2% Inflation Targeting is Arbitrary and Accidental

But unfortunately, the US in no position to change it right now.

Almost nothing in modern macroeconomics is as universally accepted yet thinly justified as the two percent inflation target. Every major central bank holds it and every serious investor trades on the basis of it. Meanwhile almost no one can tell you where the number came from or why it is exactly two. The answer is that it is best understood as a convention — anchored in a few rough considerations but mostly improvised rather than derived from first principles.

The first inflation target in the world came out of New Zealand at the end of the 1980s. After the Reserve Bank of New Zealand Act took effect in 1990, New Zealand became the first country to write an explicit inflation target into law. The early agreements between the finance minister and the central bank governor set a band around 0-2 percent, later widened to 0-3 and eventually 1-3 with a 2 percent midpoint, meant to represent “true” price stability plus or minus about one percentage point to account for the fact that measured inflation runs a bit hot. Those ranges reflected a desire for low inflation and some allowance for index mismeasurement, but they were not the output of a carefully solved social‑welfare optimization problem, and subsequent changes were driven as much by politics as technocracy. That alone is reason enough to question the way the number has hardened into an object of faith.

And when you interrogate it honestly, the case against an evergreen two percent target turns out to be fairly strong. In fact, within the monetary policy literature the center of gravity has been drifting toward the view that there are much better ways to run policy than by fixing a single low number and treating it as sacred rule. The unfortunate reality, however, is that at the current juncture, the United States is ill-positioned to switch.

The origins of, objections to, and alternatives for, two percent inflation targeting

Canada, Britain, and Sweden followed New Zealand within a few years of its inflation target taking effect. The Federal Reserve was the great holdout: Alan Greenspan governed by instinct and constrained discretion, implicitly aiming at “low and stable inflation” but refusing to nail down a figure. It was only in 2012, under Ben Bernanke, that the Fed finally committed in writing to a two percent target “as measured by the annual change in the PCE price index,” making the anchor that disciplines the most important monetary authority on earth younger than the smartphone.1

To be sure, the reasons offered for two percent are real. A small inflationary cushion keeps interest rates far enough above zero that the central bank has room to cut in a downturn. Measured inflation runs a little hot because price indexes cannot fully capture how people substitute, trade up, and benefit from quality improvements, so true price stability sits slightly below the measured figure. And a bit of inflation greases the labor market because it lets real wages fall without anyone having to cut a nominal paycheck.

Each of these rationales is sound, but they are more so general reasons for a low positive number rather than for two in particular — as opposed to, say, one and a half or three. In reality, the number is a rudimentary convention (dressed as a calculation) that we’ve grown to accept. But because the world has genuinely shifted underneath it, the convention is aging poorly.

