Eight Countries With Strong Public Finances

Fiscal strength is engineered, not inherited. And the US has every tool but the will.

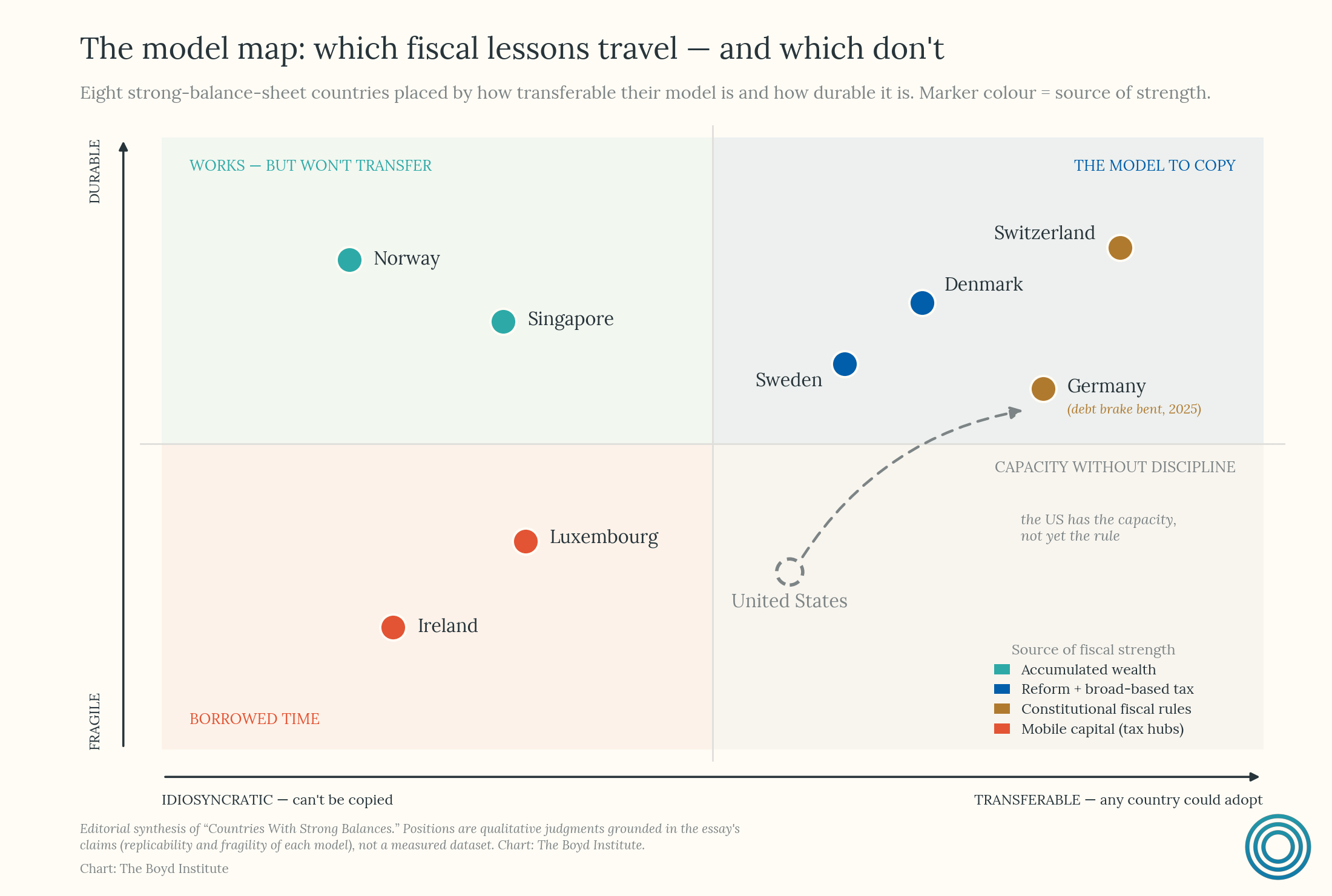

This piece examines eight countries with notably strong public finances — Norway, Singapore, Denmark, Sweden, Luxembourg, Ireland, Switzerland, and Germany — and asks what, if anything, their experience can teach larger, more complex economies. The cases are deliberately varied.

Norway and Singapore derive their fiscal strength from accumulated wealth — oil in Norway’s case, decades of compulsory savings and sovereign investment in Singapore’s. Denmark and Sweden demonstrate that generous welfare states can be compatible with fiscal discipline, but only after rounds of market reform and pension restructuring, and only when financed by broad-based taxation rather than redistribution alone.

Luxembourg and Ireland are cautionary as much as exemplary: their headline finances look impressive, but both live off a concentrated windfall, and unlike Norway and Singapore they spend it rather than save it, building permanent commitments on revenue that a change in tax policy or corporate strategy could redirect. Switzerland and Germany are instructive cases for large advanced economies, though for different reasons and through meaningfully different paths. Switzerland benefits from structural economic advantages that, while not as dramatic as North Sea oil, are nonetheless distinctive. Germany is the more instructive example of fiscal discipline achieved with fewer natural tailwinds.

Governments with high levels of asset holdings, such as Norway and Singapore, can be much more solvent than their headline debt-to-GDP figures suggest. At the same time, windfalls — whether from oil, favorable tax geography, or financial services — should be treated as temporary and saved rather than spent. And fiscal rules, when credibly designed and politically sustained, can secure a country’s fiscal solvency for the long term — though, as Germany’s 2025 constitutional exemption illustrates, even the most durable rules can bend under sufficient investment and geopolitical pressures.

