MMT is dumb, and dangerous

The "infinite money glitch" that never was

The proliferation of Modern Monetary Theory (MMT) always struck me as odd. Like many contemporary artworks, or like Beyoncé winning a Grammy for country album of the year, you can see how we got here, yet it feels no less blasphemous.

What follows is the story of how MMT’s central operational claim — that government bond yields are a policy choice rather than a market outcome — went from fringe heterodoxy in the 1990s, to operational practice under Ben Bernanke’s Fed, to the “new normal” by the late 2010s, to the foundation of a roughly fifteen-year experiment in what monetary policy could be made to do.

It is also the story of how that experiment was rapidly dismantled in 2022 when inflation came back, and how the constraints the framework had insisted no longer applied came rearing back with a vengeance. We are now living inside the institutional wreckage of the MMT experiment.

Infinite money glitch?

MMT starts from a premise that’s true — that a government issuing debt in its own currency is not financially constrained in the way an individual or household is, nor even the way a eurozone member (e.g., Greece) is. Such an unconstrained government — one that controls its own currency — can always create new money to service its obligations. So, in the MMT view, the real limit on deficit spending lies in the economy’s productive capacity and inflation, not in the mechanical question of whether a sovereign bond auction “goes through.”

The post‑GFC world seemed to validate this. When Treasury markets buckled in 2008, and again under stress episodes since, the Federal Reserve’s expanded policy toolkit — large‑scale asset purchases / an ever more elastic repo backstop — meant that failed or fragile Treasury auctions could be rescued with Fed support. The central bank could, in practice, ensure that the government’s paper cleared by just… buying it!

From this, MMT draws its central claim: deficits are effectively self‑financing as long as the interest rate on government debt remains a policy choice rather than a market outcome.

If that is true, a rationale emerges for running up debt and deficits. If interest rates and demand for government debt can be set by policy rather than discovered in markets, why shouldn’t policymakers simply set parameters such that the cost of financing deficits is minimized? And, pushed one step further, why should ballooning national debt be thought of as a problem at all?

The answer, if simple, is a rejection of the premise: policymakers can influence rates for a time; but alas, they cannot control them forever. So the wrongness of the whole MMT rationale is not in its chain of reasoning but in the core premise itself.

The wrongness of MMT also lies in its sleight of hand about how deficits are actually funded. The economist Stephanie Kelton’s 2020 book, The Deficit Myth, was profoundly influential in the popularization of MMT. In it, she invites readers to see the government’s budget constraints as — and I’m slightly paraphrasing here — fake and gay. In her cartoonish telling during a 2025 podcast appearance:

“The government’s bank, its fiscal agent, is the central bank in the US — that’s the Federal Reserve. And the Federal Reserve’s job is, in part, to carry out the payments that have been authorized by Congress on behalf of the US Treasury. Now ask, how does it do that? It uses a computer keyboard to change the numbers in the appropriate bank accounts. It types them in, and that’s where the money comes from.”

What Kelton is saying is technically accurate at the settlement level. She’s referring to the Treasury General Account (TGA), the checking account Treasury uses at the Fed. But the extremely important and existential caveat she neglects to mention is that Treasury cannot run an overdraft at the Fed; the TGA must — legally — have a funded balance in order for the transfers to clear. And that balance is funded by taxes and debt issuance, not by the Fed arbitrarily deciding to credit the account.

Kelton goes on:

“But that’s the strength of MMT, is that we’re willing to have that honest conversation so that we don’t talk to people as if they’re children. We don’t dumb it down and pretend as if the government has to go out and find money and collect it from rich people or other taxpayers or borrow it from savers. They create the money in the act of spending, and that’s just how it works.”

So MMT suggests that the government can always conjure money out of thin air to finance its spending, and that “that’s just how it works,” by essentially collapsing Treasury and the Fed into a single entity.1 This consolidated view is the load-bearing assumption of the entire framework. When the government spends, it issues new liabilities to the private sector, and bond sales just swap one form of government IOU for another. In such a view, one where money basically lacks scarcity, Treasury bond issuances must be nothing more than a trivial formality.