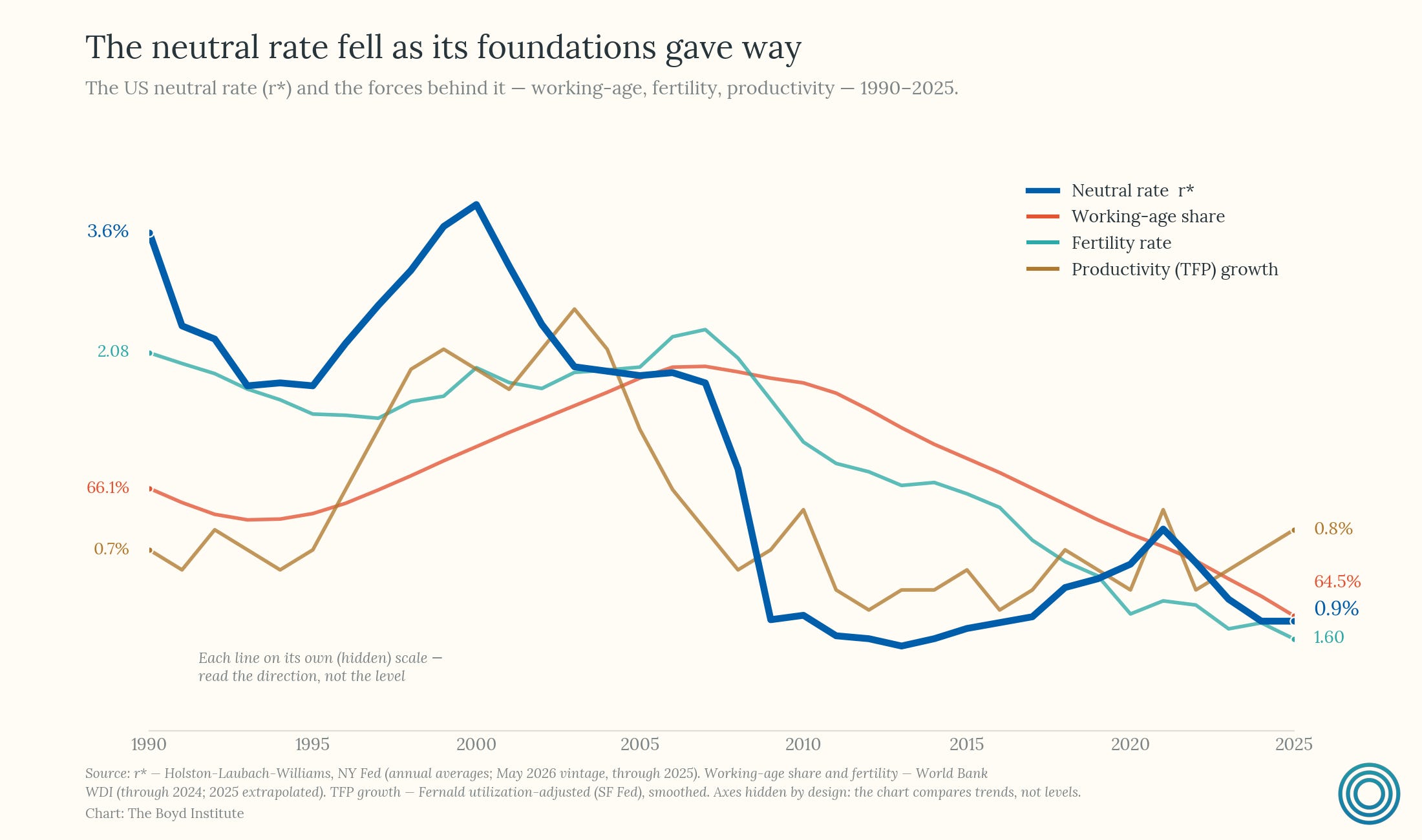

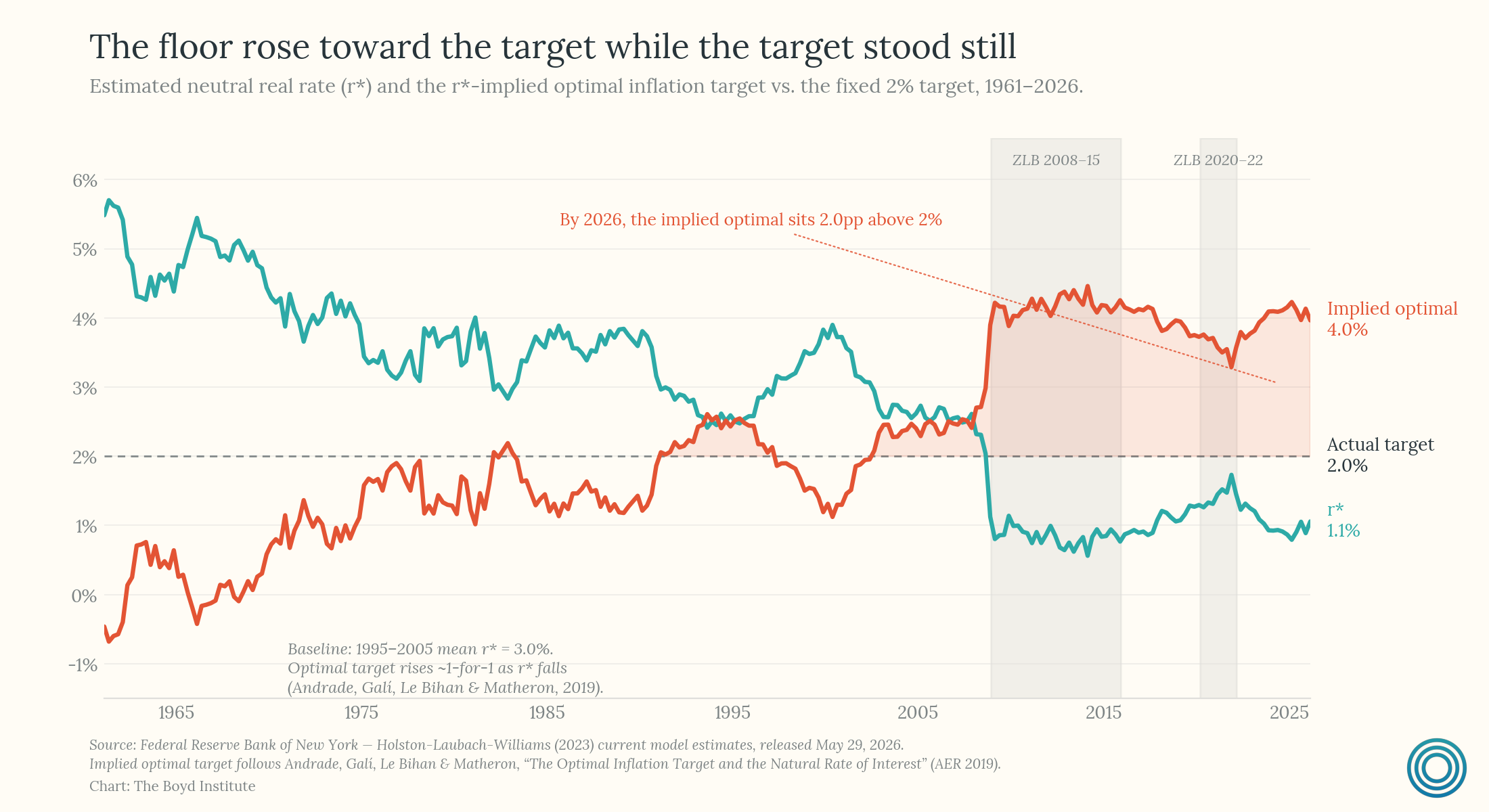

Here’s how. The neutral rate of interest (r*) — i.e., the rate at which monetary policy is neither contractionary nor expansionary, i.e., the short-term interest rate that would prevail when the economy is at full employment and stable inflation — has fallen for decades in advanced economies, dragged steadily down as the population has aged, fertility rates have plummeted, and productivity growth has stayed somewhat sluggish.

The problem is that a fixed two percent inflation target, which might have made sense when neutral rates were in the low‑to‑mid single digits, now guarantees more frequent collisions with the floor, meaning that the Fed starts every downturn closer to the zero lower bound (ZLB) and runs out of conventional policy-response room faster.2

It is on this basis that economists like Olivier Blanchard and Larry Summers have been arguing (for years now) that four percent is simply the better number. And more recent formal work has shown that in many mainstream models, as the neutral rate falls, the optimal inflation target tends to rise with it, recovering most of the decline, though not all of it. This is true because the cost of repeatedly hitting the ZLB rises while the marginal cost of somewhat higher steady‑state inflation remains comparatively small.3

There are also cleaner designs than an inflation target at all. The most elegant is to target the level of spending in the whole economy rather than the change in a price index — nominal GDP targeting, argued for years as a favorable option by Scott Sumner and the market monetarists, and developed in serious detail by economists at Mercatus.

NGDP-targeting fixes a single deep flaw in price targeting: an inflation-targeter reacts to prices without asking what is moving them. When prices move for reasons that have nothing to do with demand, it pushes policy the wrong way — and which wrong way depends on the shock. A productivity boom that drives prices down reads as below-target inflation, so the inflation-targeter eases, loosening into a bubble.4 A supply shock that drives prices up while output collapses reads as above-target inflation, so it tightens, deepening the slump. A spending-targeter is fooled by neither, because it tracks total spending rather than prices: it does nothing in the first case and holds steady in the second.