Norway

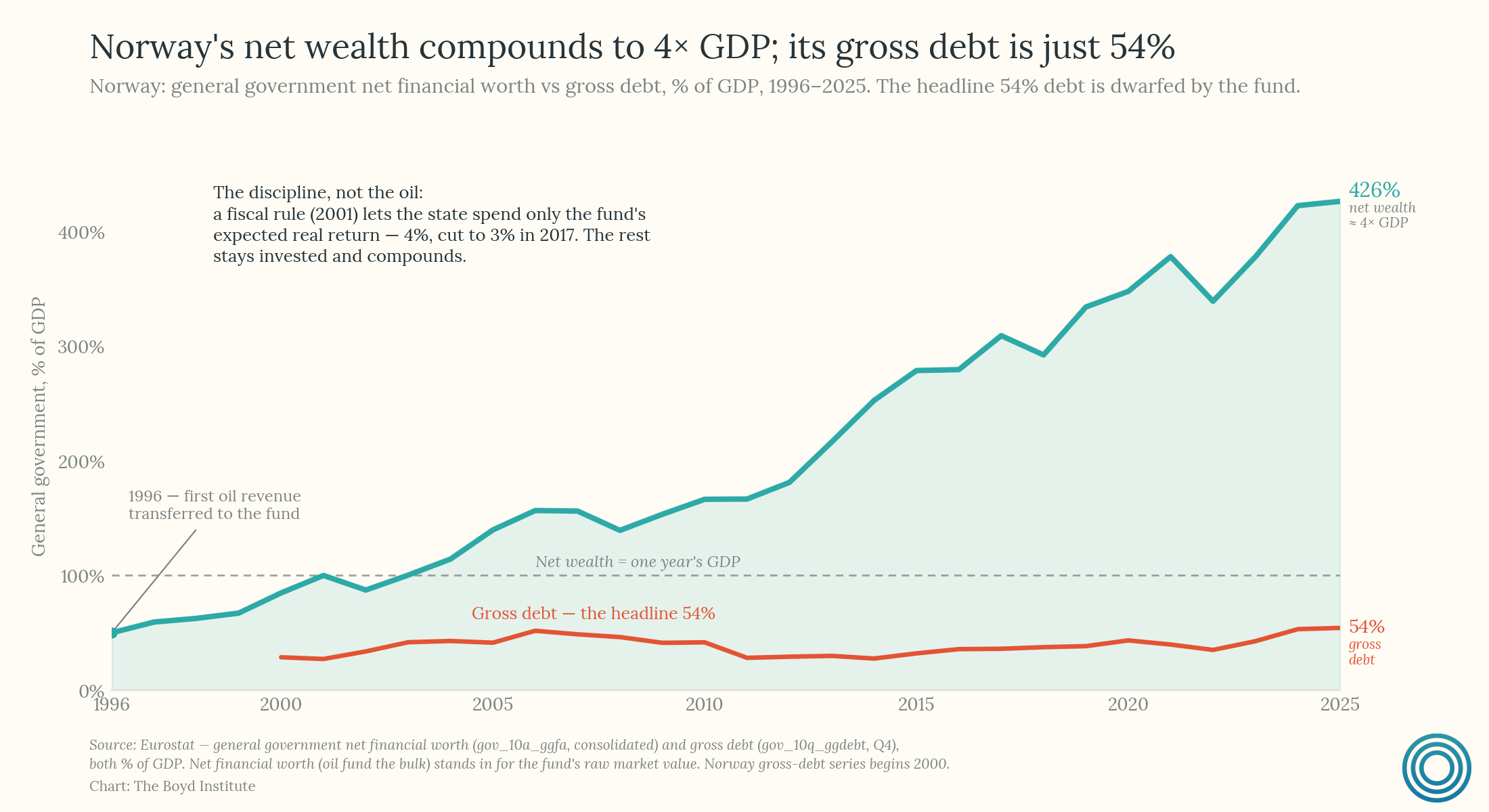

Norway has one of the largest and most comprehensive welfare systems in the world, but also a dynamic economy and one of the best fiscal positions of any nation on Earth. Many commentators attribute Norway’s ability to fund a welfare state without sacrificing growth or fiscal discipline to the nation’s immense oil wealth.

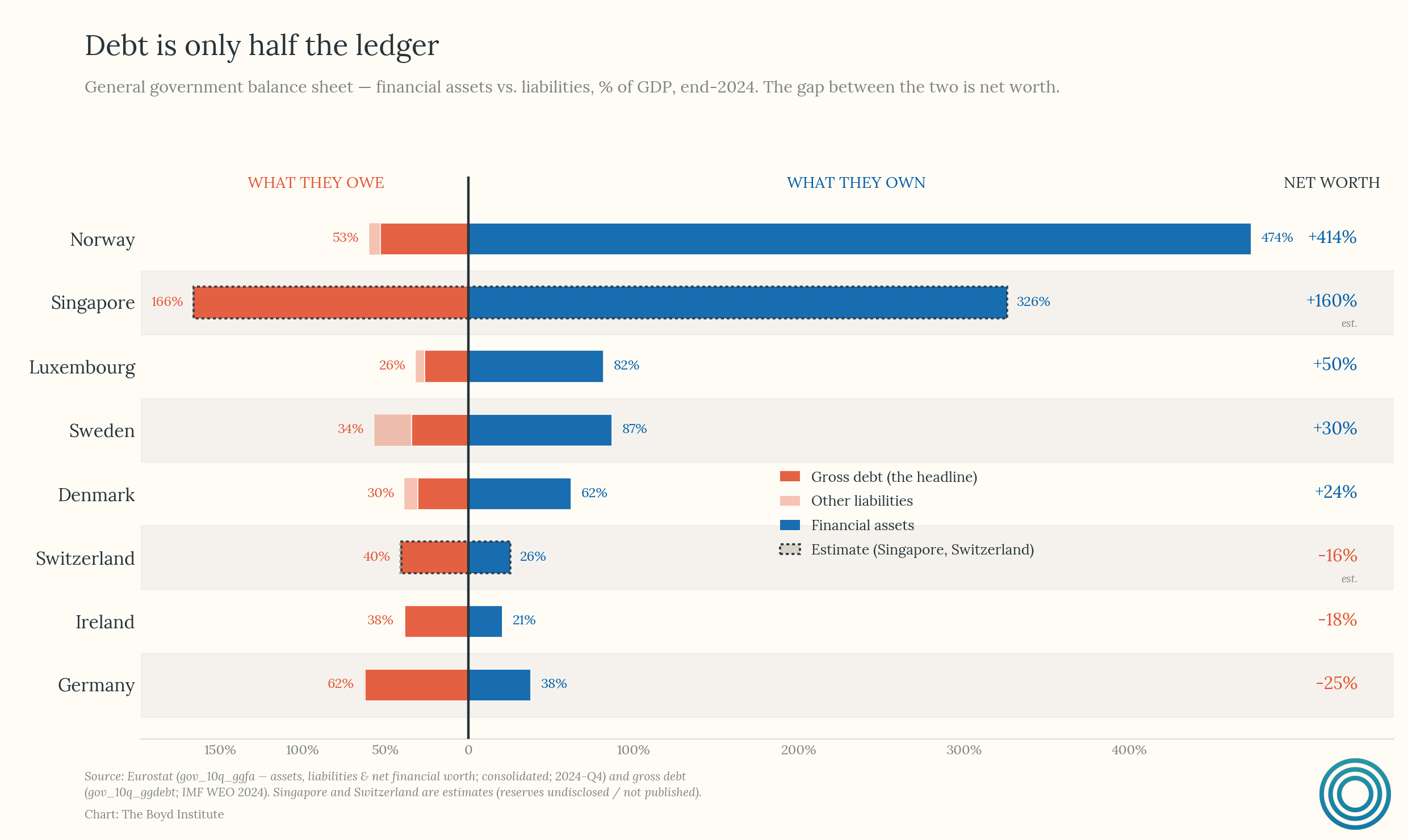

Indeed, while Norway’s gross government debt is 54% of GDP, its net public wealth remains positive because its financial assets dwarf GDP. What is unique about Norway among oil economies is not that it gives oil wealth to its citizens1, but that it places a strict 3% ceiling on how much of the oil fund can be withdrawn each year and invests the rest in a well-managed sovereign wealth fund.2