But in order for a Treasury auction to be considered trivial, there needs to be a… what? A guaranteed buyer.

It’s QE all the way down

Now, former Fed Chair Ben Bernanke would hardly characterize himself an MMT-adherent. Even at its peak in popularity, MMT carried a certain stigma within serious policy circles. But he oversaw the operationalization of its central intuitions — that the Fed can always just “change the numbers in the appropriate bank accounts,” and that rates and government bond yields are a policy choice, not a function of market discovery. He oversaw the transition of these tenets from MMT-derived intuition to institutional imperative — and ultimately institutional instantiation.

In the throes of the financial crisis, inducing relief via conventional monetary policy had run out of room at the zero lower bound — short-term rates being held “lower for longer” was unlikely to provide enough easing of financial conditions for the economy to recover. Fiscal stimulus was authorized by Congress in short order, but beyond the scope of ZIRP existed a real gap: the risk of a bond market rejection of Treasury’s post-GFC stimulus packages.2 (That is, the risk that not enough investors show up to bid in a Treasury auction and yields soar.)

Bernanke’s Fed opted to plug this gap with what, at the time, was a radical experiment: quantitative easing (QE), or the large‑scale purchases of hundreds of billions (and eventually trillions) in securities by the Fed. It was designed to stabilize key fixed income markets like Treasuries and agency MBS — and, by extension, the real economy — by suppressing longer term rates3 when short-term rates were already pinned at zero. It was designed to make money cheap, the wholesale way.

In practice, it seemed to be working extraordinarily well. Treasury was able to seamlessly finance a litany of massive spending bills and corporate bailouts with newly issued long-term paper. This coincided with markets stabilizing and the real economy recovering to new highs in shockingly short order.

The technical reason QE worked in those moments of economic desperation is pretty straightforward: the Fed stopped merely influencing government borrowing rates and started being the marginal buyer of the actual debt. Krishnamurthy and Vissing‑Jorgensen (2011), looking at the first couple tranches of QE, estimated that the programs reduced longer‑term Treasury yields on announcement by on the order of 90 to 200 basis points across maturities, with much of that effect coming through lower term premia rather than changes in expected short rates.4

More recent work by Haddad, Moreira, and Muir (2025) pushes this further. In models where asset purchases follow transparent rules, QE not only generates a one‑off “stock” effect from absorbing bonds, it creates an insurance effect, because investors come to expect that the central bank will step in whenever stress emerges. (A lasting axiom on Wall Street is that you simply “Don’t fight the Fed” — if the central bank is buying en masse, you, the investor, should be too.) That expectation, according to the empirical literature, lowers term premia by something on the order of 75 to 100 basis points on a persistent basis, transforming long‑dated Treasuries into an unusually safe, quasi‑insured asset.

Pre‑QE, the basic relationship was simple: more long‑dated debt relative to GDP and income tended to mean higher long‑term yields, because someone had to be compensated to hold the extra duration. But with what seemed like a defensible proof-of-concept, successive rounds of quantitative easing — including and especially the pandemic-era “bazooka” — coincided with lower long‑term yields, tighter credit spreads, and a decade (plus) in which debt service costs stayed low even as public debt soared.

Under this new normal monetary regime, the Treasury market supply‑yield relationship has meaningfully weakened and sometimes even inverted.5 As the Fed absorbed duration from the market, increases in Treasury supply — new government debt issued — no longer showed up as higher yields to the same degree. Indeed, the QE era of cheap debt was a heyday for borrowers abound, not least governments.

However, the problem that arises when the entire monetary environment hinges on the existence of an infinite buyer of last resort to artificially suppress rates is… What happens to the party once the music stops and the punch bowl is taken away?