In short, the spending-targeter stops fighting the real economy and starts accommodating it — and on the merits alone, NGDP‑targeting is probably the better system.5

One could go further still and tie the goal to something structural like the growth of the working population or the growth of productivity so that the target being optimized for maps to the economy in its current state rather than the state it was in a generation ago. I have not seen anyone build a rule that writes those structural trends into the target itself, and it would be something new. In effect it would bake the determinants of the neutral rate directly into the policy rule instead of leaving them as background estimates. But the instinct behind it seems sound (to me at least).

At any rate, on the technical merits, the critics of two percent inflation targeting are right: a static number governing a moving economy is a strange and suboptimal way to run the most important price in the world. It is largely arbitrary within a narrow band of “low positive numbers,” too low for a world of chronically depressed neutral rates, and too rigid to adapt to persistent changes in demographics and productivity.

So if this were only a question of monetary engineering, it is rather apparent that the answer would be to retire the existing target and build something smarter — be it higher long‑run inflation targets or some alternative convention.

But is it simply a question of monetary engineering?

No… at least not entirely.

There is also a serious opposing camp, including former Fed chairs Bernanke and Yellen, the economist Frederic Mishkin, and others, who worry that higher inflation targets can pull expectations loose from their mooring. Central banks have spent decades teaching the public that “two percent” essentially just means price stability; move the goalposts and you risk losing the price anchor itself.

The more basic worry is that inflation is not just a statistical outcome but a behavioral one. So long as expectations stay anchored — so long as the public believes next year’s prices will behave roughly like this year’s — a central bank can carry a little inflation without it compounding. But expectations are fragile. Let them come un‑anchored and a modest, well‑meant adjustment to the target gets read as permission for something larger: if households expect prices to be higher tomorrow, they spend sooner today, and at the macro level, the price-expectation loop begins to feed on itself. In other words, the hazard of moving the goalposts is that the act of moving them signals to everyone that the number can move.

