Weekly Roundup #8

Housing | Construction, construction, construction (loans, costs, productivity)

EXECUTIVE SUMMARY

Welcome back to Boyd’s weekly roundup series. The past week was a busy one as we had three great Substack Live conversations — be on the lookout for several more over the course of next few weeks. Guests we currently have booked include Howard Husock of AEI (11/3), economist and notable housing realist Mike Fellman (11/4), and YIMBY Action Executive Director Laura Foote alongside Jeff Fong (11/7).

As for this week’s roundup, it’s almost entirely related to construction (loans, costs, productivity). This will increasingly be a hot topic for us.

Newsflow:

Fannie and Freddie to potentially expand into construction lending; FHFA seeking input

Apartment rent growth is waning; tenant incentives abound as landlords try to maintain occcupancy levels

Academic research:

How land use regulations have stifled construction productivity gains, and whether this is even true

How large cities are increasingly failing to accomodating growth, and the challenges confronting pro-affordability policies

Additional reading:

US construction labor productivity has meaningfully declined, even when using the most generous measures

Comparing California multifamily costs to peer states — namely Texas

NEWSFLOW

Politico: Homebuilders are using President Donald Trump’s growing calls for government-controlled Fannie Mae and Freddie Mac to get house construction “going” to push a controversial proposal: getting the mortgage giants to back construction loans. Proponents believe federal backing would make it easier for builders to secure large loans and give investors confidence, potentially increasing housing supply and lowering prices. Some policymakers — including prominent Senate Democrats — have expressed interest in expanding Fannie and Freddie’s authority but acknowledge the higher losses associated with construction lending. Bipartisan Senate efforts to address housing supply are underway, but there is concern about increasing federal involvement in private markets, especially as the administration considers privatizing Fannie and Freddie. The FHFA is currently seeking input on how Fannie and Freddie could play a greater role in boosting homebuilding.

WSJ: Apartment rents nationally are advancing at their slowest pace in years, thanks to the glut of new units that has taken longer than expected to absorb. More recently, job concerns among young people are posing a new threat to the rental market. “There was a saying: ‘Stay alive until 2025,’” said David Schwartz, chief executive of real-estate investment firm Waterton. “We’re in the camp, ‘We’ll be in heaven in 2027.’” Apartments are getting leased at record levels. But that is largely because of all the supply and because building owners are offering more tenant incentives. They agreed to concessions such as months of free rent on 37% of rentals in September — a record for that month — according to Zillow.

ACADEMIC RESEARCH

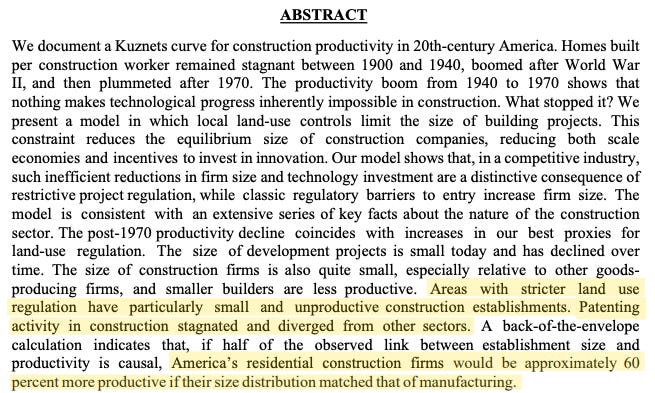

Why Has Construction Productivity Stagnated? The Role of Land-Use Regulation

D’Amico, Glaeser, Gyourko, Kerr, and Ponzetto (2024)

This study, which Jess Remington mentioned in our recent conversation, evaluates the hypothesis that land-use regulation reduces the average size of home builders, which limits their ability to reap returns from scale and their incentives to invest in technology. It found that:

Construction projects and firms are now much smaller, especially in regulated areas; small firms have much lower productivity — both revenues and units built per employee increase as firm size increases. Firms with 20 to 99 employees produce 45 percent more units per employee than the smallest firms. Firms with more than 500 employees produce more than four times as many units per employee.

Areas with more restrictive land-use regulation (measured by the Wharton Residential Land Use Regulation Index) have both smaller firms and lower construction sector productivity.

The decline in construction productivity has significant economic consequences, including reduced housing affordability and slower overall economic growth.

The policy implications of this suggest re-examining the local regulatory frameworks that fragment project scale and restrict firm growth, limiting sector productivity and innovation.

But there are objections to this research and by extension its policy prescriptions. Cameron Murray contends that construction measurement classification games hide productivity: when prefabrication improves, it’s reclassified as manufacturing rather than construction, making construction appear stagnant by accounting artifact. Mike Fellman noted that multifamily family units as a percentage of total units built are at a 40 year high, and that employees per unit is deeply flawed as a metric as homes are humongous compared to 1950. “What about square footage of housing per employee,” he asks.

Furthermore on a recent episode of the Odd Lots podcast, Brian Potter highlighted some real limiting factors:

Factory-built/modular housing is not the magic bullet: Despite attempts to standardize and prefabricate, modular construction faces unique challenges (shipping, assembly, custom site needs, liability, and unexpected costs) that limit efficiency gains.

Regulation and custom work: On-site homebuilding is still mostly manual and customized, with heavy administrative and regulatory burdens driving costs up.

Comparisons to other industries: Manufacturing industries achieve scale and efficiency differently than construction. Lessons from car or aircraft production are difficult to translate because buildings are larger, more varied, and site-specific.

Risk and incentives: The construction industry is risk-averse — failures in new technology or processes can lead to massive cost overruns, so there’s reluctance to experiment.

