Japan Is Not The Counterexample

For decades, Japan has been trotted around as proof that high debt and wide deficits are costless. Now that's reversing, and treating it as a model for America gets both countries wrong.

Seemingly every argument that America’s debt concerns are overblown arrives on Tokyo as Exhibit A. Stephanie Kelton called Japan a country that “has been conducting MMT for some time.” Warren Mosler, the theory’s originator, has held that high JGB yields are “a distributional issue at most, not a funding problem.”

The evidence, in fairness, has looked pretty compelling. A sovereign that borrows in a currency it prints took gross debt past 240% of GDP and held it there while suffering functionally none of the predicted consequences. There was no funding crisis, no default, no inflation spiral, and ten-year yields on government bonds floated persistently near zero. Blind faith in monetary orthodoxy led many traders to short JGBs in what became known as the “widowmaker” trade. Politically, Japan’s record has made debt hawks in Washington’s hand-wringing over a debt ratio half Japan’s size look like pure theater.

We have also been critical of MMT, even if it’s impossible not to concede much of the theory’s core premises. The central descriptive claim — that a monetary sovereign does not face the hard external-funding ceiling that constrains a household, a firm, or even a euro-zone member — is not wrong. Unlike the Soviet Union or the graveyard of other sovereigns whose fiscal crises precipitated their nations’ undoing, Japan’s debt is almost entirely held by its own citizens and domestic institutions. This means that the risk of a classic sovereign default, where a country runs out of foreign currency to pay its foreign creditors, is effectively nil.

But sovereign default is not the only risk vector and Japan’s record was never evidence of deficits being costless. In this piece, we argue instead that it was evidence of a specific machine running under specific conditions, that these rather goldilocks-esque conditions have meaningfully shifted, and that Japan isn’t as much the counterexample to fiscal anxiety as it is a fairly strong case for it.

The Machine

The conventional fiscal-anxiety framework begins with Sargent and Wallace's 1981 “Some Unpleasant Monetarist Arithmetic,” which showed that monetary financing eventually becomes a tax on bondholders via inflation. Japan long looked like the exception. Headline and core inflation ran near zero or below 2% for most of the period after the 1990s asset bust, and even after the BoJ formally adopted a 2% CPI target in 2013 it repeatedly undershot that goal — the expected tax never showed up. Yet former IIF chief economist Robin J Brooks has characterized Japan as “where MMT goes to die.” Exactly how it is dying is an instructive case for the developed world's fiscal hawks.

Let's start with the underlying "machine," which involved three moving parts:

A central bank with an inflation target it couldn’t hit;

A fiscal authority that took advantage of the resulting low‑rate environment to borrow heavily at near‑zero nominal yields; and

A captive, predominantly domestic, investor base — banks, insurers, pension funds, and eventually the BoJ itself — that absorbed most of the issuance.

An aging population and chronically weak demand kept underlying inflation pressures subdued, giving the BoJ room to expand its balance sheet aggressively. Rather than demonstrating that debt and deficits are irrelevant, under the cover of chronic deflation, Japan’s experiment amounted to a prolonged attempt by the BoJ to lift inflation to target via large‑scale asset purchases (QQE and yield‑curve control) that made its balance sheet, as a share of GDP, far larger than the Fed’s at its QE peak.

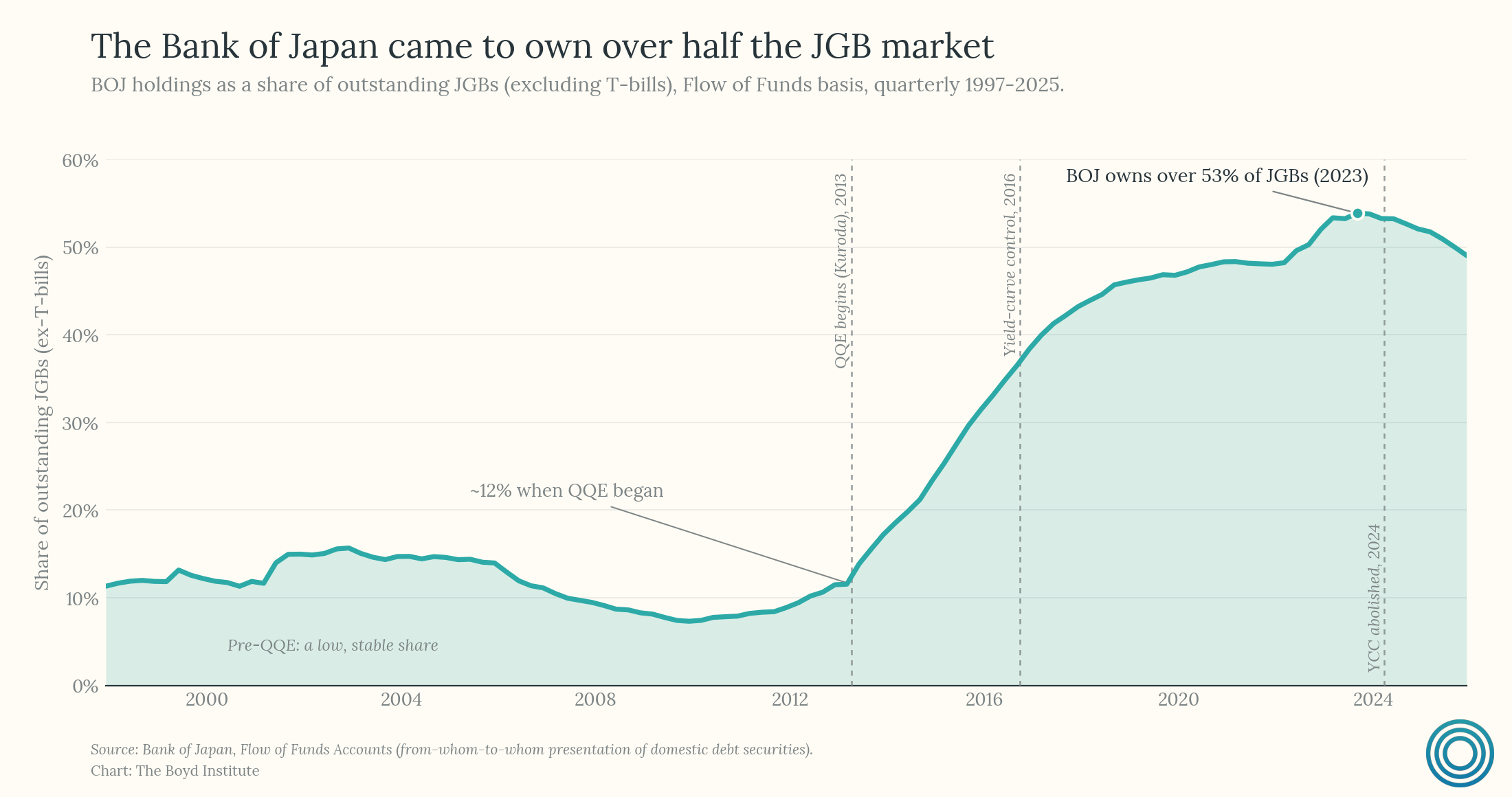

This was highly convenient for the fiscal side. As long as inflation stayed below target and long‑term yields remained compressed, the government could roll over and expand its debt stock at minimal interest cost, while the central bank absorbed a growing share of outstanding JGBs through secondary‑market purchases. Put simply, the government issued while simultaneously the central bank absorbed.

