, where the Fed conducts its Treasury-related open market operations, and where the vast majority of price discovery and trading volume occurs (including retail or ‘mom-and-pop’ buying and selling).

The final technical piece of information you need to know about is “the yield curve”, or the relationship between Treasury yields and time to maturity. The short end — T-bills ranging from 1 to 12 month maturities — tracks the fed funds rate closely. But the long end — Treasury notes and bonds with maturities ranging from 1 to 30 years — is a different beast. Long-dated yields reflect things the Fed may influence but does not actually set, namely market expectations of long-run inflation1 and, more generally, the balance of supply and demand for long-dated paper.

Who holds it

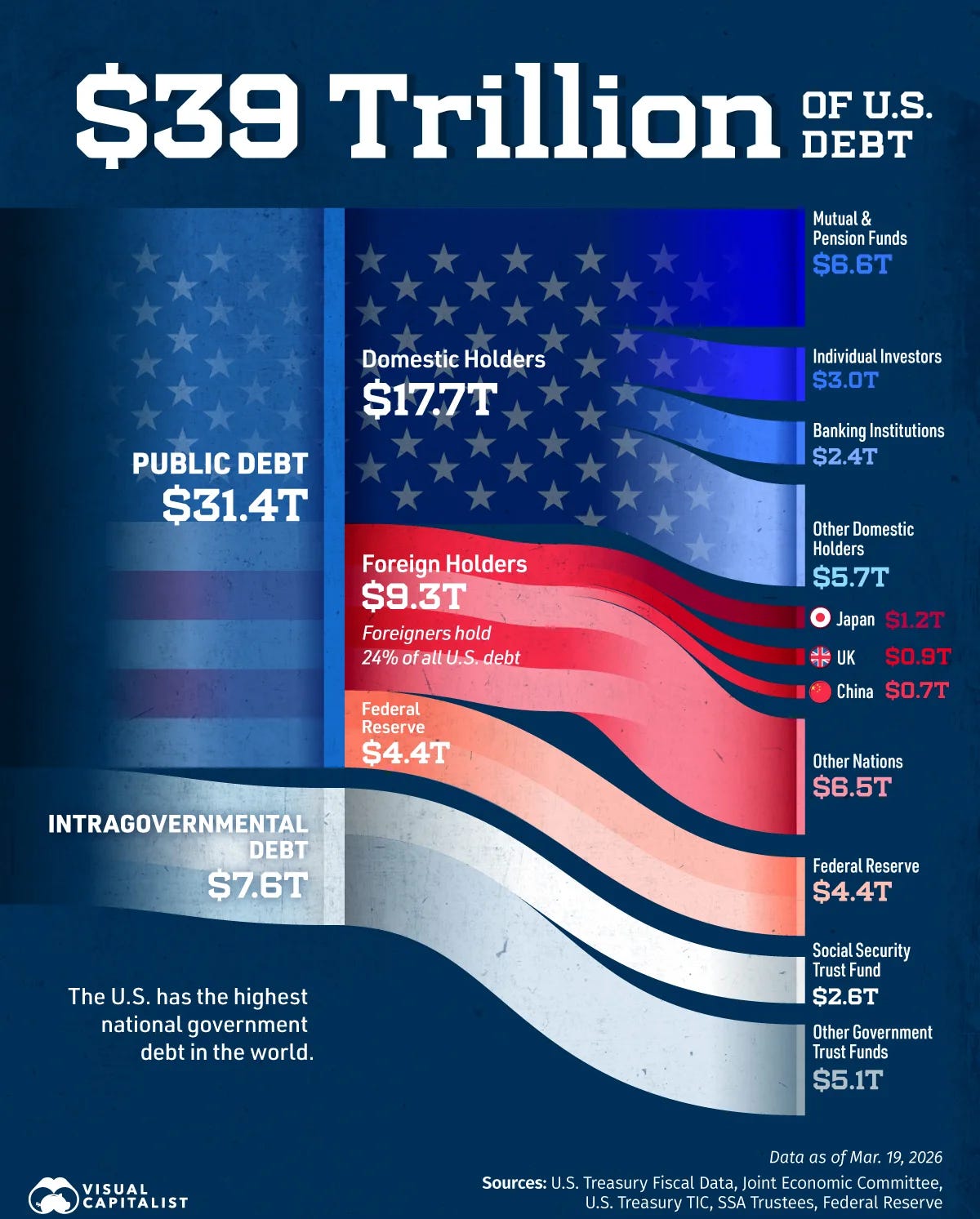

The debt is mostly held by three groups.