Singapore

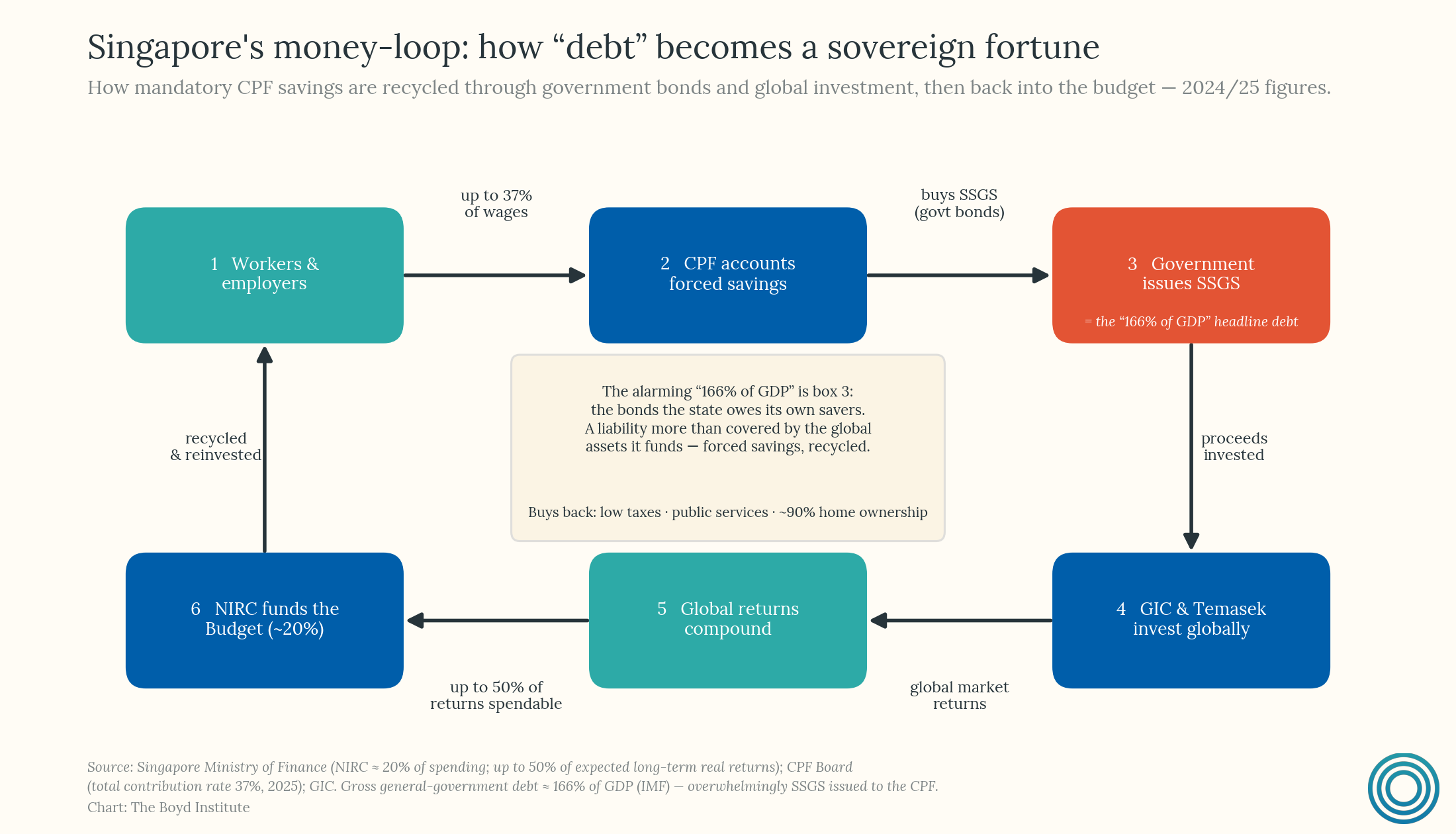

On paper, Singapore carries a surprisingly high debt-to-GDP ratio for a country synonymous with fiscal conservatism and technocratic governance. In reality, while Singapore’s debt-to-GDP ratio is 171%, most is held to manage reserves and fund compulsory savings rather than to finance deficits.. Like Norway’s, Singapore’s government holds assets well in excess of public debt and other liabilities.

The engine behind Singapore’s reserve accumulation is the Central Provident Fund (CPF), a mandatory savings scheme that functions as the country’s primary social security system. All Singaporean workers and their employers are required to contribute a portion of wages into individual CPF accounts. These funds are then used by the government, which issues Special Singapore Government Securities (SSGS) to the CPF at guaranteed rates, effectively borrowing the population’s forced savings. The proceeds are passed to GIC, one of Singapore’s sovereign wealth funds, for investment in global markets.

This mechanism is a large part of why Singapore’s gross debt figure appears elevated: the debt is not a sign of fiscal distress but rather the liability side of a balance sheet that is more than offset by investment assets. In this sense, Singapore’s “natural resource” is not oil or minerals but the institutionally captured savings of its workforce, intermediated through the state and deployed into global capital markets.3

Singapore’s constitution allows up to 50% of expected long-term real investment returns from reserves to be spent through the Net Investment Returns Contribution, and the state uses these revenues to fund approximately 20% of annual government expenditure. This allows Singapore to maintain competitive tax rates while still financing world-class public services.