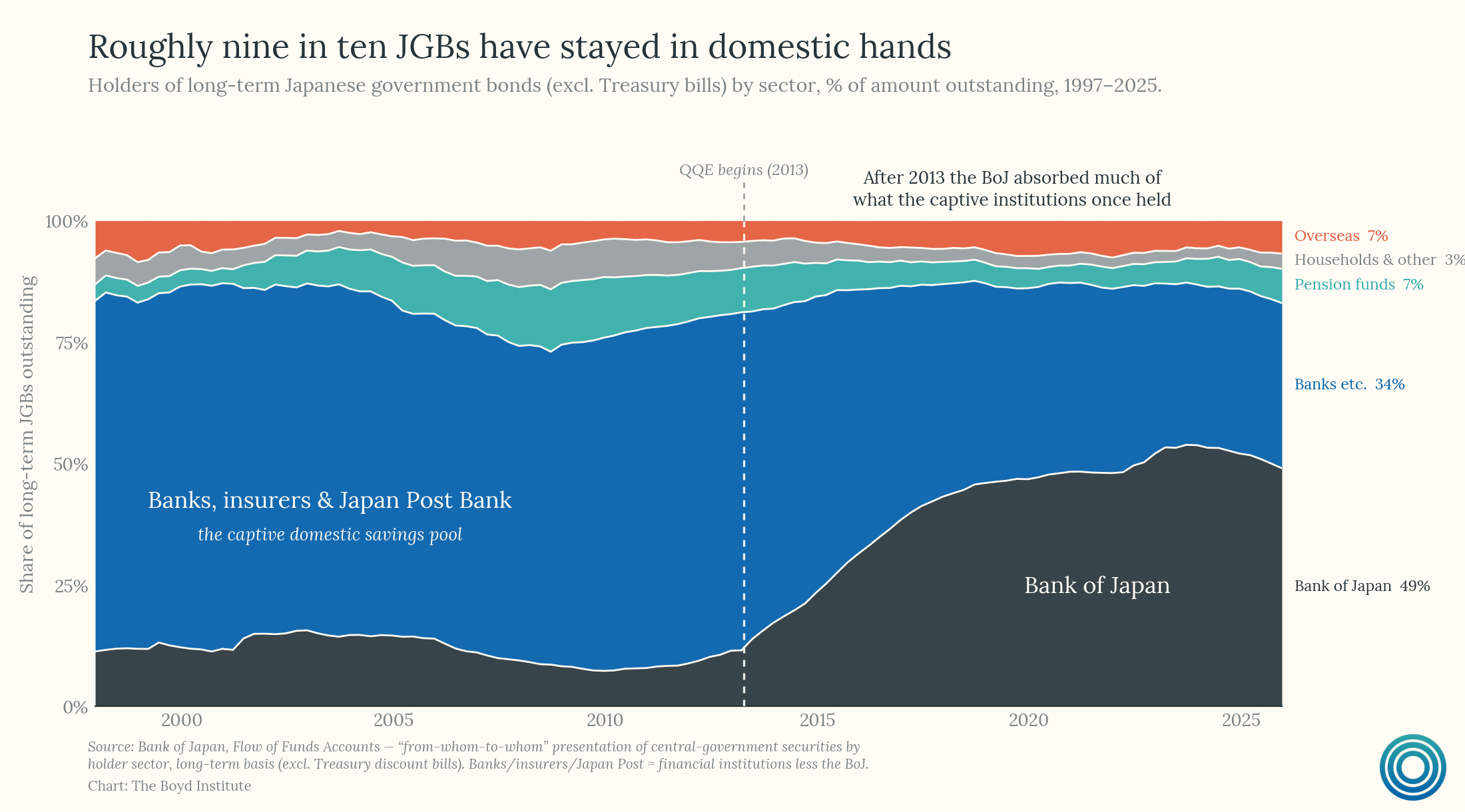

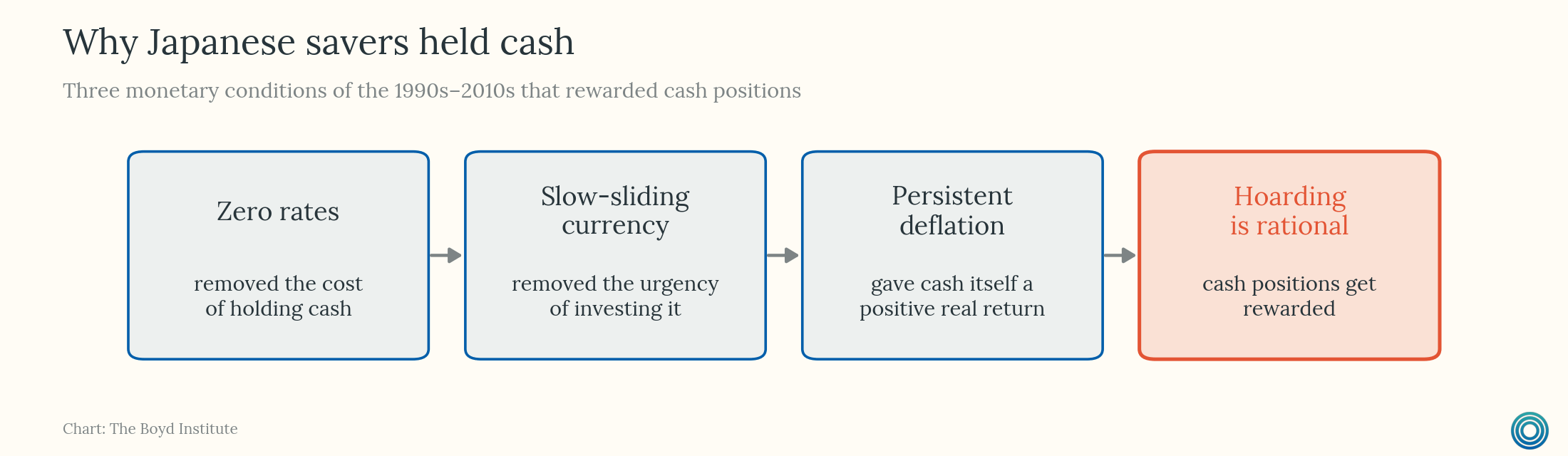

What the BoJ didn't absorb directly, the captive domestic savings pool did. Regulations had channeled household deposits into low-yield accounts and the postal system: upwards of 90% of JGBs have been held by domestic institutions and households for most of the past two decades.1