These are curious objections and constraints. It’s certainly a complex topic with lots of moving parts, but we plan on addressing the housing construction productivity issue in the coming weeks/months once we roll through our live conversations. For now, we’re still gathering facts and empirical evidence.

But given how fragmented the industry is, there must be some opportunity for achieving better economies of scale — whether via consolidation (structural), standardization (administrative), or technology/automation/AI (innovation). This is a core housing issue for Boyd, so stay tuned.

***

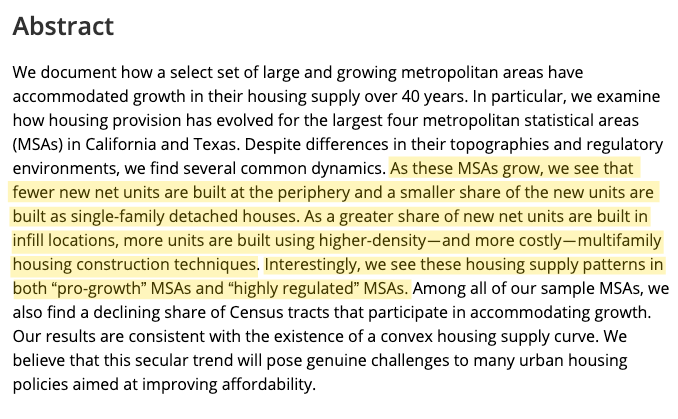

Houston, you have a problem: How large cities accommodate more housing

Orlando and Redfearn (2024)

***

Mike Fellman brought this study to our attention the other day. This idea of convexity in the housing supply curve — supply curves becoming steeper, or less elastic, with added demand — means that in practice, developers are less able to respond to price signals, especially in denser urban centers. In other words, according to this study’s findings, as cities reach limits of peripheral expansion, marginal cost of new units rises.

Moreover, even in less-regulated environments, large/denser cities naturally develop more rigid supply curves, posing long-term challenges for affordability: while regulatory reform and ADU policies in California and Minneapolis have added units, effects were smaller than forecasted, insufficient for major affordability improvements.

Theoretically, this is interesting because it implies that urban supply curves are not simply a function of regulatory regime or topography, but also city size and density as endogenous, dynamic constraints. That the Texas catch-up in housing development to California is not so much about institutions as it is about a particular city’s size and stage of urbanization challenges the standard view that Texas builds more because of relaxed land use regulations (Houston has notoriously low minimum lot sizes).

If this is all true — if, regardless of regulation, supply curves bend upward with increased density and demand, revealing greater long-run supply rigidity — it poses a fundamental challenge for housing policy.

ADDITIONAL READING

Five Decades of Decline: U.S. Construction Sector Productivity

Richmond Fed | Chen Yeh

During the 1950s and 1960s, construction productivity actually grew at rates that matched or exceeded the broader economy. However, around 1970, construction productivity began a sustained downward trajectory that has continued for five decades. While aggregate U.S. labor productivity tripled between 1950 and 2020, its measure for construction remained essentially the same. This divergence is especially notable when compared with manufacturing, which experienced a large increase in labor productivity over the same period despite dealing with similar physical assembly and configuration challenges.

[…]

Using three different analytical approaches — econometric techniques, detailed construction cost data and observable quality measures from property tax assessors and homeowner surveys — this paper finds evidence of upward bias in construction price deflators. However, the magnitude of this bias was not large enough to fundamentally alter existing conclusions about poor construction productivity performance. Its most generous estimates suggest that unobserved quality improvements may have biased construction sector productivity growth downward by at most 0.5 percentage points per year from quality-related factors, with additional small biases from other measurement issues.

[…]

Even accounting for these measurement problems, this paper concludes that “productivity growth may well have been quite low in construction, even if it has not been as low as implied by official statistics.” Construction productivity growth would still be essentially flat rather than negative, but it would remain far below other major industries: After adjusting for all potential measurement biases, construction productivity growth would still lag behind the next-lowest performing industries by about 1 percentage point annually and behind overall economic productivity growth by nearly 2 percentage points.

[…]

Additionally, the sector has shown deteriorating efficiency in converting materials into finished products, and there appears to be limited reallocation of resources from less productive to more productive areas, which is a mechanism that typically helps drive productivity growth in well-functioning markets.

[…]

The regulatory hypothesis offers a potentially actionable path forward, suggesting that reforms to land-use and building approval processes could help restore the technological dynamism that the sector demonstrated during its post-World War II boom. As policymakers grapple with housing shortages and infrastructure needs, understanding and addressing the root causes of construction’s productivity stagnation will be essential for promoting U.S. productivity growth.

***

The High Cost of Producing Multifamily Housing in California

RAND | Jason M. Ward, Luke Schlake

California is the most expensive state for multifamily housing production in every cost category we considered. Production costs per net rentable square foot for marketrate housing in California are 2.3 times the average cost in Texas. California’s publicly subsidized affordable housing costs are even higher, at 1.5 times the average cost of marketrate housing in California and more than four times the cost of market-rate housing in Texas.

[…]

Longer production timelines are strongly associated with higher costs. The time to bring a project to completion in California is more than 22 months longer than the average time required in Texas.

[…]

Key drivers of the remarkably high cost of publicly subsidized affordable housing production in California include requirements for affordable housing developers to pay substantially above-market wages and unusually large architectural and engineering fees (particularly in Los Angeles) likely related to highly prescriptive design requirements.

[…]

In California, production costs vary substantially across metropolitan regions. San Diego has the lowest average cost for privately financed apartments, at roughly twice the Texas average; costs in Los Angeles are 2.5 times the Texas average; and costs in the San Francisco Bay Area are three times the Texas average.