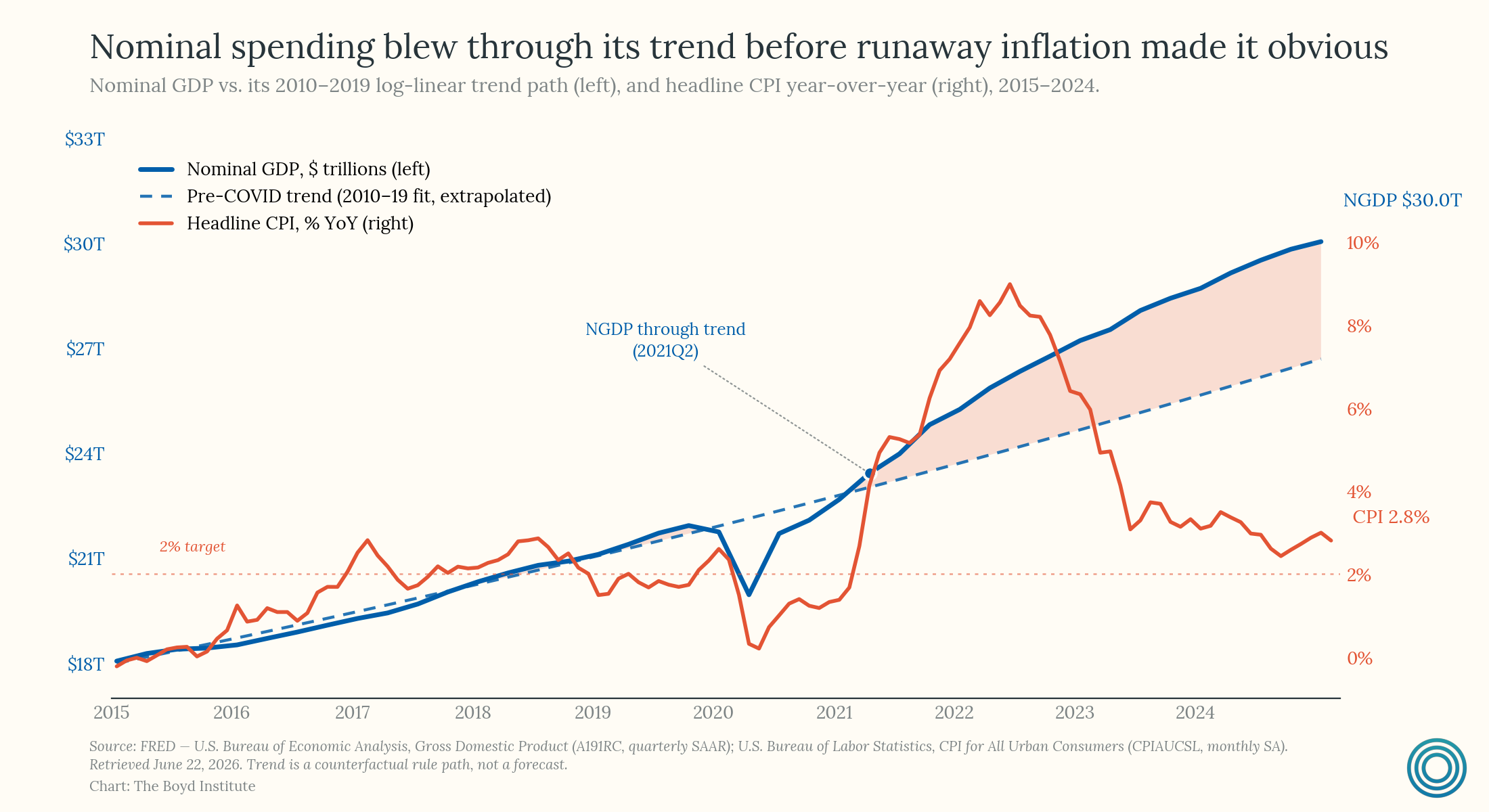

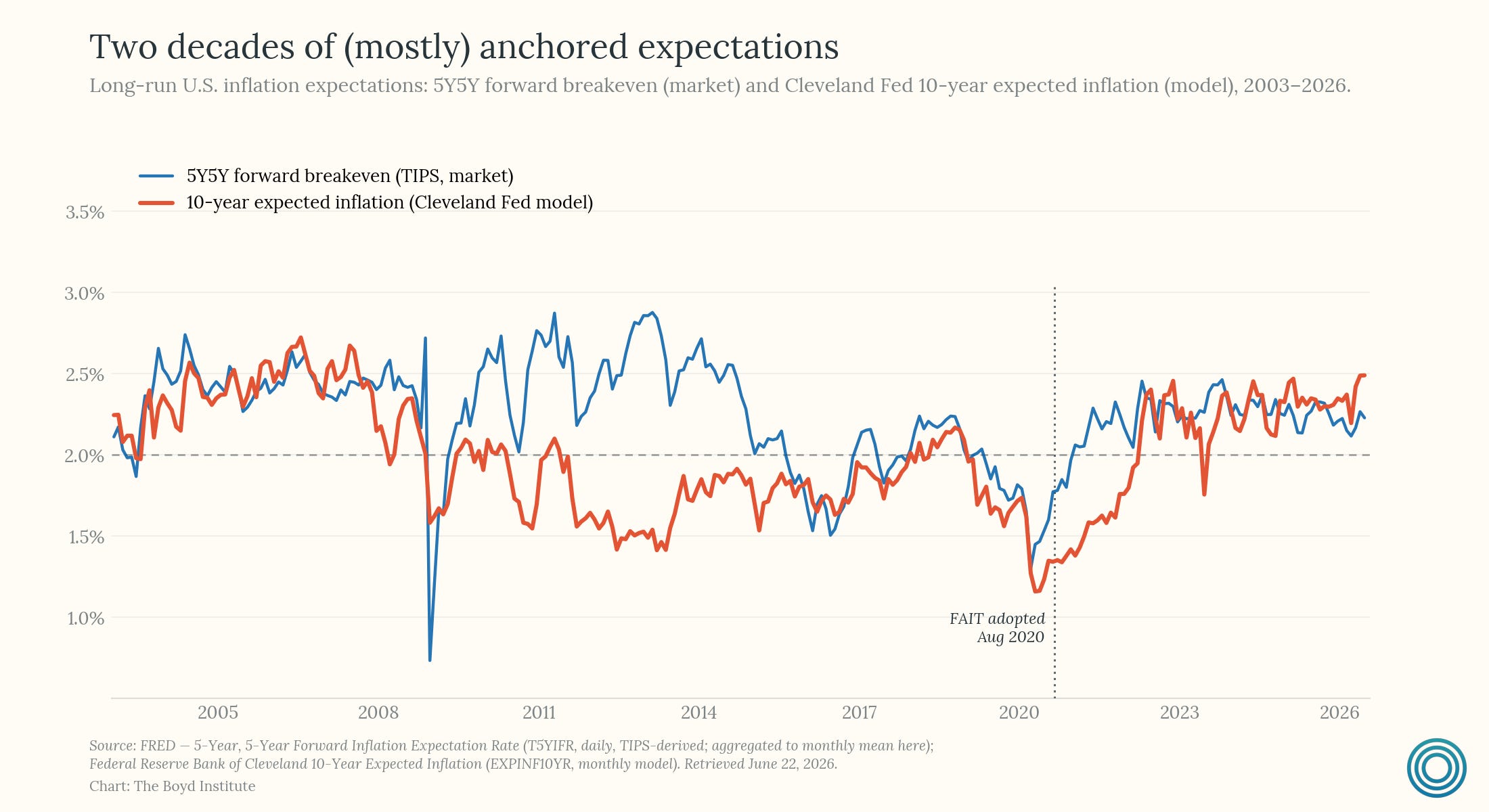

That is why the Fed’s pandemic-era framework change was so risky even though it was modest on paper. In August 2020 it rewrote its own framework and promised to let inflation run above two percent for a while to make up for the years it had run below. This came to be known as flexible average inflation targeting, or FAIT. The idea was defensible on paper: after a decade of undershooting and a sunken neutral rate, a planned overshoot of two percent to achieve a longer-run average made sense empirically. But within a year inflation had surged well beyond what the new framework had contemplated, driven by a combination of supply shocks, fiscal stimulus, and accommodative monetary policy all at once. The promise to tolerate overshoot then became a serious credibility problem for the Fed (and frankly an embarrassment it spent years living down).

Formally, the language of FAIT survived into the mid‑2020s. But in practice, by the time inflation had been wrestled back down, the Fed returned back to something closer to plain-vanilla inflation targeting and symmetric concern for too much or too little. Overall there was at least one lesson from this episode that is pretty straightforward: even if the old framework was not perfect, a new rule is easy to announce but very hard to keep control of once shocks arrive and expectations start to move. And the part that should worry us is that FAIT was a modest reform attempted in a storm that turned out to be passing. The next reform attempt, if tried now, would be amidst a storm that is not so — dare we say — “transient.”

Political incentives make changing the Fed’s targeting framework right now risky

Consider the structural and rapidly-worsening situation the US finds itself in now. The country is not in a war, not in a deep recession, and unemployment remains low. Yet it is running a deficit of roughly six percent of national income, debt held by the public is closing in on the record it set at the end of WWII as a share of GDP on current projections, and net interest is approaching the trillion‑dollar mark — already larger than defense and Medicare — leaving only Social Security above it in the budget. This is an almost unprecedented combination.