Scott Sumner makes the sharpest version of the reading. In the market-monetarist frame, the stance of monetary policy is defined by outcomes-versus-target, not by instrument settings themselves. Perhaps counterintuitively, low rates and a massive balance sheet are actually consistent with a tight monetary stance in a situation where the central bank keeps missing its inflation target to the downside.2

By that measure, the BoJ ran a relatively hawkish policy regime for three decades — whatever the face value of its instruments might have indicated, and however stable markets remained.

No Crisis Is Not The Same As No Cost

What the dovish reading misses, even on its own evidence, is what the dormancy actually cost. Japan didn’t disprove the inflation constraint so much as find the one macroeconomic environment in which it lies dormant — chronic, structural deflation — and live there for thirty years. The cost of doing so was real, even if it wasn’t paid in the way the dovish framework would predict.

The fiscal expansion that ran alongside the monetary one — in Sumner’s own words, “one of the most reckless in human history” — was reckless precisely because it failed to stoke aggregate demand. Monetary offset kept demand neutralized in real time, so the deficits bought very little in macro terms, not even inflation.3 For an MMT framework that locates demand in fiscal policy, this must constitute the model failing on its own metric. Indeed, the one period of decent NGDP growth — Abenomics — came when Japan combined aggressive monetary easing with a shift back toward consolidation, including consumption-tax hikes in 2014 and 2019, rather than the ever‑looser fiscal stance MMT advocates.

What the deficits bought instead was time. Japan paid continuously in foregone growth: for much of the period since the mid‑1990s, its nominal GDP has been essentially stagnant, with the level in the early 2000s about the same as in 1995 and even in 2025 still below its mid‑1990s peak in dollar terms.

So the honest framing here is that the debt ratio climbed less because the numerator exploded than because the denominator refused to grow. Three decades of calm bond markets were three decades of monetary policy successfully suppressing what fiscal policy was trying to do — while the debt stack piled up. As Sumner has put it:

“I was told ‘deficits don’t matter’ because interest rates were low. I pointed out that rates might not stay low forever, and that these debts would still be on the books when interest rates started rising.”

The familiar “Lost Decade” story does a good job of naming the symptoms, but the underlying dynamic gets much less attention.

Such an environment produced an economy where capital found no productive call worth answering, and what got starved was the productive base. Real wages went sideways for decades; corporate Japan, sitting on the deepest cash piles in the developed world, rationally declined to deploy them. Unsurprisingly, the Nikkei spent thirty-four years climbing back to its 1989 peak, creating a generation of equity investors who got less than nothing in real terms. Meanwhile balance sheets stayed pristine and markets non-volatile, while the central bank was left without the capacity to answer shocks and household purchasing power eroded under a currency the authorities had limited room to defend and ultimately allowed to slide.4

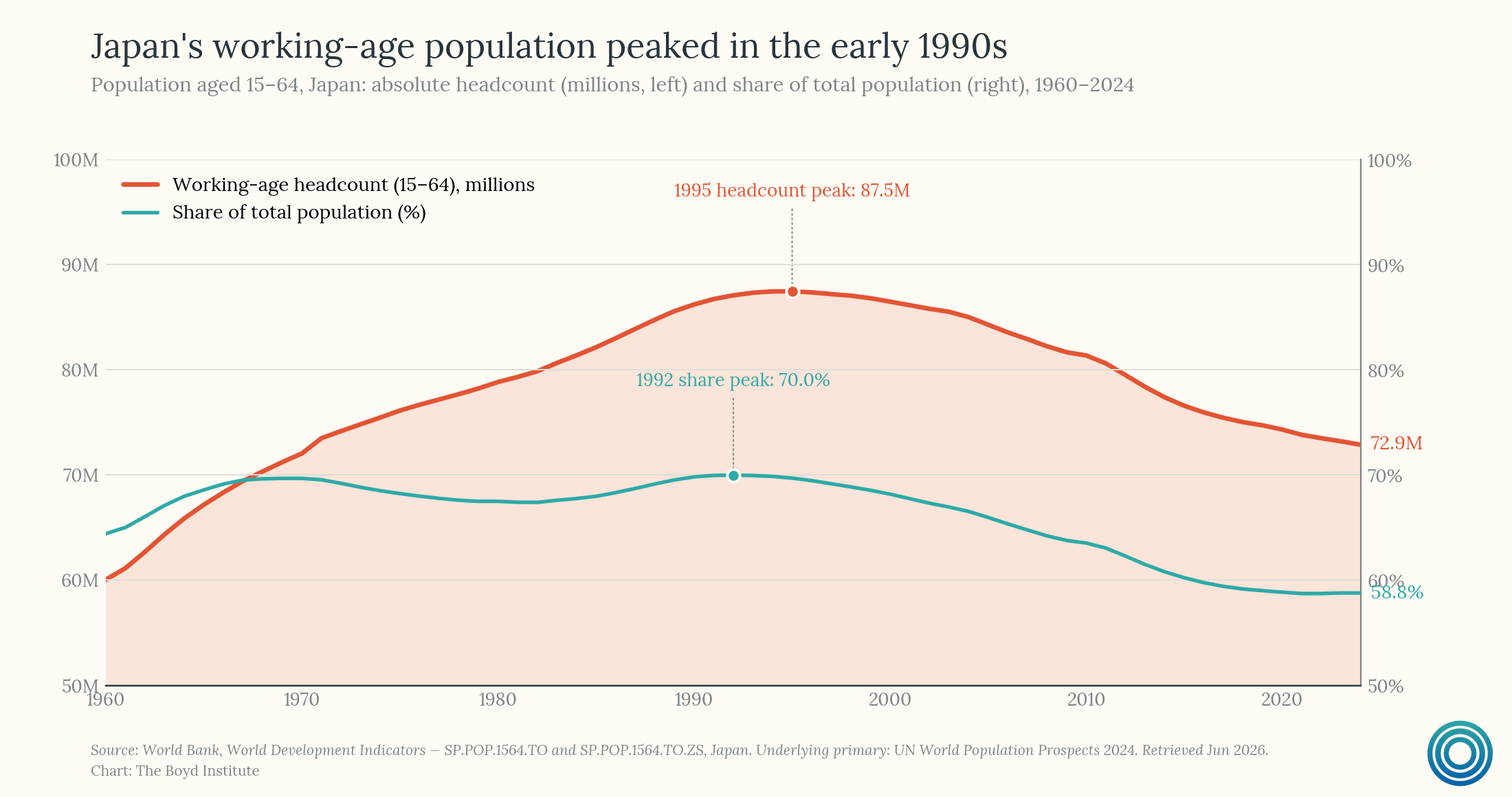

Now, none of this argues away demographic forces. An aging, shrinking workforce was never going to support 4% growth no matter what the BoJ targeted, and any honest account has to start there.

