Debt killed the Soviet Empire

"The [communists] will [borrow from] us the rope with which we will hang them."

Among the many competing explanations for the collapse of the USSR, the most plausible, in my opinion, is that the state functionally went bankrupt, and was dissolved in what amounts to essentially a corporate-sovereign restructuring.

Starting in the 1970s and accelerating thereafter, the Soviet growth model — extensive capital accumulation poured into new urban factories, power plants, steel mills, and machine tools — had effectively run out of low-hanging investment opportunities, resulting in persistently diminishing marginal growth potential. This dynamic was compounded by a total lack of market-driven capacity for productivity-driven growth or creative destruction on one side, and ballooning imperial obligations on the other (Easterly and Fischer 1995).

To paper over these holes, the Soviet Union financed its civilian consumption and military spending — along with the subsidies it paid to its puppets — through oil rents made possible by the global energy crisis of the 1970s. But when oil prices normalized again in the mid-1980s, the regime was forced onto international debt markets, where it was eventually strangled.

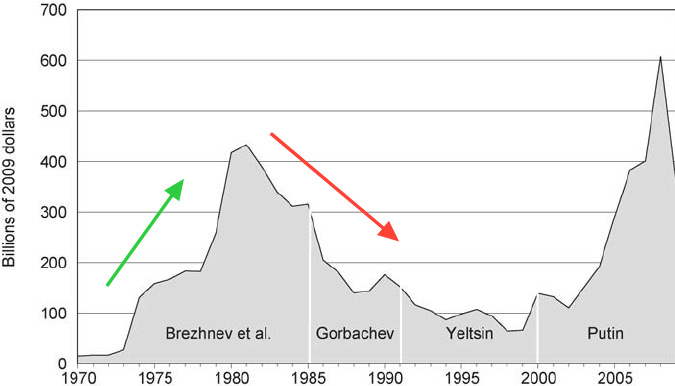

Soviet/Russian oil and gas “rents”:

I’ll develop the argument below, but the most important thing to take from it is that this pattern — fiscal exhaustion under inelastic obligations — is among the most legible and predictable failure modes in the historical record, and that the contemporary United States, while not in the Soviet position, lies on the same structural axis, with buffers that are real but not infinite.

Debt crowding meets central planning

The USSR’s balance sheet was dominated by three items, each of which was load-bearing to the state’s legitimacy. Together they accounted for ~30% of Soviet GNP in 1985, although because of the way planned economies work this is definitionally an estimate.

One, the military. Since the victory of the communists in WW2, the Red Army had acted as a backstop against exit by both its puppets — as seen in Hungary and Czechoslovakia — and domestic dissidents. Western estimates put real Soviet defense spending at 15% to 17% of GNP through the late 1970s and 1980s — triple the US share at the time. More recent estimates have pushed this number even higher.

Two, the Empire. In the initial post-War years, the USSR extracted huge amounts of booty from their conquered western territories — most notably East Germany — but by the 70s this dynamic had reversed. Increasingly, the Soviets were subsidizing their allies through the sale of cheap electricity and petroleum by way of a barter system in exchange for their manufactured goods. Beyond just this were, within the union republics themselves, large variations in endogenous productivity creating a perpetual transfer to Central Asia and the Caucasus as well as Siberia from the more productive western provinces. These transfers channeled through the central government which, in turn, became more and more politically unpopular as resources became zero-sum when growth slowed.

Third and finally, there were direct household consumption subsidies. In order to win compliance from the population, the government directly controlled the distribution of basic goods like housing. But food in particular became extremely expensive; since the USSR was unable to produce enough calories to feed itself, the state imported huge amounts from the globe. Retail subsidies rose from 4 percent of state budget expenditure in 1965 to roughly 20 percent by the late 1980s.

This worked, in a manner of speaking, until it didn’t. Specifically, when Brent crude oil prices halved — from ~$30 a barrel in 1985 to ~$15 in 1986 — it cratered Soviet hard-currency income. The CIA's 1988 retrospective put Soviet hard-currency export earnings at $32B in 1983–84, falling to $25.1B in 1986, with oil earnings alone collapsing from a 1982–84 average of $15.2B to roughly $7B by year-end 1986. In turn, gross hard-currency debt nearly doubled, from ~$22B in 1984 to $41.2B by year-end 1987.1

The result was that the budget deficit, which had traditionally run at 2–3 percent of GNP, blew out to roughly 10 percent by 1985, where it remained. To try and balance this, the USSR began to shift more and more of their oil sales onto the global market and away from the CMEA barter system, starving their puppets. Between 1980 and 1990 the CMEA share fell from 46 percent to 16 percent. Although this did buy the regime breathing room, it played a significant role in accelerating the breakdown of the Eastern European communist regimes.