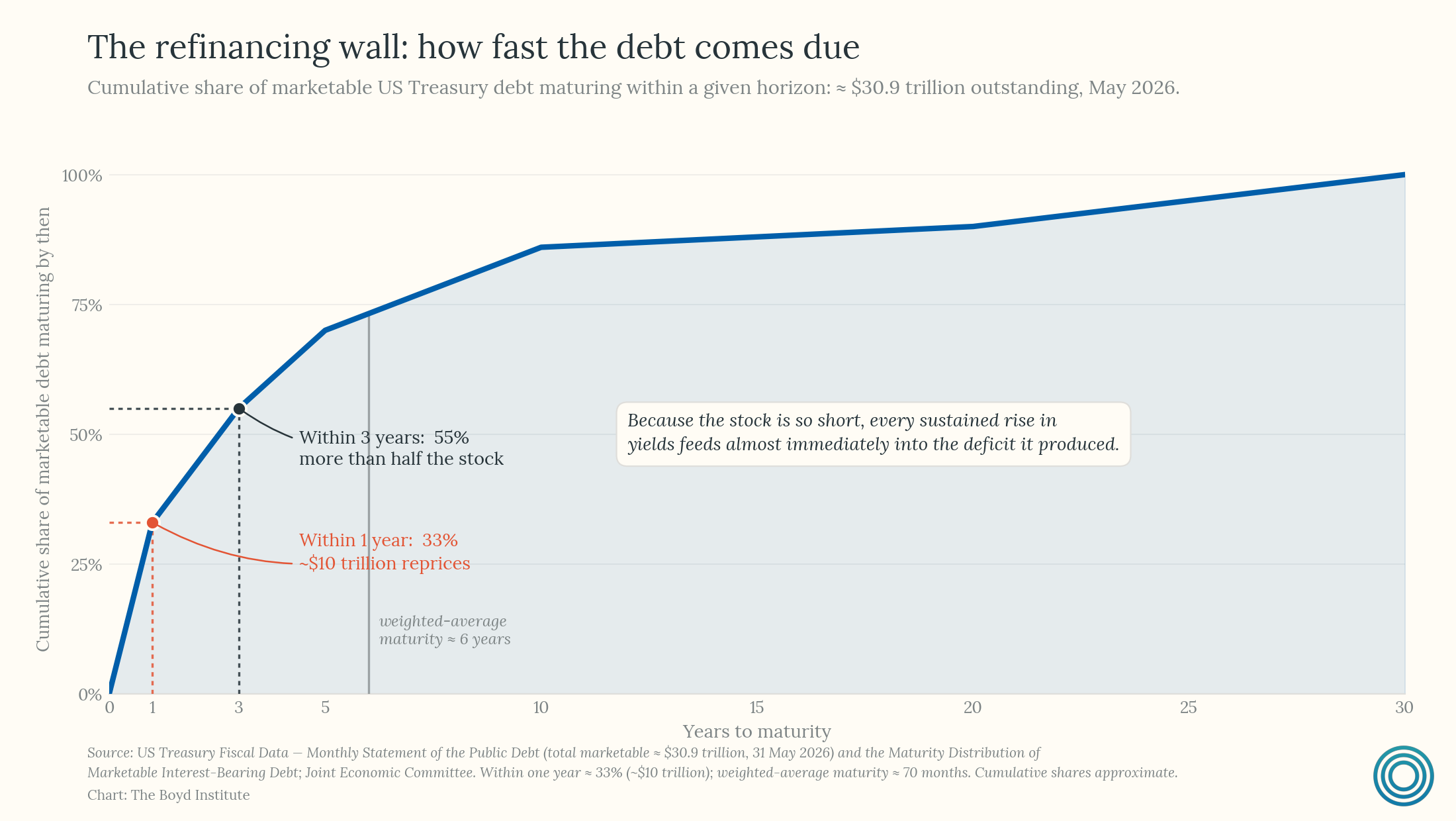

Furthermore Treasury data show that on the order of one‑third of marketable debt is due to mature within a single year and well over half within three, meaning that every sustained climb in yields feeds straight back into the deficit that produced it.

Why the looming debt‑and‑deficits storm reshapes the inflation‑targeting reform calculus comes down to political forces. A government borrowing — more specifically, borrowing to refinance — at this scale has an unspoken but powerful interest in cheaper money: a few years of rates held lower than they should be, and thus a little more inflation, means that the real weight of the debt eases on its own.

To capture this opportunity would mean the inflation target stops being a technical dial the Fed turns at will and instead becomes something the Treasury has a stake in. That is the edge of fiscal dominance: a regime in which the fiscal authority, not the central bank, sets the path of inflation — a regime where “monetary policy serves fiscal ends.” So the risk to reopening the framework right now would be handing a fiscally cornered government say over the one number it most wants to move, and for reasons that have nothing to do with sound monetary policy. The unsettling question is whether we are already drifting toward it.