But the argument here is incremental: conditional on those structural drags, the policy arrangement let the productive base hollow much further than it had to — by suppressing the price signals (rising yields, a weakening currency, modest inflation) that would have pushed capital into more productive use. Former IMF chief economist Ken Rogoff puts the counterfactual — Japan without the bubble, the messy crisis aftermath, the policy errors — at roughly 25-50% richer per capita than the actual one. So yes, demographics did a lot of the work. But policy probably did a lot of it too.

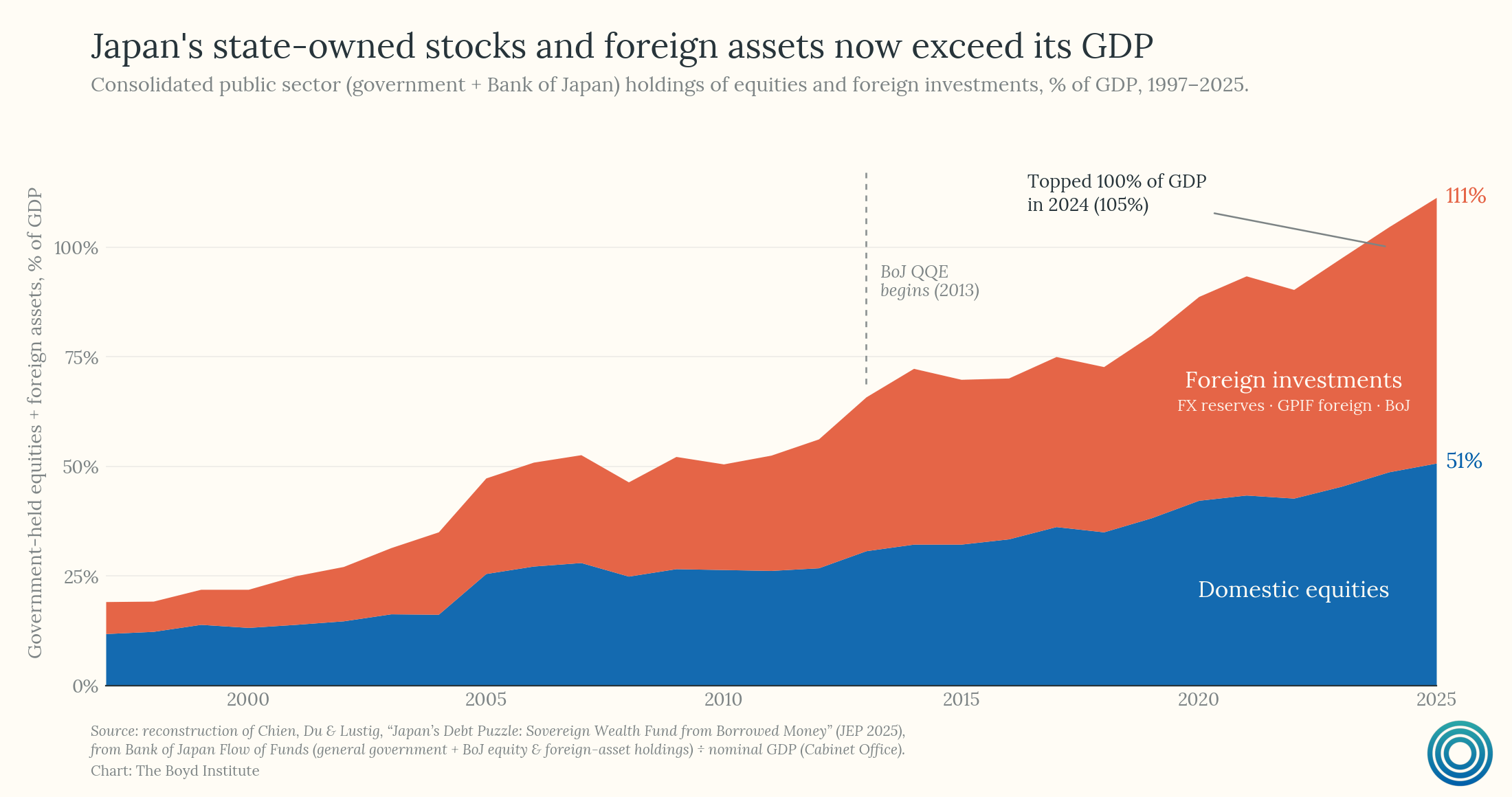

Crucially, what began as the BoJ’s failure to hit its target became, over time, the architecture the state built around. Chien, Du, and Lustig (2025) gives the cleanest recent statement of what that architecture was: a sovereign wealth fund built on cheap, borrowed money. Yen-denominated household deposits, effectively held captive, were what shouldered the costs of exorbitant JGB issuance. In other words, Japan’s private households and financial institutions financed a leveraged equity portfolio — a hedge fund of sorts — running a carry trade that belonged entirely to the state. Another way to think of this is that Japanese domestic savings were effectively channeled into funding the productive economic bases of other countries, while Japan’s own went unfunded (or at least, underfunded).

By the mid-2020s, Japan’s government-owned stocks and foreign investments topped 100% of GDP. Less than half of that portfolio was in domestic equities, with the rest in foreign assets — US stocks, Treasuries, and other sovereign bonds.5

The financial-repression literature (Carmen Reinhart’s work is canonical) is pretty straightforward on this. Sustained negative real rates against captive demand quietly liquidates the national debt. Ken Rogoff, Reinhart’s frequent co-author on this work, calculates these “very large losses on domestic savers through a combination of low real yields, currency weakness, and financial repression” to be on the order of 3–4% of GDP per year in many historical episodes.