The permanent emergency

By the late 2010s, the circular monetary apparatus had been running long enough that a generation of economists and policymakers had come to treat it as the infinite money glitch MMT suggested it was. Minneapolis Fed president Neel Kashkari, in a 60 Minutes interview in 2020, said as much and was subsequently meme’d into oblivion:

At the time he was simply voicing the prevailing consensus among his peers at the Fed, in academia, and on Capitol Hill. Inflation had remained stubbornly below the Fed's 2 percent target for nearly the entire decade despite the central bank’s balance sheet having swelled from under a trillion dollars to over four. The “natural rate of interest,” by some estimates, had drifted toward zero or below.6

Also around this time, former Treasury Secretary Larry Summers popularized the secular stagnation thesis, which framed chronic demand shortfall and depressed real rates as a structural condition rather than a transient post-GFC phenomenon. Olivier Blanchard, in his 2019 American Economic Association presidential address, argued that when the safe interest rate sits persistently below the growth rate, the fiscal cost of public debt "may be zero" — giving MMT's practical conclusions academic respectability without requiring anyone to sign onto MMT itself.

The professional mood had shifted decisively. Many well-respected economists — famously Paul Krugman, Nobel laureate for trade theory turned blogging polemicist — argued time and again, sparing no conviction, that the US had entered something like a post-inflation world.7

Meanwhile those who dissented, voicing caution around the insistence that rates could remain "lower for longer" indefinitely, or warning that the explosion in money supply would eventually spell inflation, were sidelined.

Kenneth Rogoff, the Harvard economist and former IMF chief economist (and chess grandmaster!), was among the most prominent dissenters. Throughout the 2010s he warned that ultra-low rates and subdued inflation were not the new permanent state of the world, that mounting debt loads would constrain monetary policy when inflation eventually returned, and that a regime of "fiscal dominance" — where central banks lose the operational freedom to fight inflation because tightening would crater government finances — was the foreseeable consequence of complacency. The profession was, by and large, uninterested.8

Indeed, the dominant worry was no longer debt sustainability or an inflation-inducing overheating of the economy, but under-investment, insufficient fiscal support, and the risk of a Japan-style deflationary trap. In other words, the emergent consensus held that the primary constraint on fiscal policy was political dogma rather than economic fundamentals.

The most telling expression of this consensus was the discussion of “yield curve control” (YCC) — first posed at an FOMC meeting in July of 20199 — as the natural next step in expanding the central bank’s toolkit. YCC, essentially, is the explicit operational endpoint of MMT's logic: rather than influencing long rates indirectly through asset purchases, the central bank simply “names” target yields across the curve — not unlike how it “names” its Fed Funds Rate target range — and commits to buying or selling whatever quantity of bonds is necessary to enforce their target yields.

Mind you, this discussion was taking place during a time of all-time highs in markets, historically low unemployment, and a genuinely broad-based economic expansion in the US. Nevertheless the Bank of Japan had been running a version of YCC since 2016. And the Reserve Bank of Australia adopted it in 2020. The Federal Reserve, under Powell, openly studied whether to follow. The discussion was framed as the natural extension of what QE had already accomplished — and at the time, it was hard to convincingly argue otherwise. If the Fed could already suppress rates on the long end of the yield curve through purchases, why not just do it explicitly?

The distinction between MMT's operational claim and Fed practice had, by this point, functionally collapsed. What had begun as an emergency response to the 2008 crisis was now being theorized as the permanent architecture — the “new normal” — of monetary policy.

In the end, the Fed never formally adopted YCC. It didn't need to. When the pandemic hit, it launched a round of asset purchases that dwarfed every previous QE program combined; its balance sheet ballooned from roughly $4 trillion in early 2020 to nearly $9 trillion by 2022, with the Fed at one point absorbing nearly the entire net new issuance of long-dated Treasuries.

The effect on the yield curve was indistinguishable from what an explicit YCC regime would have produced. Long yields stayed pinned near historic lows even as the federal deficit hit double-digit percentages of GDP and Treasury issuance reached unprecedented levels. The Treasury market’s supply-yield relationship, already weakened by a decade of QE, had broken entirely.

And so for a moment in 2020 and 2021, the MMT project looked not just empirically validated but operationally complete. The Fed had demonstrated that it could absorb essentially any level of Treasury issuance the federal government chose to throw at the market without yields rising. The framework's central premise — that long term rates and demand for government debt are a policy choice rather than a market outcome — appeared to have been confirmed at scale.

Then came inflation and the infamous “Fed pivot.”