Ultimately the state was unwilling to either cut domestic subsidies or curb military spending sufficiently, and was in turn forced to borrow from the international market. Gross hard-currency debt, which the CIA placed at about $16.5 billion in 1980 and $20 billion by 1982–83, rose to roughly $54 billion by the end of 1989, and approximately $105 billion at dissolution two years later. Although this was in nominal terms a relatively affordable debt load, because of the closed nature of the Soviet economy they had extreme difficulty raising the hard money to service it — by 1989 Soviet debt servicing alone had risen to ~30% of hard-currency exports.

To add to the woes of international debt, years of money printing had created enormous, and unpayable, domestic obligation. Since output had been static but paper wages had continued to grow during the era of stagnation, families were forced to “save” an increasing share of their income in the state banks. There was nothing worth buying for their money. From this era came the famous aphorism:

“We pretend to work, and they pretend to pay.”

As the state ran out of cash to pay its lenders, the rollover environment decisively deteriorated, and in 1991, the Soviet foreign-trade bank, Vneshekonombank, suspended principal payments on the external debt. Only four days later, on December 8, the Belavezha Accords formally dissolved the Union. The successor states opted to liberalize price discovery in January 1992, and the shortages which characterized the final years of the USSR were immediately replaced by hyperinflation, which wiped out both the domestic obligations and household savings.2

Debt was not the only vector of decline in the USSR — ideological hollowing among the apparatchik class and national unrest were accelerants. But without the loss of fiscal leeway both dynamics would probably have remained manageable; what sharply accelerated them was the collapsing elite payoff matrix that fiscal exhaustion itself produced.

Option one was loyalty to a central regime that was now metaphysically dead, financially insolvent, and unable to enforce its writ. Option two was alignment with the republican nationalists and participation in the anticipated plunder. Unsurprisingly this resulted in a textbook preference cascade where the climbers who would have been ideological communists in the 1960s became intrepid nationalists in 1991.

Once the Baltic states — which had always been restless — declared independence in 1990–91 and immediately began to liquidate state assets and economically privatize, the ball was thoroughly in motion and nothing could stop its momentum.

How does this apply to America?

Direct comparison between the contemporary United States and the late USSR would of course be naive. The US borrows in its own currency and not only regulates, but is funded by, the deepest and most liquid capital markets in the world. Unlike the Soviets, we do not lack access to hard currency or have generally atrophied foreign trade. Countries can persist with huge debt burdens. Japan, for example, has carried general government debt of nearly 250 percent of GDP for more than a decade without much sovereign distress to speak of, and Soviet-style financial repression has no analog in the American economy.

But still the mechanism at play here is one of the most binding in history and has shown up again and again, from the Crisis of the 3rd century in Rome to the collapse of the Ancien Régime. Since debt is a claim on future cash flows, once interest obligations grow beyond the capacity of revenues to pay them while also continuing to maintain the essential services of the state, governments are forced to either squeeze out vital spending or default on their borrowing — formally or through inflation.

Nothing about our current position is a law of nature. America’s “exorbitant privelege” — the dollar’s global reserve currency status — is, and always has been, conditional. Instead, it reflects the high degree of trust the international community currently places in the stability and accountability of American institutions, and that trust can be lost.

Seriously ask yourself what it would actually take for you personally to start holding savings in euros, Swiss francs, or bitcoin. Sustained inflation? Routine debt-ceiling theater in which sovereign payment becomes a domestic political bargaining chip? A pattern of monetary accommodation of fiscal demands? Capital controls floated as a serious policy option? Whatever the threshold is for you, every other holder of dollars is running the same calculus in parallel. The Soviet position in 1980 was one where international creditors were willing to lend at favorable rates, but by 1989 that was no longer true, and by 1991 they could no longer get money from anyone at any rate.

Even if the US doesn’t collapse from our debt, we are already facing the price of crowding out vital spending. Every dollar spent on interest is a dollar that could have been used to provide public services or returned to taxpayers. In 2025, net interest outlays rose to $970 billion — roughly $3,000 per citizen. That figure is approximately equal to the combined budgets of Defense, Homeland Security, Interior and EPA, Agriculture and FDA, and the legislative branch. The United States has tools and time, but it does not have unlimited amounts of either.

When a government's debt is denominated in its own currency, inflation erodes the real value of what it owes.

This sounds quite similar to the arguments made by Anders Aslund in "Russia's Capitalist Revolution." He further emphasized that in the late 80s state enterprise managers used their influence to redirect all attempts at economic reform in order to maximize their opportunities to rent-seek. The real, worthwhile economic reform mostly took place in a window of a few months after the August '91 coup, when Soviet conservatives were temporarily unable to resist. Afterwards those factions regained the upper hand, and reforms didn't resume until the early Putin years. Lesson: don't expect the US political system to deal with the debt issue until and unless it causes an acute crisis.

I'm quite sympathetic to this view, and the perhaps stronger view that it was oil vol specifically that did the most damage. Chernobyl is not part of the story?