Denmark and Sweden

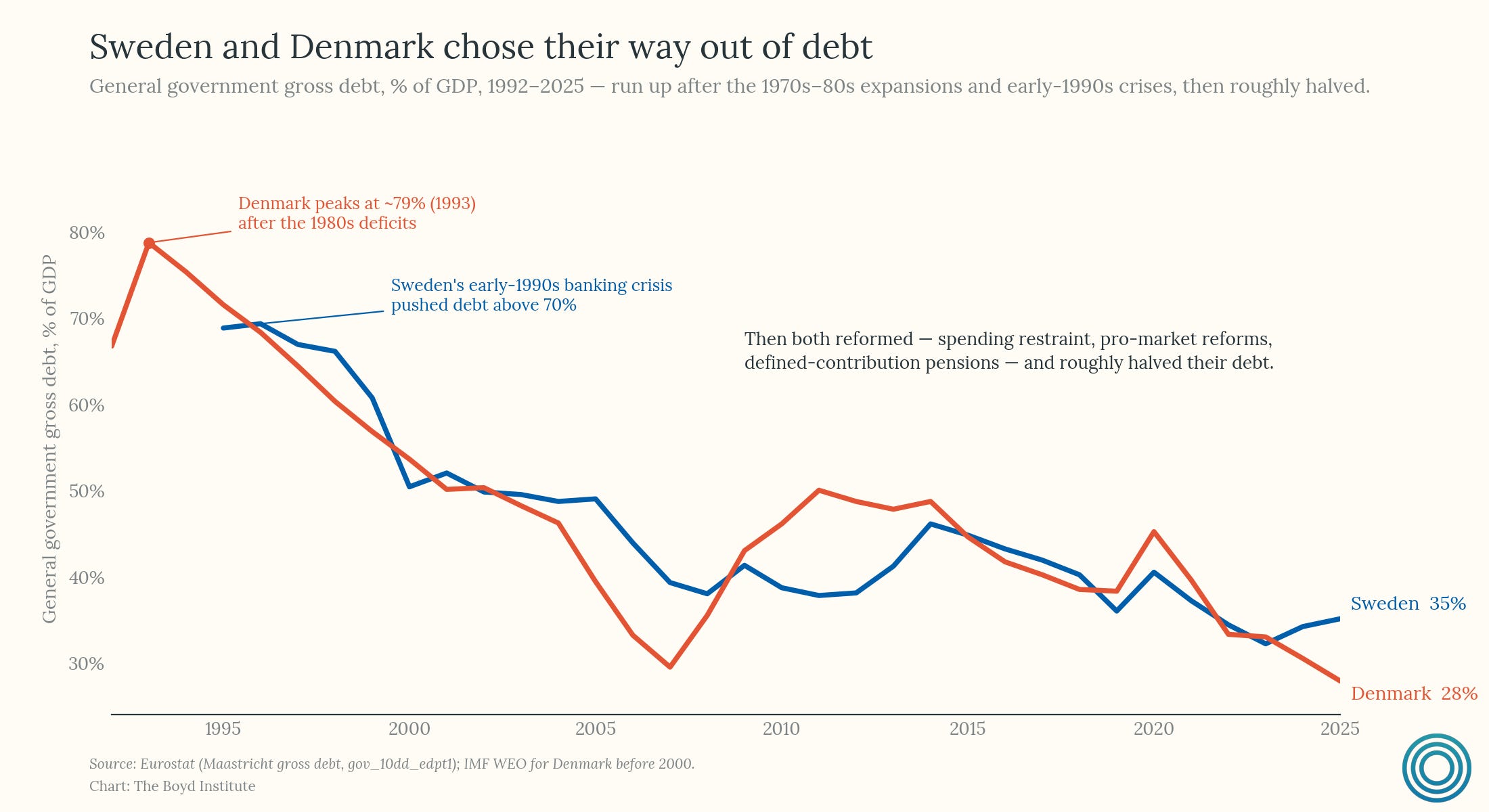

Like their oil-rich Scandinavian neighbor, Denmark and Sweden combine generous welfare states with strong growth and fiscal solvency. But this was not always the case. During the 1970s, both countries expanded public spending beyond what their economies could sustainably support, accumulating deficits. To change course, both nations (Denmark in the 1980s and Sweden in the 1990s) implemented pro-market reforms, spending restraint, and switched to defined-contribution pension plans.

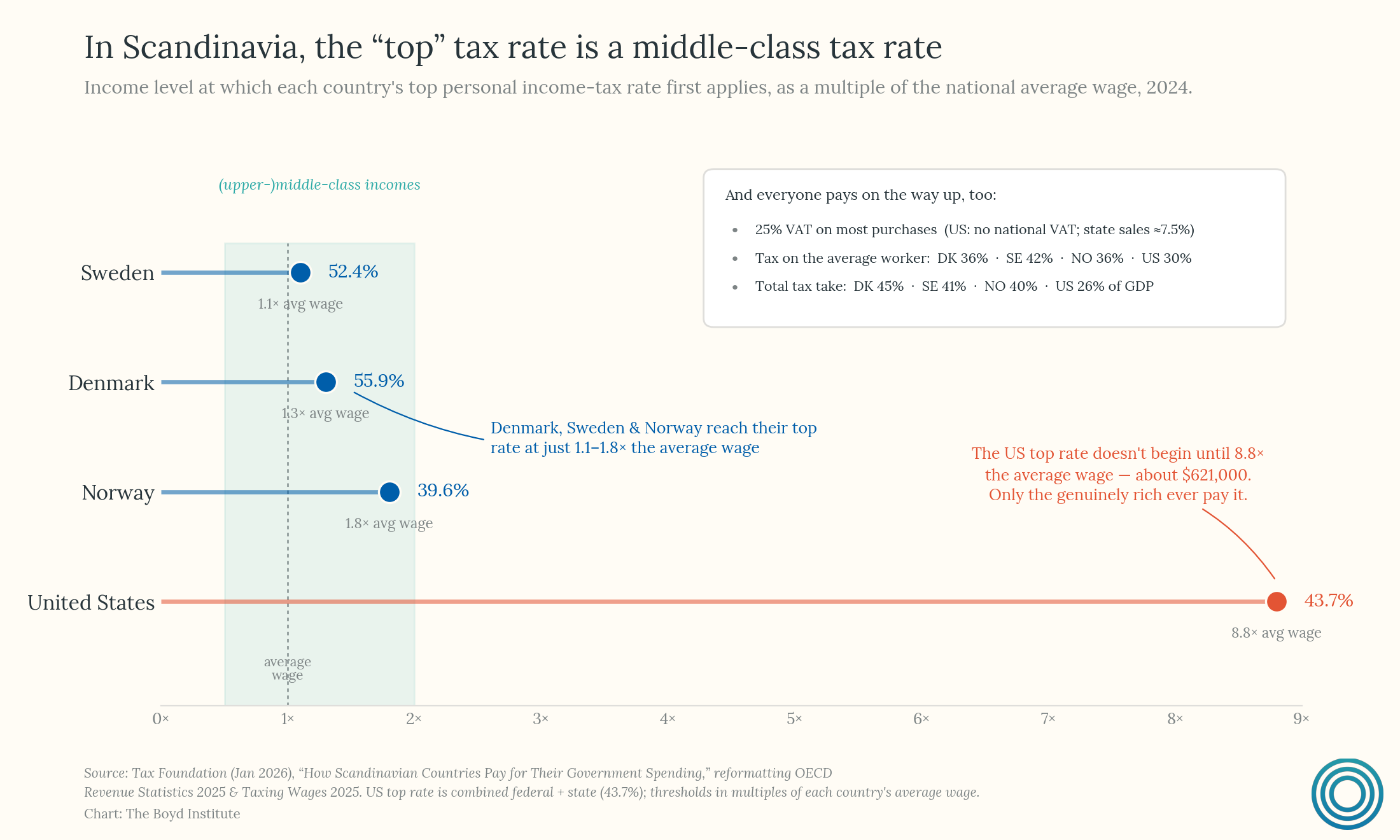

The breadth of their tax bases is the part Americans miss. Denmark and Sweden do not finance their welfare states by taxing the rich — by most measures their tax systems are less progressive than America’s. Both lean on 25% value-added taxes that fall across the income distribution, and their top income-tax rates bite at little more than the average wage compared to the US, where the top bracket doesn’t begin until roughly eight times average earnings.

The ordinary Scandinavian worker hands over a far larger share of his paycheck than his American counterpart. The equality Americans admire is real, but it is produced on the spending side — through universal benefits and services — not by soaking high earners on the tax side. That is the uncomfortable lesson: Americans want Scandinavian services and have shown no appetite for the broad-based taxation, consumption taxes above all, that pays for them. The Nordic bargain is simply “tax everyone, and spend it well,” not “tax the rich.”