The first is the government itself.2 The Social Security trust fund, the Civil Service and Military Retirement funds, Medicare’s trust fund, plus the Federal Reserve, together hold roughly twelve trillion dollars in Treasury securities.

The second is foreign investors, who hold roughly nine trillion dollars, nearly a fourth of the total outstanding debt. Most of this represents holdings by foreign central banks and sovereign entities that buy Treasuries as a safe, liquid store of dollar value. A world that trades in dollars needs a place to park them. This is the Hamiltonian case for the existence of federal debt.

The third group is domestic private holders — US banks, hedge funds, pensions, mutual funds, insurance companies, IRAs, 401(k)s, etc. Unsurprisingly, this relatively cleanly to the ownership distribution of assets in general, and so is extremely skewed toward the wealthy. Sandy Brian Hager’s Public Debt, Inequality, and Power documents this in a comprehensive empirical study of US bond ownership.

Why debt is “bad”

It isn’t. The US has always carried debt, and post-Bretton Woods, the global financial system is one big oroborus of the Treasury market. But it does involve a specific tradeoff that, although everyone seems to grasp in principle, is rarely openly discussed. If it were financing investments that raise future growth and productivity, it could be justified as an asset-building tool. It could also be justified on the grounds of “macroeconomic stabilization,” as it was nearly two decades ago in the wake of the Great Financial Crisis.

The problem, however, is that much of today’s borrowing is not going to growth-inducing public capital, but to financing the welfare state and current consumption, which leaves future taxpayers with the bill yet no corresponding productive return. And the sobering reality is that interest payments now consume 18.5 percent of federal revenue — nearly one in five dollars collected by the IRS goes to servicing coupon payments on government bonds. So regardless of whether there is some universally optimal debt load, every borrowed dollar commits the state to a stream of interest payments that displaces other spending.

You can see this clearly in the current US budget. The total deficit, at 5.8 percent of GDP, is abnormally high almost entirely because of interest payments, which run at roughly 3.3 percent of GDP. Strip those out and the primary deficit — the gap between revenues and non-interest spending — is 2.6 percent of GDP, a historically normal figure. Before the state can fund anything, it is obligated to pay bondholders out of tax receipts.

This phenomenon, where interest payments displace other government spending, restricts the state’s capacity to deliver the services it once delivered regularly: things like public works projects and investment in infrastructure. And this is only half the picture. The other half is that interest payments amount to an extremely regressive transfer from taxpayers to capital holders.

Conclusion

The honest framing is this: every dollar of new debt is simultaneously a decision to fund something now and a decision to transfer tax revenue to bondholders for decades after. Politicians on the left argue in favor of funding transfers with debt the entire time committing to future transfers to the rich. And the right denounces spending while hypocritically presiding over exploding deficits. Something needs to change or soon we won’t be able to afford anything but redistributing taxpayer dollars to asset-holders, foreign and domestic.

Which determines the term premium, or the extra yield investors demand for locking their money up for a decade or three.

The Social Security and Medicare trust funds do not hold ordinary marketable Treasuries in the same way a private investor does; much of this is special-issue Treasury debt held inside the federal government’s accounts.

Why does the government need the money that it has already spent or lent, via banks, to be returned, to fund itself?

The spending, taxing, bond buying sequence is indisputable. No one has a dollar to spend unless the government first issues it.

Why does the government need the money that it has already spent or lent, via banks, to be returned, to fund itself?

Issuing US Treasuries is a relic of privilege and a fine example of THE welfare state.