The reckoning

By mid-2022, headline inflation was running above nine percent and was top of mind for every American in a way that the country hadn’t seen since the 1970s. Many of the same voices that had spent the previous decade arguing for ever‑higher government spending backed by a complaisant Fed treated the surge as “transitory” — that is, a supply‑chain story, a base‑effect story, a one‑off energy shock. The honest accounting is that "helicopter money" — the trillions in post-Covid fiscal stimulus absorbed by the Fed’s balance sheet — created a demand shock that drove a meaningful share of the inflation. Larry Summers, to his credit, was an early and loud dissenter from the “it’s transitory; keep printing the money” consensus.10 Most of the profession was not.

Eventually, given the Fed’s pesky dual mandate, and given that the economy had already returned to full employment, the inflation reality forced a break with the MMT script. The Fed raised rates at the fastest pace in four decades and began letting its balance sheet run off (i.e., “quantitative tightening”). The “infinite money glitch” was no more.

Predictably, long yields backed up, the supply‑yield relationship reasserted itself, and the comforting assumption that the central bank could always keep debt service cheap evaporated. This was Jerome Powell’s belated Volcker moment, which was, in effect, a rejection of MMT’s core promise. But by then the emperor had already spent a decade without clothes.

In principle, what the yield curve is supposed to reflect is the market's collective expectations about growth and inflation, plus a term premium tacked on for the risk of getting either wrong. For most of the QE era, it reflected something closer to the Fed's preferences than the market's expectations. Today it remains unmoored from conditions in the real economy — only this time the distortion runs in the opposite direction, with long yields elevated above what market-based growth and inflation expectations alone would justify.