Luxembourg and Ireland

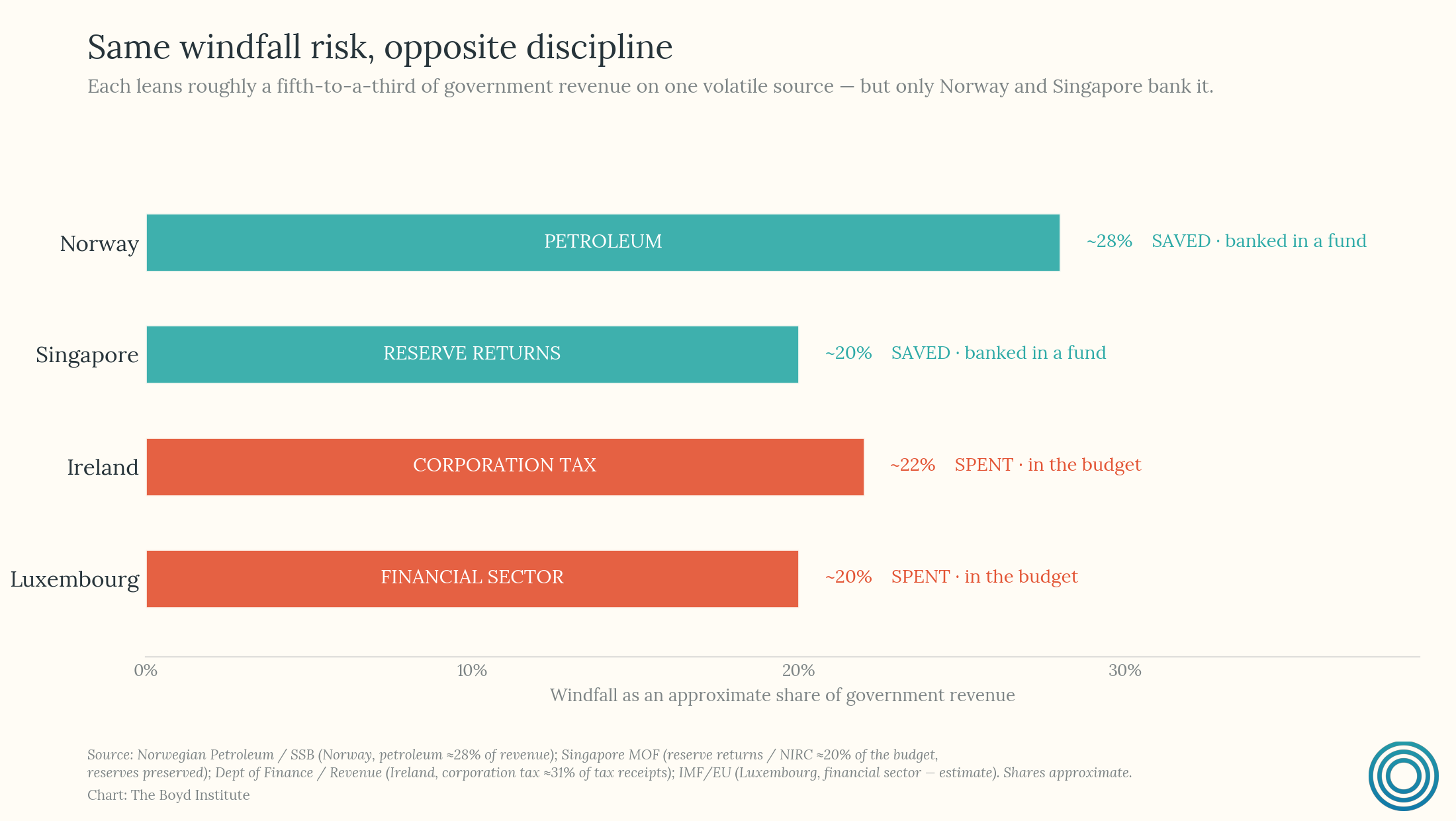

Norway and Singapore are not the only countries living off a concentrated windfall. Luxembourg and Ireland are too — the difference is what they do with it.