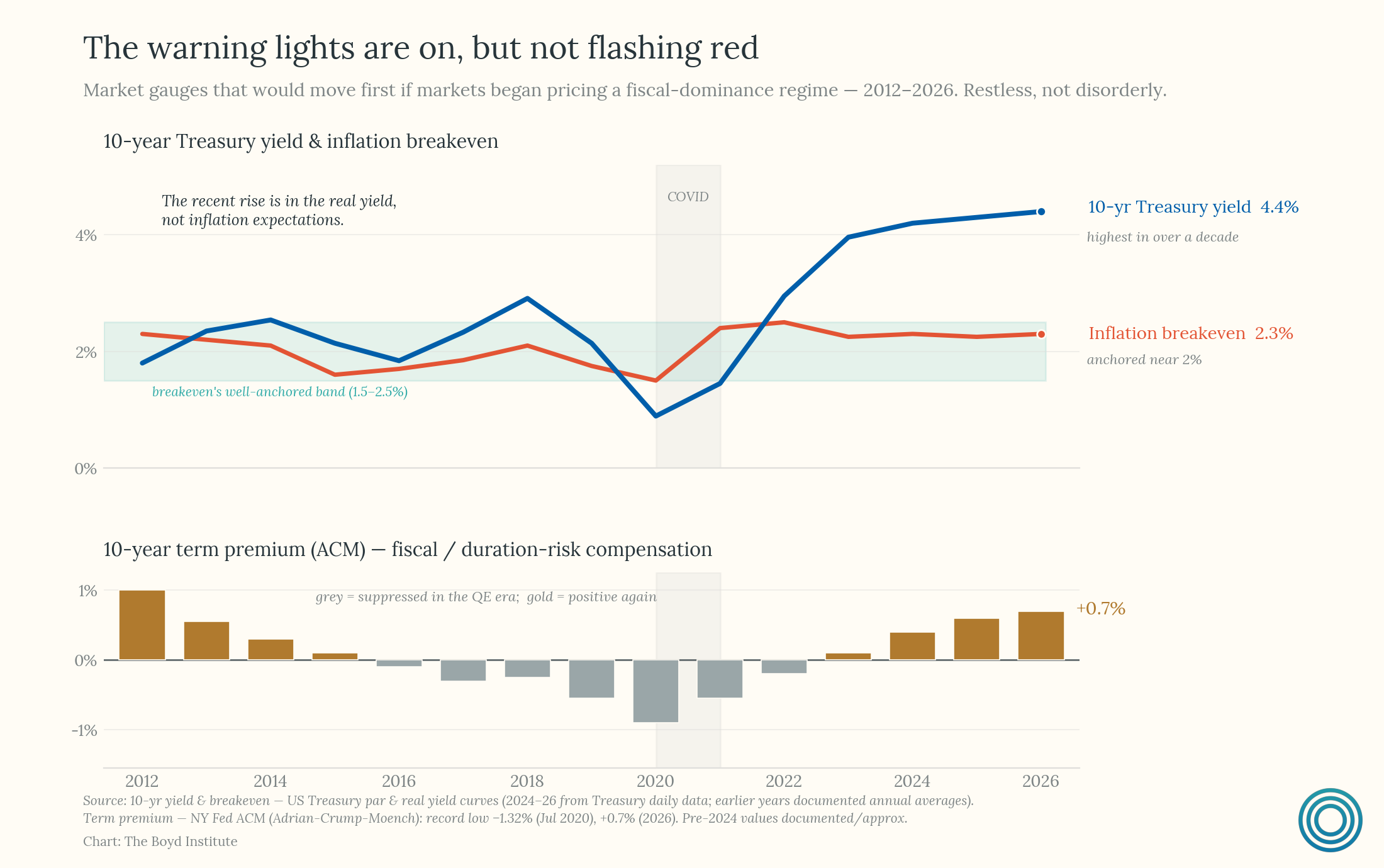

Despite abounding incentives, the answer is that we are not there yet, at least according to the market’s reading. Treasury yields, term premia, and inflation breakevens may be showing slight signs of distress over the past few years, but they are still consistent with a world in which the central bank retains the upper hand — and where inflation expectaions remain relatively anchored.

The Fed still sets policy to hit its target and the bond market has not begun to price anything like a fiscal-dominance regime. If Fed independence were genuinely broken, the signals would likely show up in a much sharper backup in bond yields, an unusually high term premium, and a generally far more disorderly Treasury market than anything we have seen recently.

None of this means the country is out of the woods regarding fiscal capture of monetary policy. According to the logic Sargent and Wallace set out in 1981, fiscal dominance happens less through a watershed moment than through a gradual regime shift a nation drifts into. When deficits run large enough for long enough, natural forces nudge the central bank toward no longer acting as if the budget belongs to the fiscal authority. And the clearer warning is not the headline debt ratio but the share of the budget swallowed by interest. As that share climbs, so too does the risk of higher rates doing damage and thus the political payoff of paring Fed independence — potentially setting off a harmful, self-reinforcing cycle. These leanings, it should be said, may already be underway.

The president has demanded deep rate cuts and has been aggressive in trying to impose costs for Fed noncompliance. In August 2025 the administration moved to remove a sitting Fed governor, Lisa Cook, over allegations about mortgage paperwork from before she joined the Board — conduct with no bearing on her FOMC vote, and for which she has not been charged. The Supreme Court heard the case in January 2026 and signaled it was unlikely to let the removal stand. Trump’s Justice Department also went as far as opening a criminal investigation into former Fed chair Powell himself in early 2026 (over his congressional testimony about the Fed’s headquarters renovation) before dropping it months later without bringing any charges. While these are not the symptoms of a regime that has already flipped, they are the political pressures that, if maintained over time, do flip it.

It is also worth being precise about this channel, because explicit adjustments to the targeting framework are not the only door in. Political capture of monetary policy does not require reopening the target at all. Along these lines — “personnel is policy” — adjustments to the Fed’s policy frameworks can run straight through appointments and pressure, which is what the Cook and Powell fights were really about.6

And there is another door, still blunter than either of the above. Congress could simply rewrite the Fed’s mandate. It is reaching for that lever already through the Price Stability Act of 2025 (H.R. 5396), which is now moving through the House and would strip the Fed’s employment goal outright, making its inflation target even more central to monetary policy. Granted, under current conditions, this particular bill points the hawkish way. But the same power that can narrow the mandate can loosen it, and a Congress cornered by its own financing needs is the most direct fiscal-dominance vector of all — one that routes around the Fed completely.

Underneath it all ultimately sits the age-old temptation a government deep in debt faces. Nixon succumbed to it, or at least tried to. In lieu of defaulting, cutting spending, or tax hikes, a government, once fiscally-dominated, can simply let inflation run a little hot, hold rates a little low, and watch the real value of the debt effectively melt away. Economists including Hanno Lustig call this financial repression:

“[A] catch-all term for all of the things governments, central banks, and financial regulators can do to lower the government’s cost of funding below the market rate. You can think of it as an informal tax on bond holders and savers. Over the past few decades, we’ve seen governments in advanced economies reach aggressively for financial repression tools in the face of increasing fiscal pressures as a result of demographic changes.”