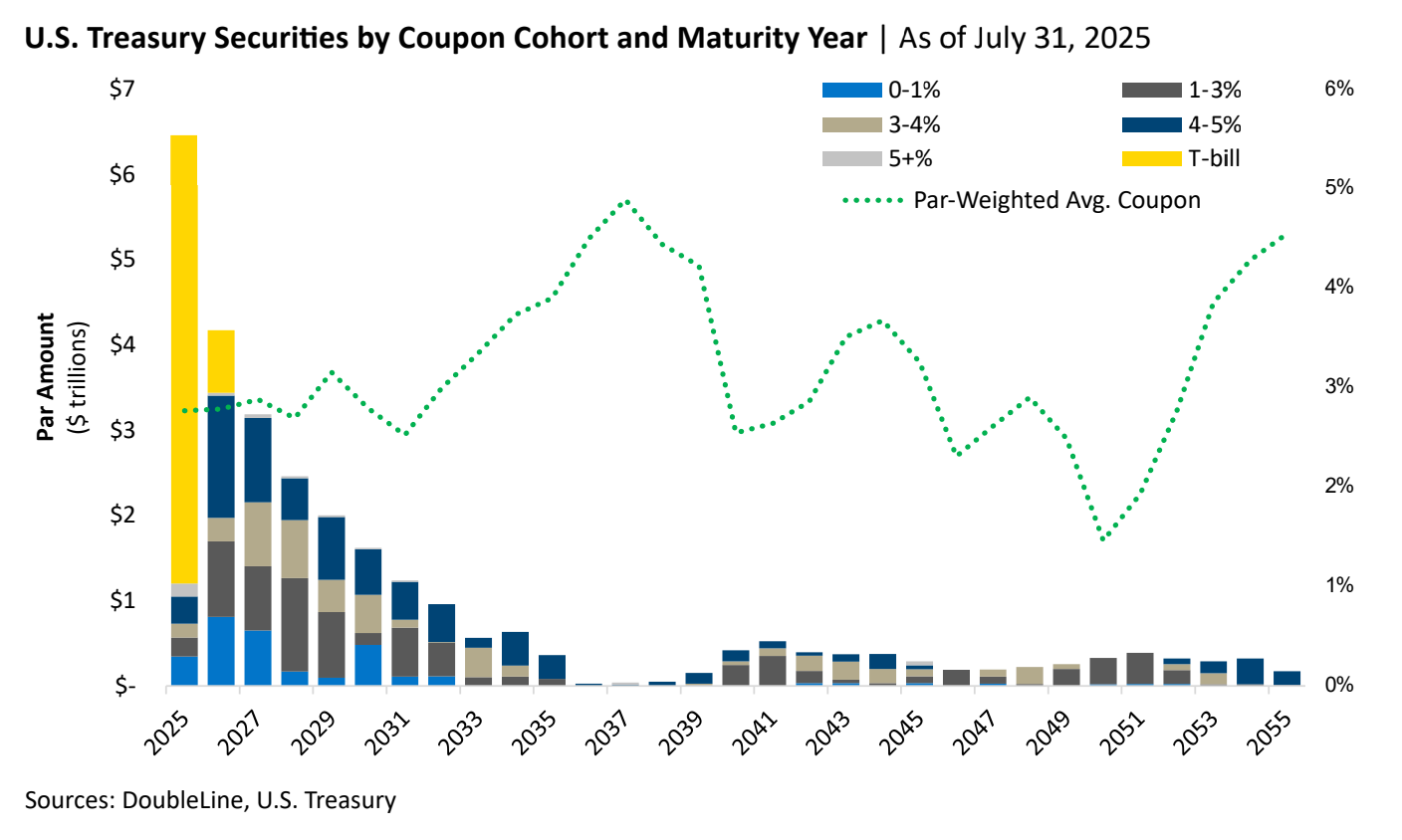

That distortion now collides with a very old-fashioned constraint: maturity. The QE era provided a golden window for issuing long-dated debt, and Treasury did. But that paper is now rolling off into a "maturity wall" — trillions in long-dated debt issued during the cheap-money era reaching maturity over the next 5-7 years — at exactly the moment when long yields are again expensive relative to growth and inflation expectations.

Treasury has responded the only way it can: by leaning heavily on T-bill issuance, refinancing maturing long paper with short paper rather than locking in current long rates. This is perhaps rational debt management given the menu of options available, but the structural consequence is that an ever-larger share of the federal debt stack now reprices continuously at the short-term spot rate (the one rate the Fed can actually control outright). Given that the entirety of the yield curve is now well above the rates on Treasury’s maturing debt, the weighted average interest rate on its outstanding debt is climbing — and is likely to continue climbing — as more long-dated paper rolls off and gets refinanced at a higher rate in the spot market.