To be sure, this liquidation cost is ultimately being paid by Japanese households, whose stock‑and‑bond participation still hovers around the low‑20s percent, versus roughly 60% of US households owning stock in some form.6 And so the much-admired price stability came in the form of an expensive tradeoff. A generation of suppressed dynamism was facilitated in exchange for basically never having a single bad week in the bond market. This tradeoff has played out even as the currency's safe-haven status meaningfully eroded, which is where we turn next.

The Cover Is Gone

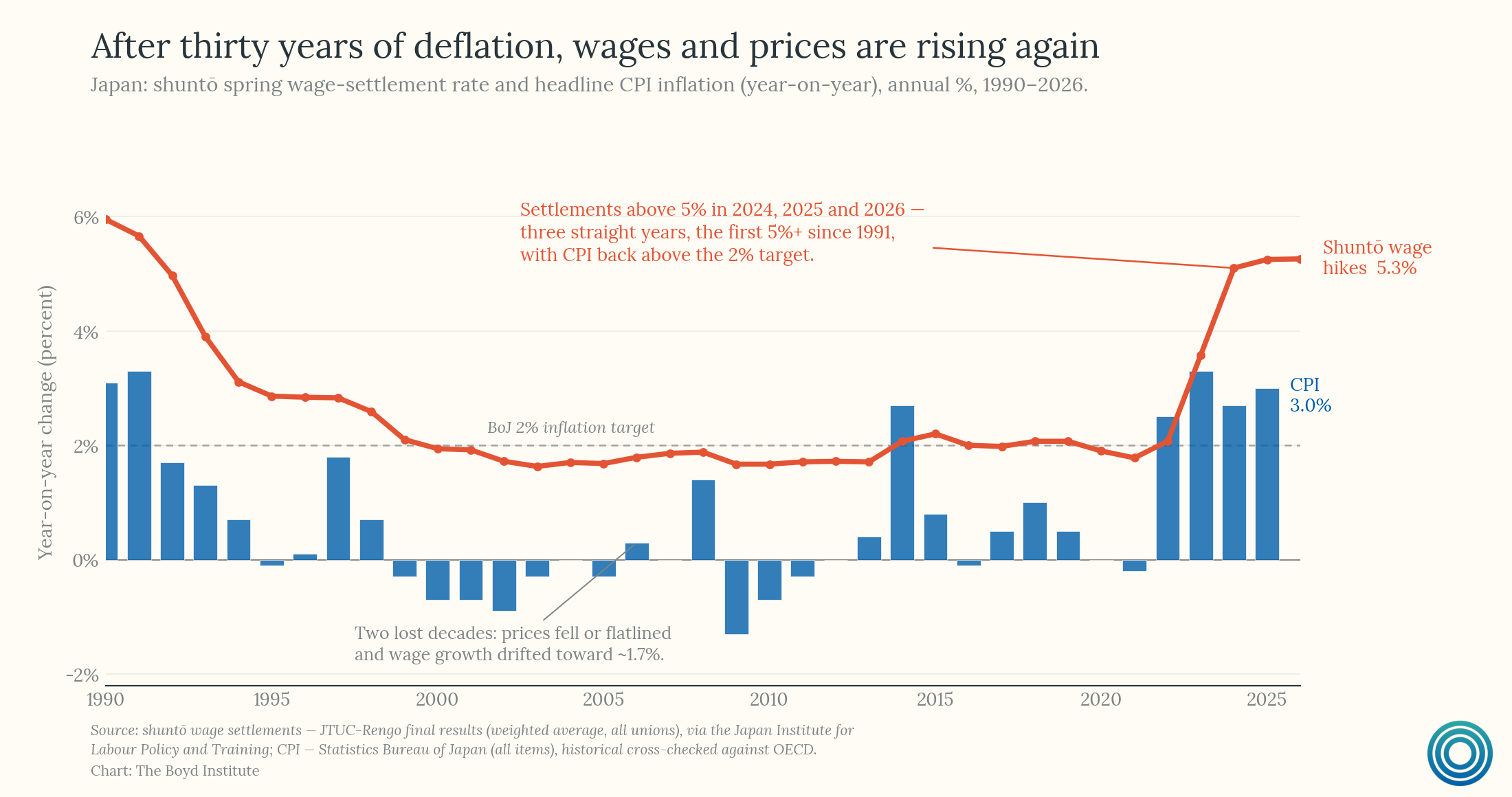

After thirty years of fighting falling prices, the conditions that made the machine work have now reversed. What Japan (theoretically) wanted — for inflation to normalize — has arrived: wage settlements above 5% for the third consecutive year, the strongest run since the early 1990s, and headline CPI that peaked above 4% in early 2023 and hovered above 2% for much of 2023–25 — partly imported through the weak yen coupled with rising global energy prices, partly a result of the domestic wage-price dynamic the BoJ spent two decades trying to summon.