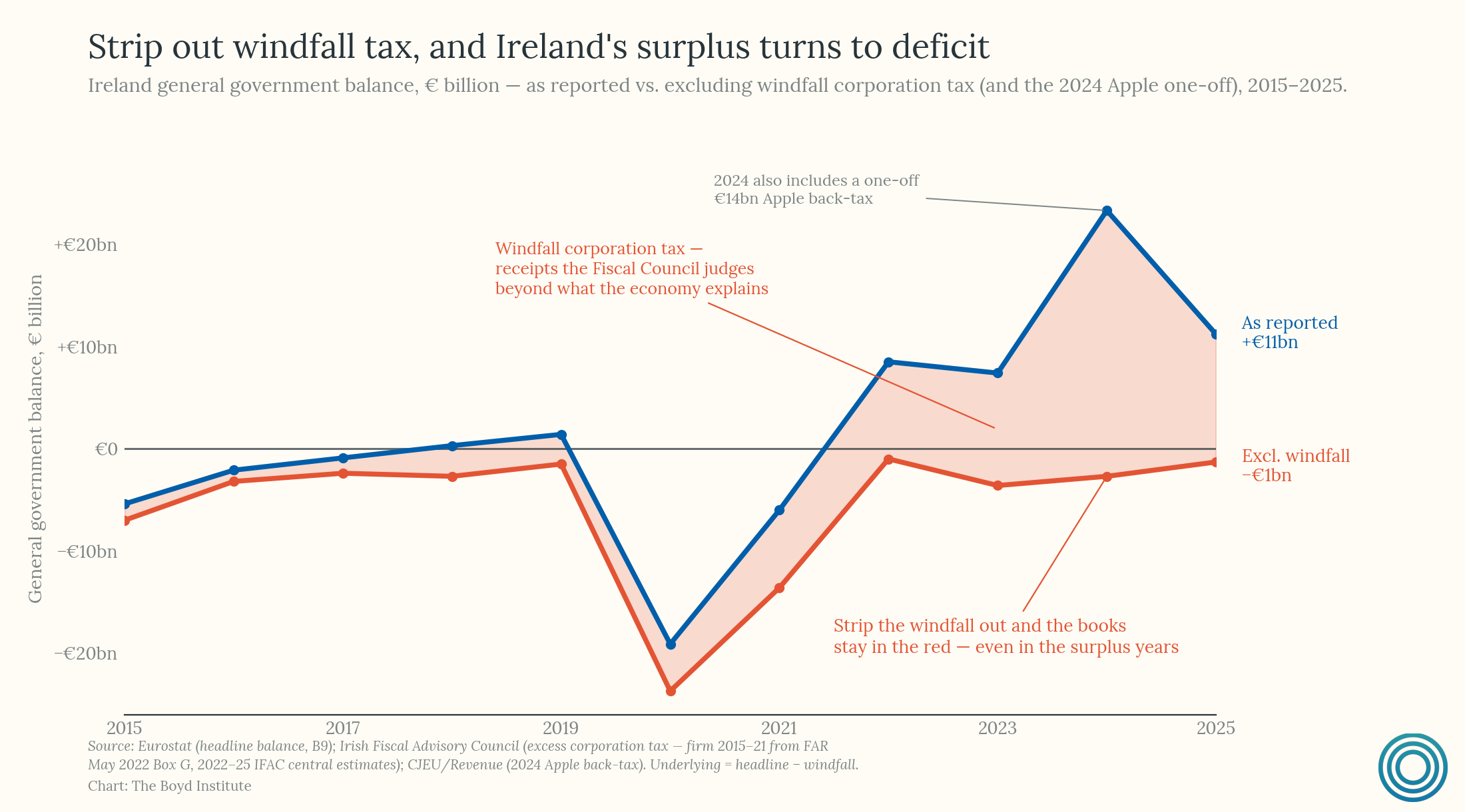

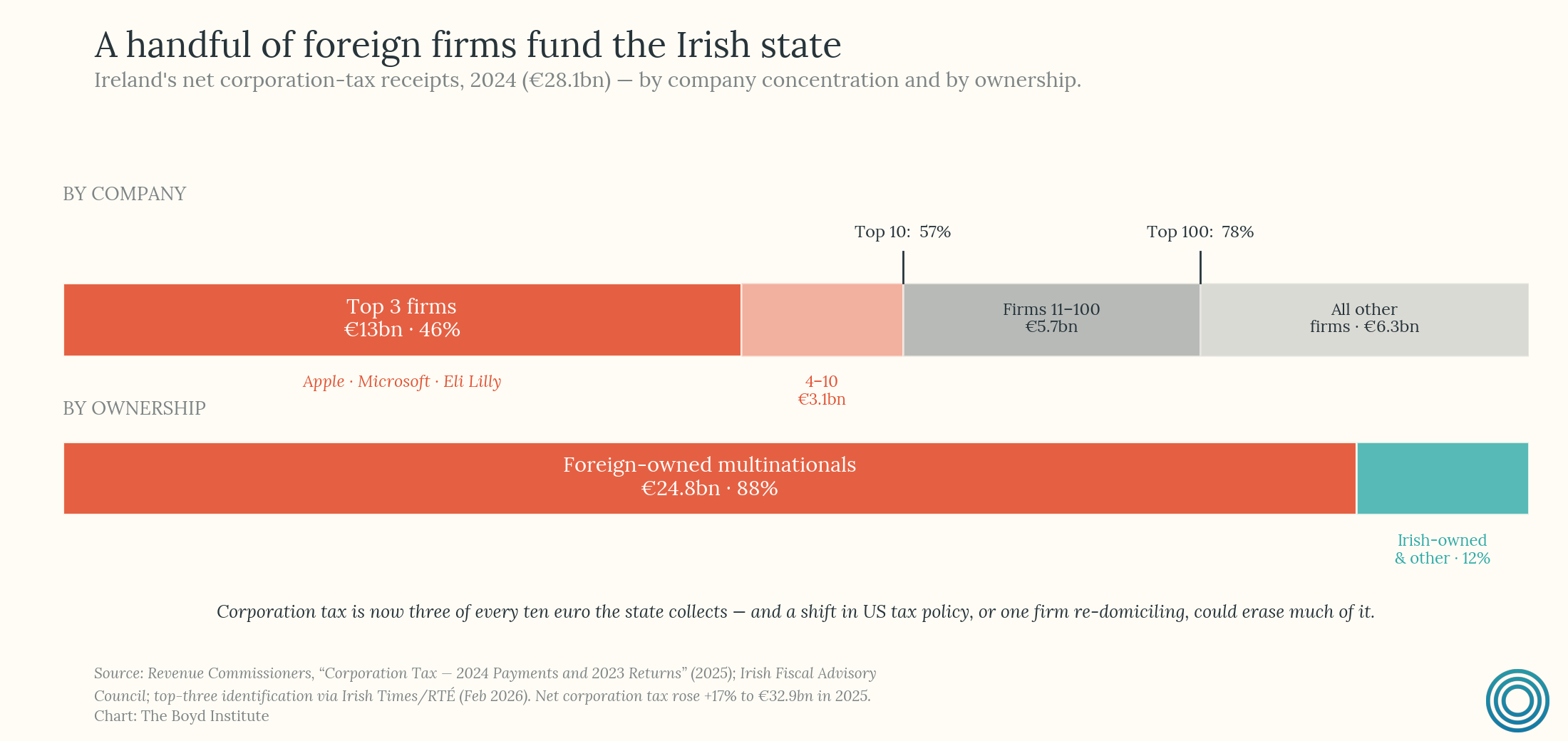

Luxembourg’s exceptionally strong sovereign balance sheet — with government debt of about 30% of GDP — rests on one of the world's most concentrated financial-services sectors, an industry that exists in large part because of its favorable tax and regulatory regime. Ireland's case is starker: it ran a budget surplus of approximately €12.4 billion in 2025 on corporation-tax receipts of about €33 billion, the bulk paid by a handful of large American multinationals booking global profits through Irish subsidiaries.

But where Norway and Singapore bank their windfalls and spend only the return, these two spend the windfall itself. Luxembourg runs its financial-sector revenue through the general budget, and Ireland — despite launching a Future Ireland Fund in 2024 — routes the large majority of its corporate-tax take, by its own fiscal watchdog’s estimate nearly 90%, into permanent commitments. Building lasting obligations on a windfall is a defensible bet only if the revenue is broad and durable. Ireland’s is neither — nearly half rests on the decisions of just three major foreign firms.

Germany

Germany represents perhaps the most instructive case for large advanced economies precisely because its fiscal strength was built not on resource windfalls or favorable tax geography, but on institutional self-discipline.