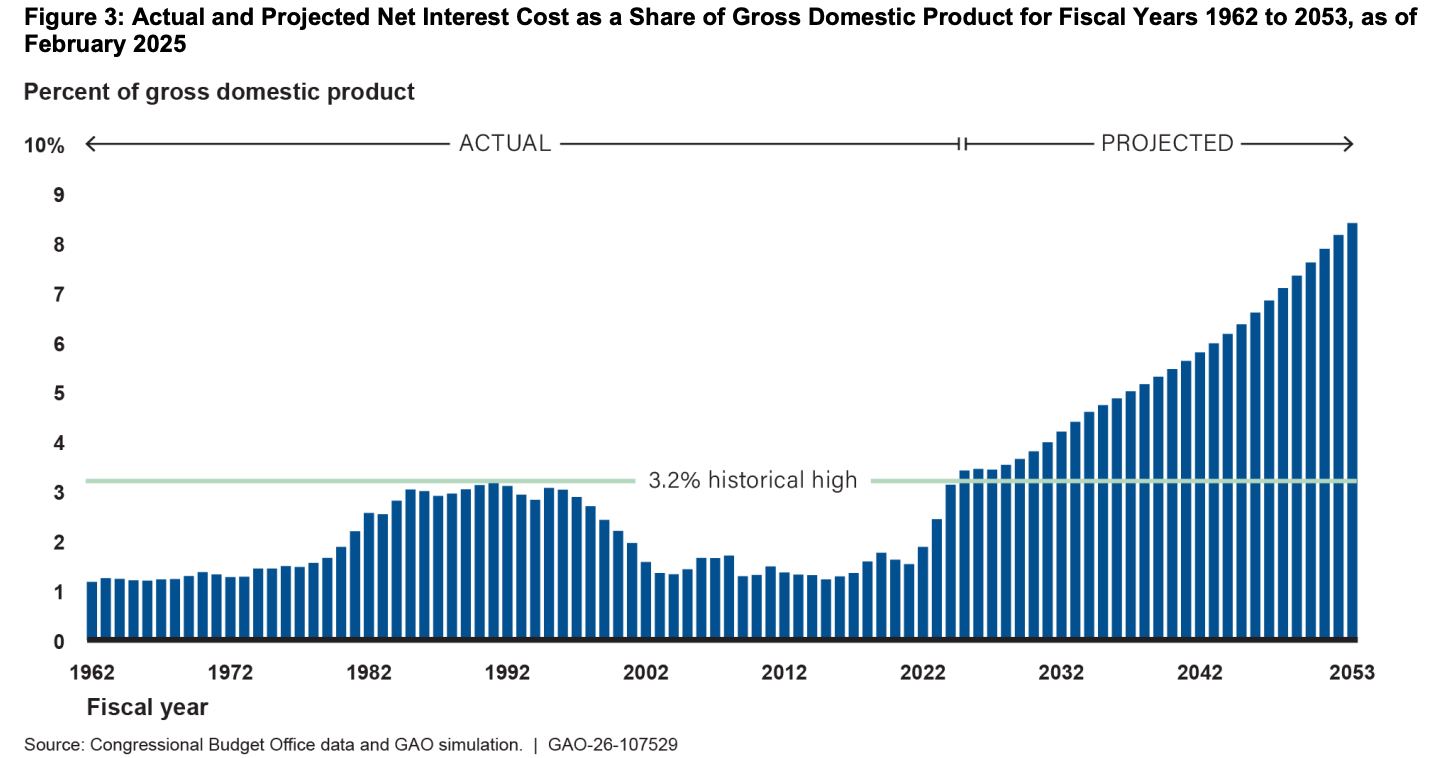

Translation: interest payments as a % of GDP will continue soaring and are projected to eclipse 8% by 2050:

What the MMT framework's adherents are now reckoning with — to the extent they are reckoning at all — is that the “infinite money glitch” apparatus not only failed to predict the reckoning, it is now feeding the reckoning. It also created a dangerous potential credibility loop for the Fed (which is set to undergo a leadership change in May):

Higher Treasury yields → higher federal interest bill → political pressure on the Fed to ease → erosion of Fed credibility → still higher yields

Any way we slice it, the US is now staring down the barrel of a vicious cycle that many an emerging market central bank has feared — and unironically one that developed market central banks have historically been able to ignore. The reason the US can no longer ignore it is precisely because of the institutional architecture MMT gave license to: a Fed balance sheet still north of seven trillion dollars, a government debt stack with rapidly shortening average maturity, and a federal interest expense that continues to grow faster than any other major budget category.

The framework's adherents argued for fifteen years that we had transcended the constraints of money. We had not. We had only suspended them, and the suspension came with a bill that compounds.

Conclusion

Milton Friedman was the godfather of monetarism, which claims that the supply of money is the first order determinant of inflation. He famously characterized monetary policy as having “long and variable lags.” While this was accurate when he said it, monetary policy no longer bites fiscally with a long lag as old long-dated paper slowly rolls over. In the new paradigm created by the operationalization of MMT, monetary policy bites immediately.

This is the part of the post-monetarism legacy that its architects never really reckoned with. The framework's central operational claim — that the central bank can keep rates suppressed and remain a perpetual buyer of government debt — works in only one direction that can be sustained as long as inflation stays dormant. The moment inflation arrives, the Fed must do one of two things:

Abandon its dual mandate of maximum employment and price stability; or

Do the exact opposite of what the MMT framework prescribes: tighten financial conditions, become a net seller of government bonds rather than a net buyer, and absorb whatever fiscal pain that creates.

In other words, absent the erosion of central bank independence, there is no version of the MMT apparatus that survives a return of inflation, because containing inflation definitionally requires dismantling the apparatus.