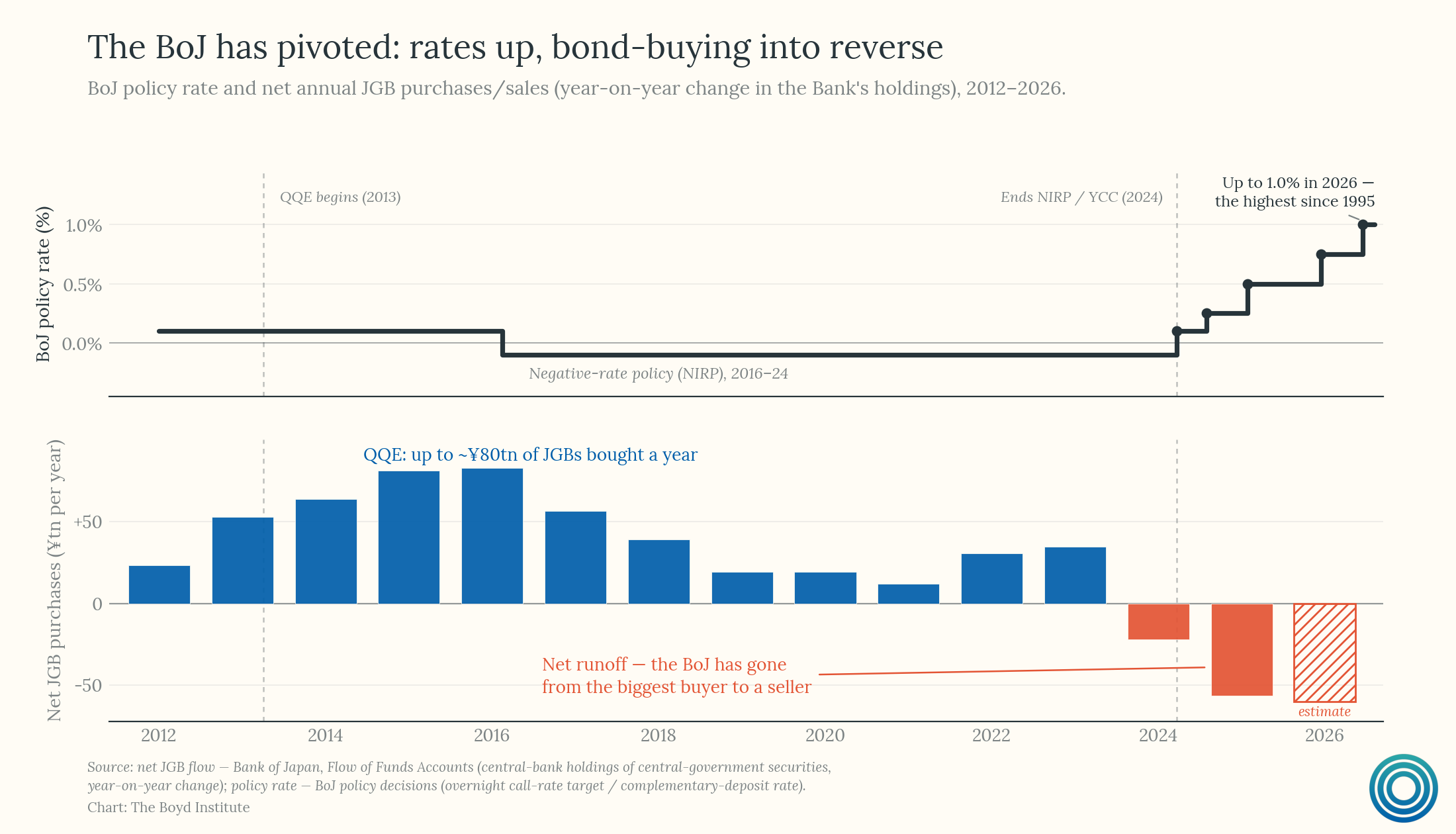

Without the deflationary cover, the BoJ cannot print to suppress yields without feeding the above-target inflation it must now instead contain. So it has been forced to pivot: it ended negative rates and abolished yield-curve control in March 2024, raised its policy rate to 0.75% by December 2025, then to 1.0% just this week — the highest since 1995 — and began tapering its large-scale asset purchases.

The instinct here would be to take cues from the bond market — from JGBs — as to the manner in which the monetary pivot is being digested by market participants. But that instinct is wrong (or at least incomplete). JGB yields, as a market signal, are a noisy and probably muted read on Japan‑specific distress, because the BoJ still holds just under half the JGB stock and remains an important buyer at the long end.7

So, if the inflation constraint does not bite via higher yields on government debt, where exactly is it binding?

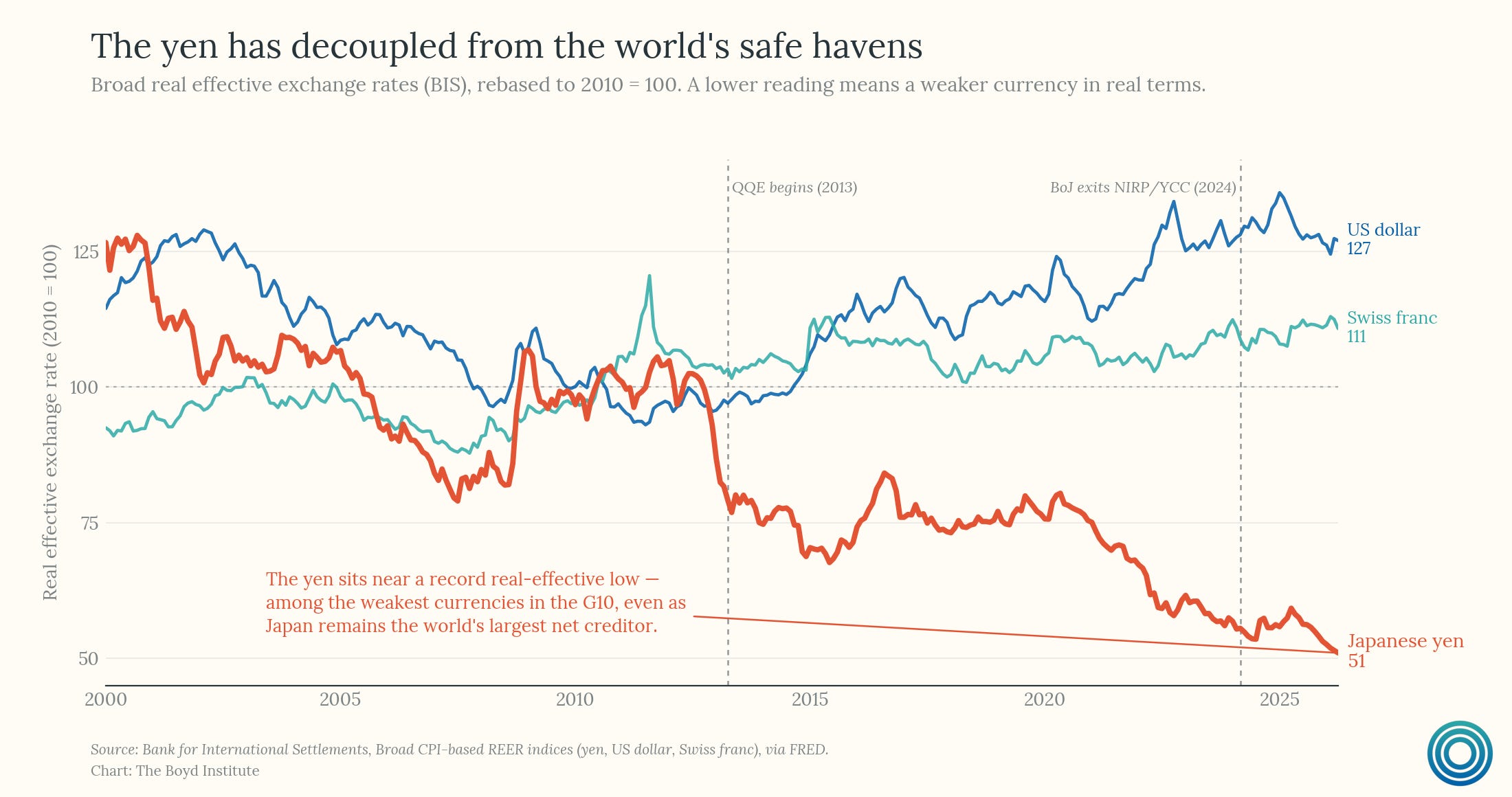

Robin Brooks’s central insight — that the constraint may alternatively take the form of currency depreciation, which can run out of control when debt gets too high — is useful here. He has adamantly maintained that a sovereign’s risk premium does not vanish when its central bank caps yields. Instead, the risk premium relocates, because yield caps plug just one of several release valves, “merely transform[ing] what would have been a bond market crisis into a currency crisis.”