The rules and their origins

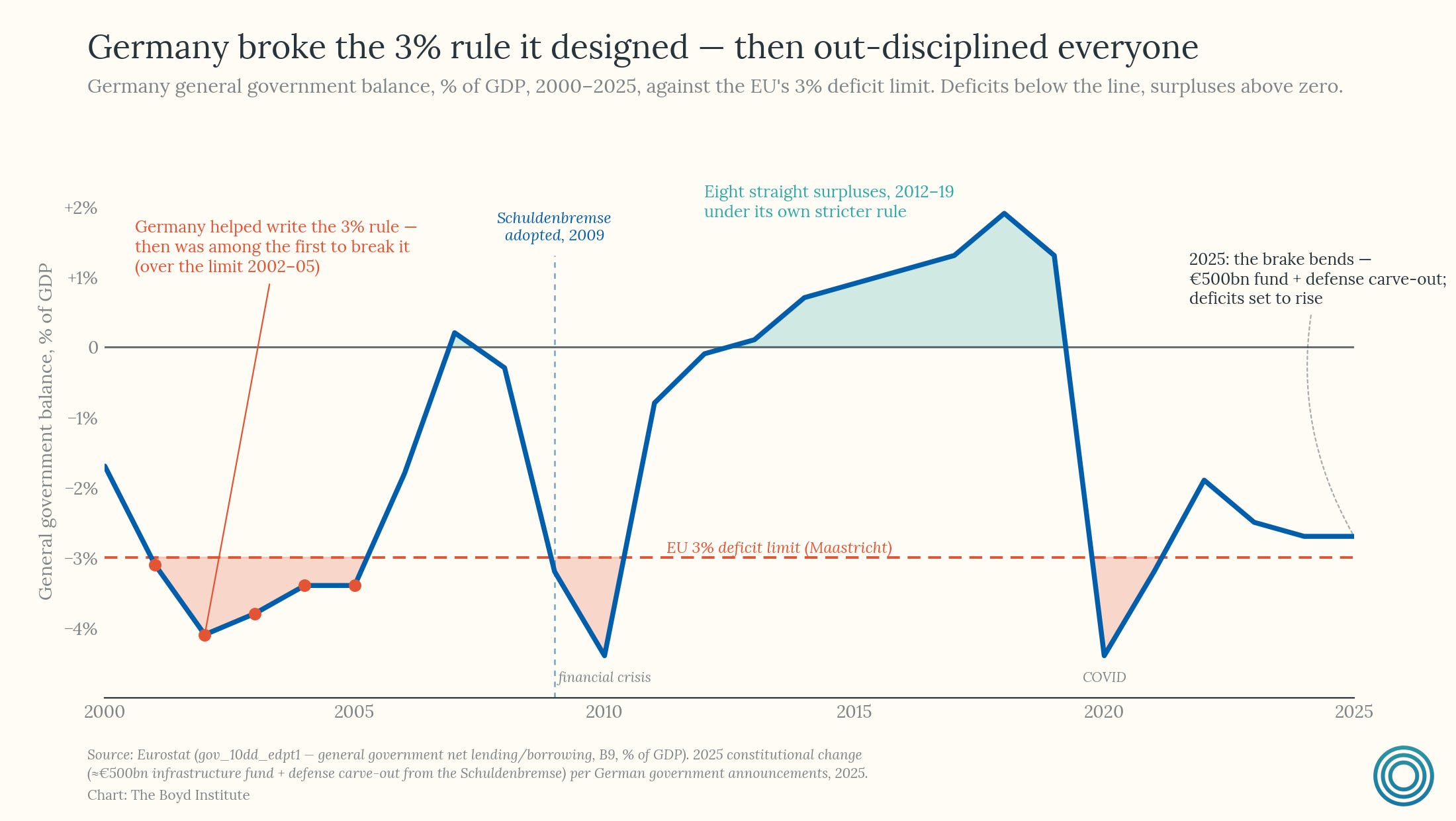

Germany’s Schuldenbremse, adopted in 2009 and fully binding on the federal government from 2016, caps the federal structural deficit at 0.35% of GDP. Alongside the “black zero” political commitment and a strong economy, it underwrote budget surpluses from 2014 through 2019 and cut public debt from roughly 82% of GDP to just below 60% before the pandemic intervened.

A nontrivial result of this is that German government bonds remain the euro area’s preeminent safe asset, a status that reflects deep market confidence in the country’s fiscal institutions.

Germany’s path to fiscal rules was shaped by reunification4, which required an estimated €2 trillion in fiscal transfers from west to east over three decades and structurally elevated debt through the 1990s. Combined with the low growth of that era — Germany was widely called the sick man of Europe by the late 1990s — these pressures produced the deficit overruns that became a political embarrassment: Germany breached the EU’s 3% ceiling in 2002, 2003, and 2004, making it one of the first prominent violators of the Maastricht rules it had designed. The Schuldenbremse was the response, intended to make recurrence constitutionally impossible.

The 2025 break

In early 2025, Germany’s newly formed government secured a constitutional exemption allowing substantially higher borrowing for infrastructure and defense. A €500 billion off-balance-sheet infrastructure fund was established alongside a carve-out exempting defense spending above 1% of GDP from the Schuldenbremse’s constraints — a response to years of underinvestment and the changed security environment following Russia’s invasion of Ukraine. The Schuldenbremse held for fifteen years and demonstrably shaped German fiscal behavior, but it bent under the combined pressure of geopolitical necessity and accumulated investment deficits. Whether 2025 proves a one-time correction or the beginning of a looser fiscal regime is the central open question in German public finance.

Switzerland

Switzerland's fiscal strength rests on both structural advantages and institutional discipline, making it a more complex case than it first appears, and one that sits somewhere between the pure rule-based model of Germany and the favorable-geography models of Luxembourg and Ireland.

Tax geography and the financial services sector play a meaningful role. Switzerland’s cantonal tax system creates internal competition that keeps rates low and has historically attracted both corporate headquarters and ultra-high-net-worth individuals. The country’s financial services industry — anchored by global private banking, asset management, and insurance — is outsized relative to the population and contributes substantially to government revenue.5

Equally significant is Switzerland’s long-standing role as a destination for wealthy European expatriates seeking relief from the higher tax regimes of neighboring countries. The lump-sum taxation regime (forfait fiscal) lets wealthy foreigners who do not work in Switzerland be taxed on notional living expenses rather than their actual worldwide income or assets — a provision that has drawn billionaires, executives, and high-net-worth retirees from France, Germany, Italy, and the UK.6 It is neither universal nor untouched — five cantons, including Zurich, have abolished it and the federal regime was tightened in 2016 — but it survives federally and in most cantons, giving Switzerland a revenue base that countries inside the EU's tax-harmonization framework cannot easily replicate.