When that happens — and 2022 demonstrated that it can and does — fiscal policy had better be in a position to absorb the shock. That is, the federal government had better not be running large structural deficits financed primarily by short-dated debt that reprices continuously with the policy rate. Unfortunately but not surprisingly, this is the exact position the United States now finds itself in. Interest payments are already the fastest-growing line item in the federal budget. The maturity wall guarantees they will keep growing for at least the next several years, regardless of what the Fed does next. And every basis point of additional Treasury yield — whether driven by inflation expectations, term premium expansion, or the credibility loop discussed earlier — translates almost immediately into additional fiscal cost.

Which brings us to a strange but necessary reframe. We typically think of taxes as a way to fund government spending. But under the post-monetarist apparatus, with the monetary lever now exhausted and the fiscal stack vulnerable to every Fed decision, taxes have to be reconceived as something else as well: the only remaining policymaking tool with which to combat inflation. Higher taxes pull spending power out of the economy, which is exactly what the central bank is trying to do when it tightens — only without compounding the federal interest bill in the process. This is not a politically convenient conclusion. It is, however, where the math leaves us.

The architects of MMT’s institutionalization (Bernanke chief among them) myopically argued for fifteen years that we had transcended the constraints of money. We had merely suspended them. And the cost of resuming them, having let the apparatus run for as long as we did, is going to be paid one way or another — through inflation, through fiscal contraction, through monetary tightening, or through taxes.

The only remaining question is which combination, and at what political cost.

More from the Boyd Institute’s ongoing sprint on debt & deficits:

Debt for Dummies

People talk a lot about debt in vague technocratic language that is both needlessly confusing and obfuscatory. So today I want to explain how the US debt actually works in layman’s terms and why paying so much in interest is bad.

The Fiscal State of the US, in 12 Charts

As we ramp up our new sprint on America’s debt & deficits crisis — yes, “crisis” would be an apt characterization — we thought it would be useful to start with a high-level overview of the fiscal problems facing the country. And what better way to set the scene, we asked, than with some charts? So, here’s 12 of them, weaved together with some commentary.

How Do We Avoid the Fiscal Cliff?

The Q1 sprint on America’s problem-solving capacity has wrapped up, and we want to thank everyone who participated. Quite a few of the ideas generated in our essay contest — in particular Sol Hando’s submission — were both actionable and important, and so we don’t plan on just dropping the topic but instead hope to continue pushing on it. However, it is…

Yes, long before Donald Trump’s rate cut rhetoric was considered a “threat to central bank independence,” MMTers posited that the Fed should functionally have no operational autonomy, its dual mandate be damned.

If a Treasury auction lacks a bid from investors, yields will rise until they are compelling enough to attract a bid. And that extra yield comes straight out of the taxpayer’s pocket.

A bond’s rate/yield is inversely related to the underlying bond’s price. So, all else equal, when a bond gets a bid to buy, the bond price goes up and the rate/yield falls.

“Term premia” is jargon for the additional yield bond investors demand for taking more duration risk. Longer maturities = more duration. The core finding of the study was that when a large, price‑insensitive buyer removes duration risk from the market, the extra yield investors demand for holding long bonds falls.

Haddad, Moreira, and Muir (2025) argued that in the post‑QE era long‑term Treasury yields appear “too low” relative to debt supply, consistent with a weakened supply–yield link.

A 2020 NBER working paper by He, Nagel, and Song titled “Treasury Inconvenience Yields during the COVID‑19 Crisis” discusses the Treasury market maker of last resort, and addresses unusual pricing around supply surges.

A 2020 paper authored by Fernando M. Martin at the St. Louis Fed, titled “The Impact of the Fed’s Response to COVID‑19 So Far,” explicitly notes the Fed’s absorption of longer‑term Treasury debt and implications for yields.

The “natural rate of interest” — known in the literature as r-star or r* — is the inflation-adjusted short-term rate that would prevail when the economy is at full strength and inflation is stable. It is unobservable and must be estimated. The most widely cited estimates come from the Holston-Laubach-Williams model maintained by the Federal Reserve Bank of New York, which put the US natural rate at roughly 0.5 percent through 2019 — far below estimates from preceding decades and consistent with the broader view that real returns to capital had structurally collapsed. Post-pandemic estimates have diverged substantially; the HLW model still suggests r-star is low, while survey-based measures suggest it has risen meaningfully.