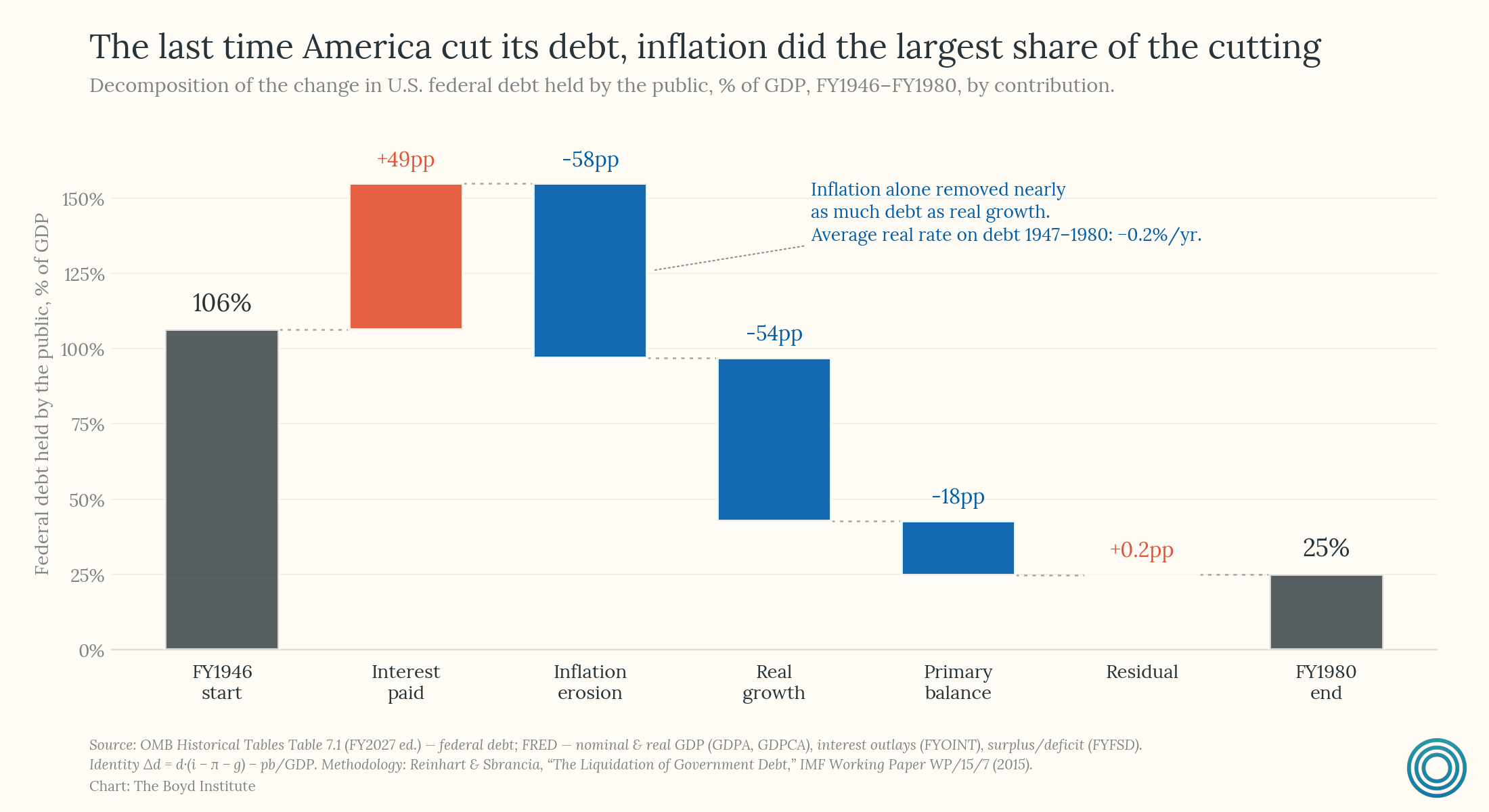

Japan is the most prominent recent example, but it is also basically how the US took its debt down from over 100% of GDP after the war to under a quarter of it by the end of the 1970s (repression coming via surprise inflation plus pegged and regulated rates).7

But that escape required a captive bond market: capital controls, long-dated debt, and savers with nowhere else to put their money. None of those requisites hold today. Roughly a third of the debt is held by foreigners who cannot be repressed, about seven percent is indexed to inflation outright through TIPS, and the average bond now matures in about six years — which means the debt reprices almost as fast as it could be inflated away. To move the debt now, inflation would need to be high enough and sustained enough to outrun a market that virtually reprices in real time.8

So the reality is that the great liquidation of the postwar decades is no longer on the menu, even if the temptation to follow that playbook remains. Furthermore none of this is to mention that, given the hyper-salience of “inflation” and “affordability” as public issues in the current climate, it is just not a very politically rational way out.

Conclusion: the right reform, the wrong moment

The question of whether a better target than two percent inflation exists is fairly settled (it does). The unsettled question is whether the US has earned the right, and whether it is fiscally positioned, to reach for it now.

The “Volcker Shock” of the early 80s — when then-chairman Paul Volcker changed the Fed’s policy stance in the middle of a double-digit inflation crisis — offers a clean test. It worked because instead of reformulating the Fed’s mandate, he adjusted its policy regime to deliver the prevailing mandate even harder. He was willing to go as far as tipping the economy into recession by driving interest rates toward twenty percent, all to prove the anchor would hold, bucking what was politically expedient in service of reasserting institutional credibility.

So it is not simply that reform from weakness is impossible. Another example is Brazil, which adopted inflation targeting in 1999 in the teeth of a currency crisis and made it hold, pairing it with a hard fiscal-responsibility law the next year. But Brazil reformed because catastrophe left it no choice and forced discipline alongside the new rule. Today the US has the opposite problem: Fed credibility is often nowadays taken as a given, the dollar’s reserve currency status buys the government enough rope to reform badly, and no external creditor is forcing it to pair a new target with restraint.