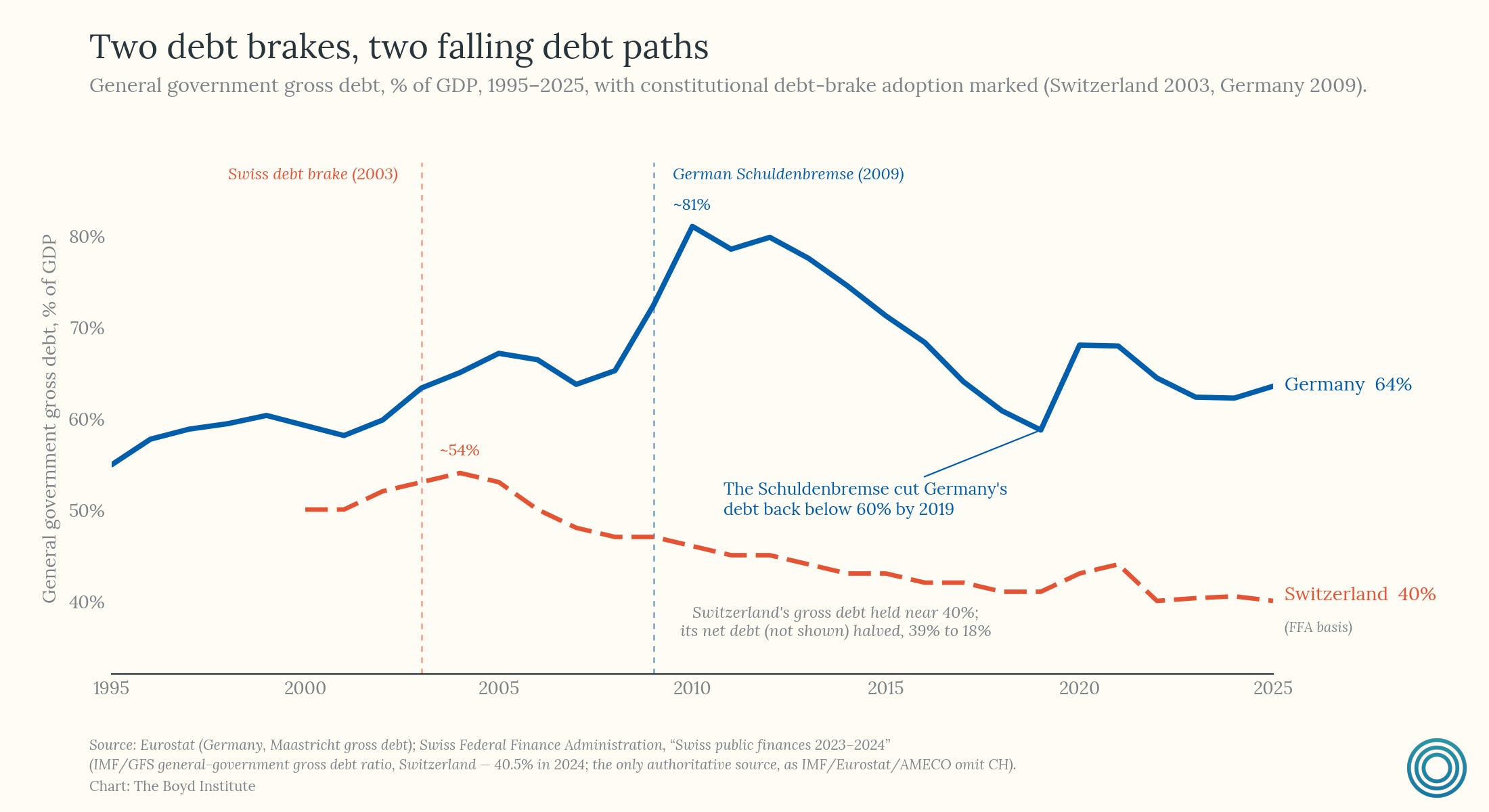

None of this is the whole story, though, because Switzerland also bound itself with a rule. A property-bubble collapse in the early 1990s dragged the economy into prolonged stagnation and pushed federal debt sharply higher; the resulting pressure of a stagnant economy and ballooning debt7 summoned a broad reform coalition, and voters ratified a constitutional debt brake by referendum in 2001. In force since 2003, it has driven federal net debt down to roughly 16% of GDP (among the lowest in the developed world) and delivered some of the cheapest sovereign borrowing anywhere.

So Switzerland is neither a pure story of self-discipline nor a pure story of luck. The structural advantages are real, even if less dramatic than North Sea oil; but the debt brake extended the discipline well beyond what those tailwinds alone would have produced.

Takeaways

Several takeaways emerge from this survey. First, headline debt statistics are frequently misleading. Norway’s gross debt understates its strength; Singapore’s dramatically overstates its weakness. What matters is the full balance sheet — assets as well as liabilities — and the quality and sustainability of the revenues that service them.

Second, windfalls should be treated as temporary until proven otherwise. Norway, Ireland, and Luxembourg all benefit from revenue streams that could diminish or disappear. The countries that have managed such windfalls most successfully are those that saved them rather than built permanent spending commitments around them.

Third, and most importantly for policymakers in larger democracies, fiscal discipline is primarily an institutional challenge, not a technical one. Switzerland and Germany did not stumble into strong public finances; they engineered them through constitutional rules that made profligacy harder and created political cover for restraint.

Similarly, Denmark and Sweden chose fiscal sustainability, at some political cost, after experiencing the consequences of not doing so.

The United States faces none of the insurmountable obstacles that might make these lessons inapplicable. It has no shortage of administrative capacity, no absence of credible institutions, and no lack of economists who understand what a sustainable fiscal trajectory looks like. What it has lacked, at least so far, is the political will to impose constraints on itself before markets demand it.

Of course, none of these analogues map cleanly onto the US — in terms of real economy and political economy — but the lessons from the countries examined here suggest that certain constraints, once adopted and sustained, can compound over time into something extremely valuable: fiscal space that provides security in crises, credibility in markets, and genuine fiscal optionality that heavily indebted nations do not tend to have.

Granted, although revenue from oil and gas production is transferred to the fund, these deposits account for less than half the value of the fund. Most of it is now capital appreciation — earned by investing in equities, fixed income, real estate and renewable energy infrastructure. [https://www.nbim.no/en/about-us/about-the-fund/]

Norway's restraint was a choice, not an instinct. When Phillips struck oil at Ekofisk in 1969, the country had no petroleum bureaucracy and no template for handling a windfall. Much of the framework that followed — state oversight, competitive licensing, majority Norwegian ownership — was shaped by Farouk Al-Kasim, an Iraqi-born geologist who had emigrated to Norway in 1968 and brought a warning drawn from Iraq's own squandering of oil. The Storting's 1971 "Ten Oil Commandments" codified the principle that the resource must serve "the entire Norwegian society"; the savings fund grew from that posture.

CPF savings can also be used to purchase public housing, which has produced one of the world's highest homeownership rates and ensures that asset accumulation occurs at the household level as well as the national level.

Germany's longstanding fiscal conservatism cannot be understood without understanding the trauma of monetary collapse. During the hyperinflation of 1921 to 1923, the Mark became so worthless that workers were paid twice daily and prices doubled every few days — an experience that left a cultural and institutional imprint persisting a century later. It discredited not just monetary recklessness but fiscal recklessness more broadly, embedding a suspicion of deficit spending into German political culture that has no real parallel among other large democracies. The Bundesbank's postwar obsession with price stability, and later German resistance to ECB bond-buying programs, both draw from the same source. The Schuldenbremse is the constitutional expression of that inherited anxiety.

Geneva and Zurich rank among the world's leading wealth management centers, and the secrecy and stability historically associated with Swiss banking have made the country a preferred domicile for internationally mobile capital.

While Switzerland has tightened these rules under external pressure and abolished the forfait in several cantons, the broader appeal of low cantonal rates, political stability, and high public services continues to draw high-earning residents who contribute disproportionately to the tax base.

Net federal debt rose from roughly 10% of GDP in 1990 to nearly 26% by 2000

In the Russia that we deserve, oil revenues will be similarly invested back into the nation.

The US is also doing better than debt to gdp suggests. We have higher taxable capacity by virtue of our great wealth.