Krugman has been a fixture of the New York Times opinion pages since 2000 and has used that platform to argue, repeatedly and with confidence, that inflation was not a serious risk in the post-GFC era.

In 2013 he argued that “servicing the debt in the sense of stabilizing the ratio of debt to GDP has no cost, in fact negative cost.” In a June 2021 Times column, he characterized the early inflation surge as "a blip" that would "soon be over." In a November 2021 column titled "I'm Still on Team Transitory," he argued that the inflation episode most closely resembled the 1946–48 postwar adjustment rather than the 1970s, and dismissed those drawing the 1970s parallel as "looking at the wrong history." Days later, on November 14, 2021, he admitted on Twitter: "I got inflation wrong; I didn't see the current surge coming."

His argument has continued to evolve in successively backfilled forms — including a 2023 reformulation that "the original Team Transitory proposition" had really been about whether unemployment would rise — but the core point stands: in 2021, with a generational fiscal-monetary experiment underway, one of the most prominent economists in the country was confidently telling Times readers not to worry.

His 2025 book Our Dollar, Your Problem is in part a sustained critique of the consensus’s complacency on debt and rates, and notes pointedly that at the American Economic Association’s 2024 annual meetings, “debt” and “deficits” did not appear in the top twenty-five words in paper or session titles.

The remark mattered immensely because even a noncommittal signal can affect the term structure: markets are forward-looking, and if markets believe the Fed might cap longer rates if it so chooses, long yields will fall in anticipation.

Perhaps unsurprisingly, he was marginalized by the Biden administration, which was hell bent on fiscal stimulus with “New Deal-era boldness.”

What's I've been on the edge of my seat about this week is Japan finally (finally! what all those people you mentioned were warning about) getting stuck between unaffordable government debt levels and currency devaluation. They should raise interest rates, but that would explode government payments on interest. Been following @Robin J Brooks who is doing a great job covering it.

You are conflating the operation of inflation targeting in unusual conditions with MMT. I'm not sure why, but probably because you (like the MMTers) are primarily concerned about government borrowing and so you're treating the Fed and the Treasury as if they were at least coordinating. But that's precisely the point of the way central banks have operated since Keynesianism was discredited - its better to set things up so the money supply is managed by an institution that's explicity disinterested in government spending and borrowing. This is what MMT aims to reverse, and so its only possible to describe recent monetary policy as MMT-like by pretending it is already reversed. But it isn't.

The last twenty years of Fed policy are simply a response to first a liquidity crisis, then an unprecedented real shock that was first deflationary and then inflationary that occurred when liquidity was still not at normal levels, within a regime of inflation targetting. You can argue for all three the extent to which the Fed might have caused the problem or initially made it worse, but the overall direction of policy was inevitable under and inflation targeting regime - they had to first find a way to expand the money supply faced with zero interest rates, and then they had to do it again, and then they had to rapidly reverse course. There wasn't really any other choice except to explicitly abandon their inflation target.

They did all of this in the face of a government that was borrowing more and more money, and so from an MMT point of view the giant black government box was "spending newly created money" but it wasn't doing that in anything like the way MMTers would advocate. The whole operation of QE is completely pointless from an MMT poiint of view. The MMT response to the financial crisis would have been something like a gigantic national jobs program, probably accompanied by direct real estate purchases, not the purchase of long term debt and mortgage securities.

MMT is dumb and dangerous. Its so dumb their explanations of their ideas are barely coherent which might have confused you, but what they're advocating for is really nothing like recent Fed policy. I spent a bunch of time researching this, basically because people being dumb on the internet annoys me, and the best model I could come up with is that MMTers think the IS curve is horizontal and so real growth is determined entirely by the money supply, or to put it another way the economy always behaves as if it is in a deep recession. Inevitably when monetary authorities response to an actual liquidity crisis they are doing to do things that are directionally similar to MMT proposals, but (thank god) they did not actually institutionalize any of MMTs policy recommendations.