Every framework change that strengthened the anchor was, at bottom, a move toward discipline. The world adopted inflation targets in the calm of the 1990s for this very underlying reason: to lock credibility in. What is being entertained now — loosening the anchor to relieve a financing problem — is the mirror image. Rewriting the rule to make a promise harder to break is fine and warranted; rewriting it to make the debt easier to carry would come with harsh second-order effects. And a reform undertaken in this fiscal weather would be the second kind, no matter how carefully it was dressed up as the first.

There is, to be fair, a real truth the reformers are reaching for, and it deserves to be granted. The inflation an economy can comfortably bear really does depend on how fast it grows, so the instinct to tie the rule to nominal output or something macroeconomically similar is not foolish. But you do not get the inflation a fast economy can carry by editing the target. You get it by… growing fast. Thus productivity is the one thing that actually changes what is sustainable, and no act of the central bank can conjure that into being.

None of this is to pretend that waiting is free. Leaving the target where it is for longer carries a real cost, and it is precisely the cost the first half of this essay laid out: a two percent anchor in a low‑r* world means more frequent collisions with the zero lower bound, weaker recoveries, and a central bank too often out of room — a failure of the employment half of its mandate as much as the inflation half (the Japan case is instructive here). To wait is to keep paying that price. And however nontrivial that price is, the alternative price — handing a cornered Treasury a credible-sounding reason to inflate — is larger, and far harder to reverse. A lost recovery may eventually be regained while a debased anchor may not.

So the honest conclusion is the uncomfortable one. Two percent is arbitrary, a better system exists, we know its name, and yet we should still leave it alone. A country in command of its budget could rewrite the rule and be the better for it. But the US — a country running massive deficits at full employment and above-target inflation — has lost the standing to act on it.

Upending monetary policy frameworks now would be like choosing a new referee in the middle of the game we are losing: in all likelihood, it would turn a bad situation worse. This is not an argument for never, but it is an argument for sequence. The moment to reach for a better target is when the conditions that make reaching for it dangerous have eased — e.g., when the deficits have normalized, when debt has stopped climbing as a share of the economy, when the interest bill no longer crowds out everything around it. Inflation-targeting reform belongs to that moment, not to this one.

And note how little of the target is actually fixed. Congress never legislated two percent. The Federal Reserve Act commands only “maximum employment, stable prices, and moderate long-term interest rates” — three goals, no numbers. Two percent is the Fed’s own gloss on “stable prices,” not set by statute.

The zero lower bound is the floor beneath which a central bank (Japan’s being a modern exception) cannot easily push its policy rate. Because people can always hold cash, which yields zero, rates cannot fall far below it. Once a bank has cut to that floor it is largely out of conventional ammunition and must reach for blunter tools — quantitative easing, forward guidance, reverse repo facilities, etc. The lower the neutral rate, the sooner an ordinary downturn drives policy back into that unconventional corner.

Simulations for Japan’s “Lost Decade” suggest that a 4 percent target paired with a stronger output‑stabilization mandate could have cut output losses dramatically by avoiding long stretches at the lower bound.

It is the older insight behind George Selgin’s productivity norm: in a growing economy, the price level should be allowed to drift down as productivity rises rather than be propped up to a fixed target. A mild, productivity-driven deflation is benign — firms passing lower costs along — and a central bank that fights it with loose policy is how you end up inflating a bubble.

These alternatives of course face practical objections. NGDP is observed only quarterly and subject to revision, structural rules would rely on noisy data, and any spending target trades off more short‑run inflation volatility for better output stabilization. But those are engineering and communication problems, not fundamental flaws in the logic.

That is exactly why the target is worth guarding rather than reopening. It is the one lever the Fed still controls itself — the mandate above it belongs to Congress — and the one place the Fed can decline to hand the fiscal authority a respectable excuse. Leaving two percent alone will not, on its own, keep the Fed independent. But reopening it now would volunteer a weapon the central bank does not have to give up.

Carmen Reinhart and Belen Sbrancia, “The Liquidation of Government Debt.” For the United States and the United Kingdom, they estimate that negative real interest rates liquidated government debt at an average of three to four percent of GDP per year between 1945 and 1980 — a tax almost no one felt in the moment, yet one that cumulatively did most of the work.

In high‑debt situations, fiscal dominance and financial repression often co‑move. Recent work explicitly notes that when fiscal dominance pressures rise, policymakers may respond with more financial repression as one mechanism for funding the state and easing the tension between fiscal and monetary policy. Financial repression shows up in their models as one manifestation of fiscal dominance — alongside explicit pressure on policy rates, “fear of floating,” and so on.

And the bill would not stay isolated. The dollar earns this country a discount — an “exorbitant privilege” — no other borrower gets: the world holds Treasuries and asks less in return because it trusts that the dollar in five years will still buy roughly what it buys today. That trust is sticky — there is no rival safe asset deep enough to flee to, and even freezing a hostile central bank’s reserves in 2022 did not break the habit. But sticky is not the same as permanent. The dollar’s share of global reserves has drifted down for two decades, and the premium investors demand to hold long-dated debt is near its highest since 2011. A privilege this large and this gradual is easy to treat as free, precisely because no single abuse seems to cost very much. But that is the trap.

I agree with you that moving to a higher inflation target would be a bad market signal right now, but NGDP targeting isn't necessarily inflationary. It would have been relatively inflationary in 2006 when Scott and others bough the idea to public awareness, but it would have been deflationary during the post-COVID inflation relative to the 2% norm. The other possibility - more superficially hawkish but still a level target - is George Selgin's productivity norm, in which the monetary authority would aim to have prices fall in line with productivity. Much more logistically difficult to pull off, but its the only deflationary proposal I've ever come across that can be defended against the accusation that it will just be a return to regular banking crises.

Admirable post, although I don't come down in the same place on the takeaways.

For one thing, you assume that the neutral interest rate has been coming down and will keep doing so. I agree that it was low or negative in the 2010s, because of demographics and productivity slowdown, and that created a sluggish ZLB economy for years.

But interest rates are higher now, and I don't think it's transient. It's fundamental. AI is changing the productivity trend and putting it on a higher path.

A 4% inflation Target would have been useful 10 years ago. I don't think we particularly need it anymore.