The higher-signal thing to watch here is therefore the currency, and Japan’s currency is indeed behaving as though a crisis is already underway.8

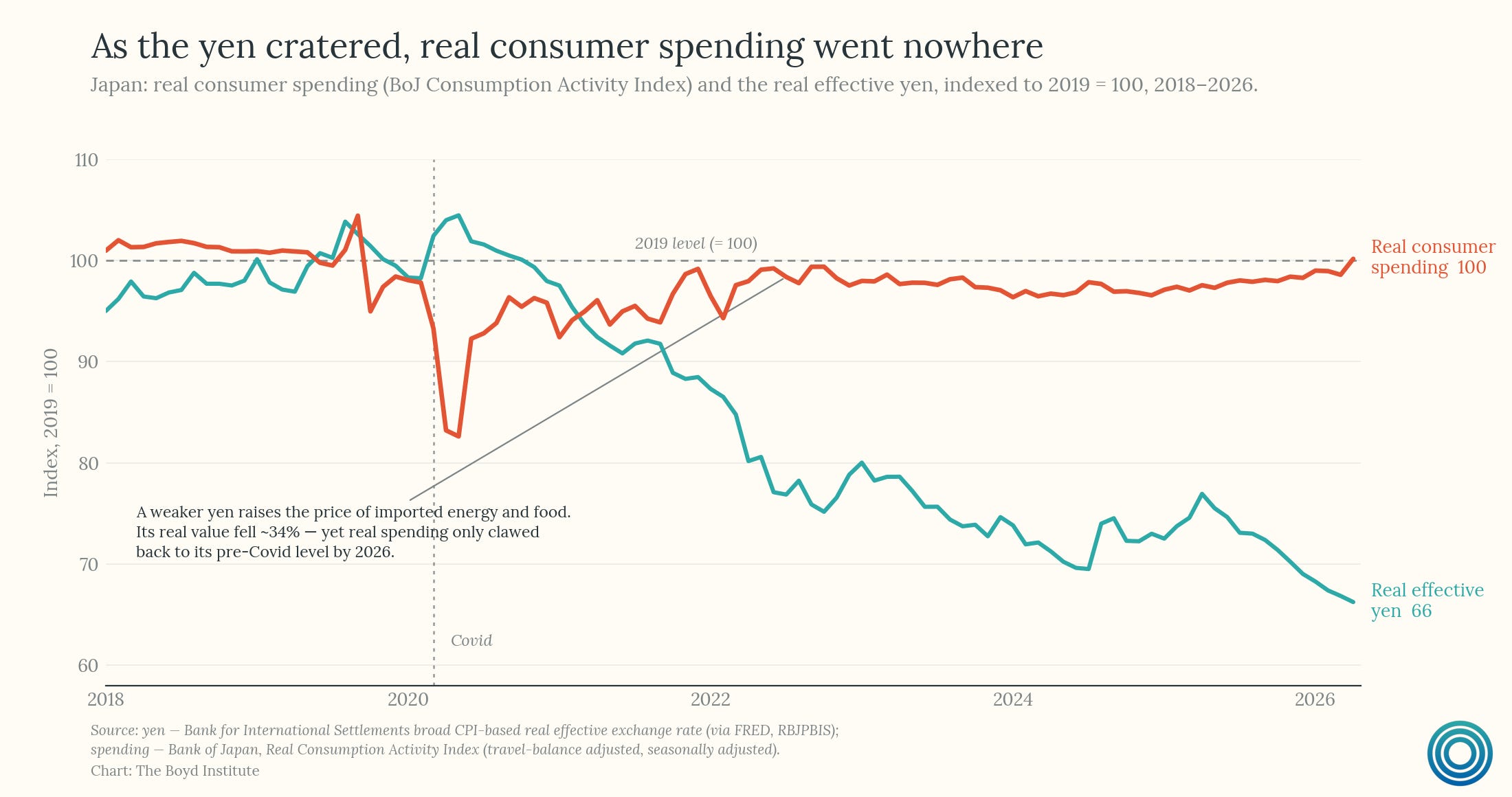

Importantly, a weaker yen is a major source of anxiety for the Japanese consumer, who imports a great deal of everyday goods like energy and food. As the yen has cratered post-Covid, consumer spending in Japan has only just recently clawed back to around its pre‑Covid level in real terms:

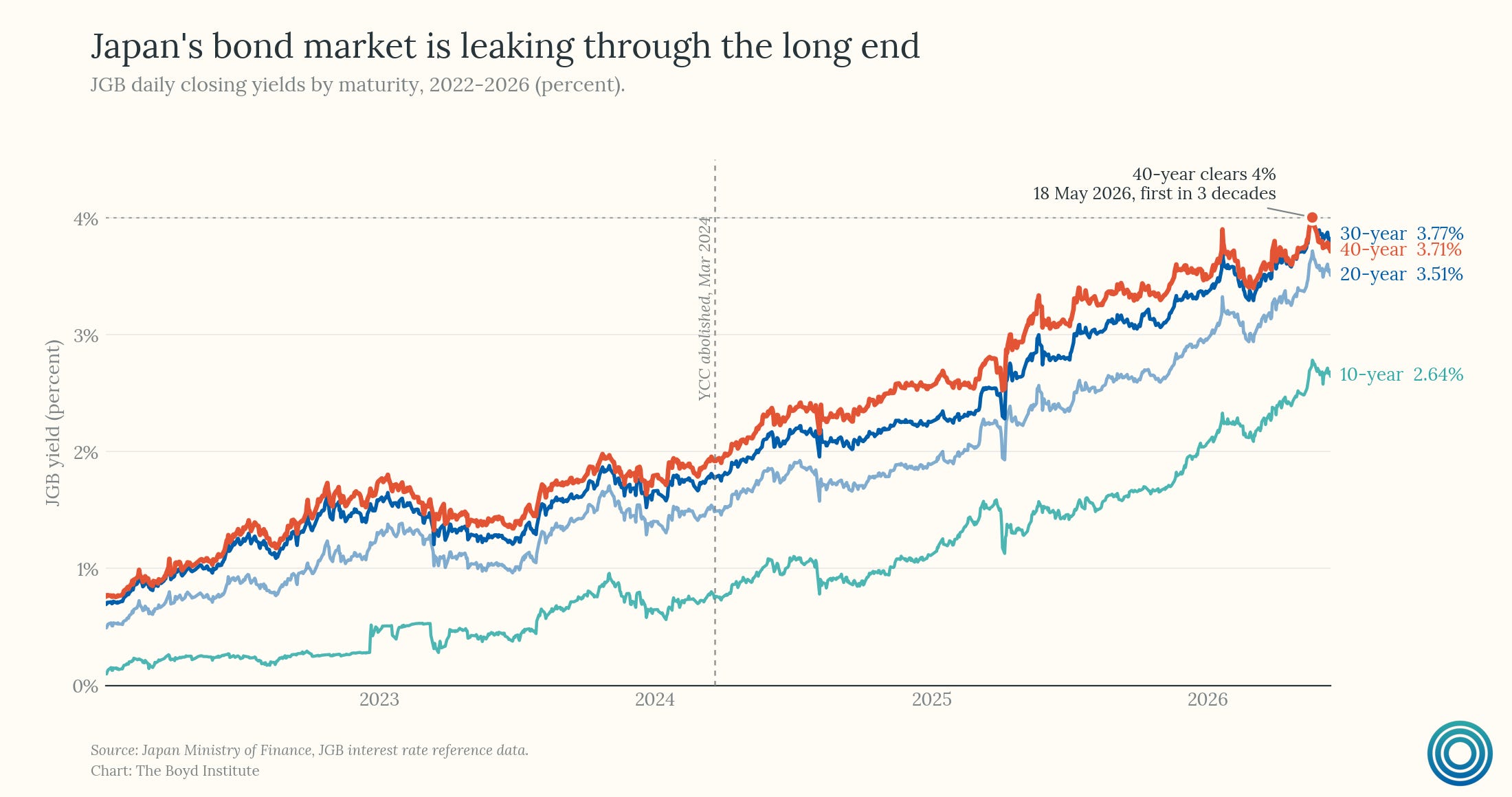

Worse yet, the bond market is still leaking because, muffled as the market may be, price discovery persists.9 The forty-year yield punched above 4% in January 2026, the first 4%+ print on any super-long JGB in roughly three decades, and the May 2025 twenty-year auction drew the weakest demand since 2012.

The Ministry of Finance has thus responded by trimming super-long issuance and shifting toward shorter tenors, the classic move of a sovereign under funding stress when the pain of higher yields starts to flow through.

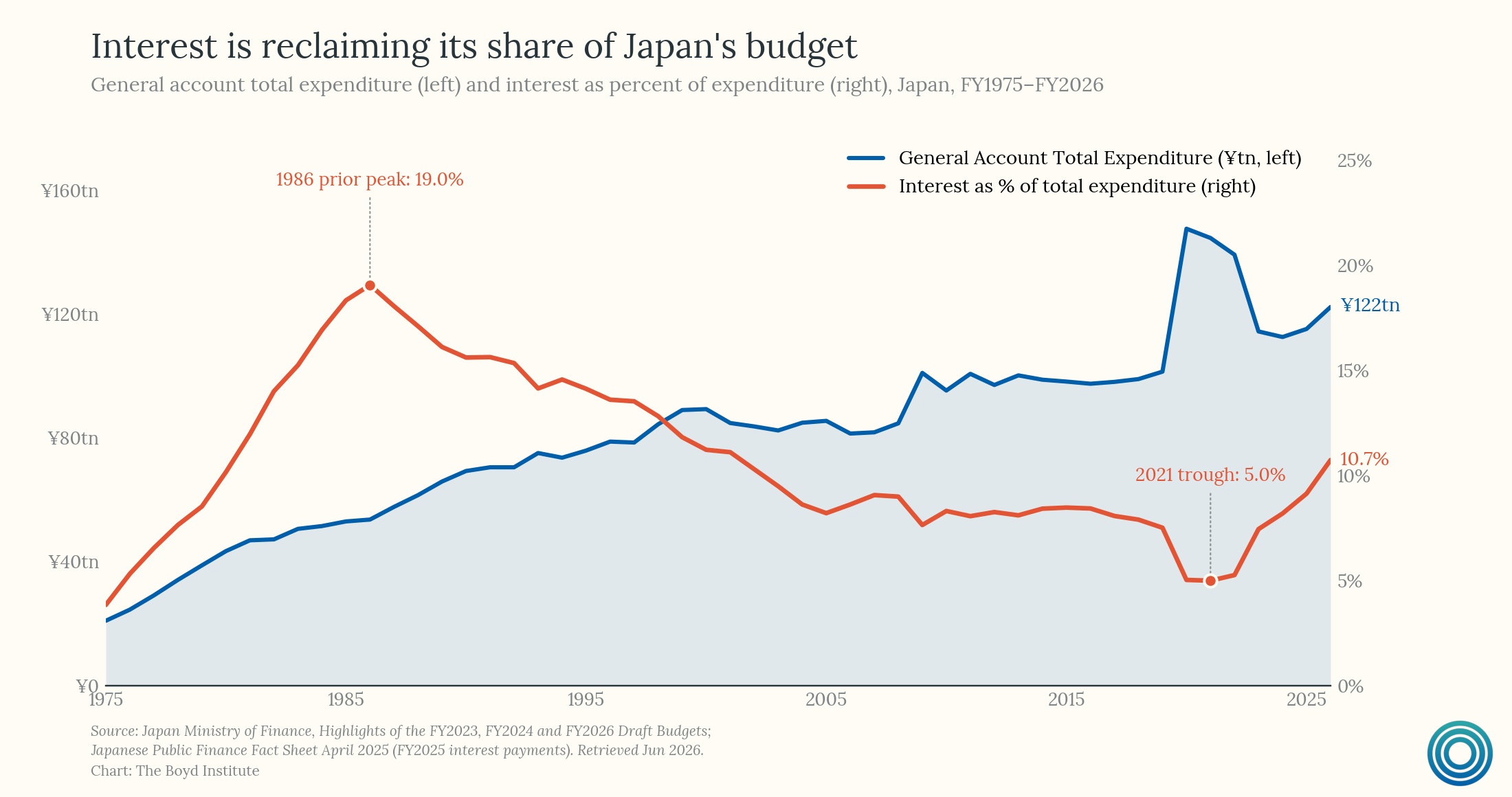

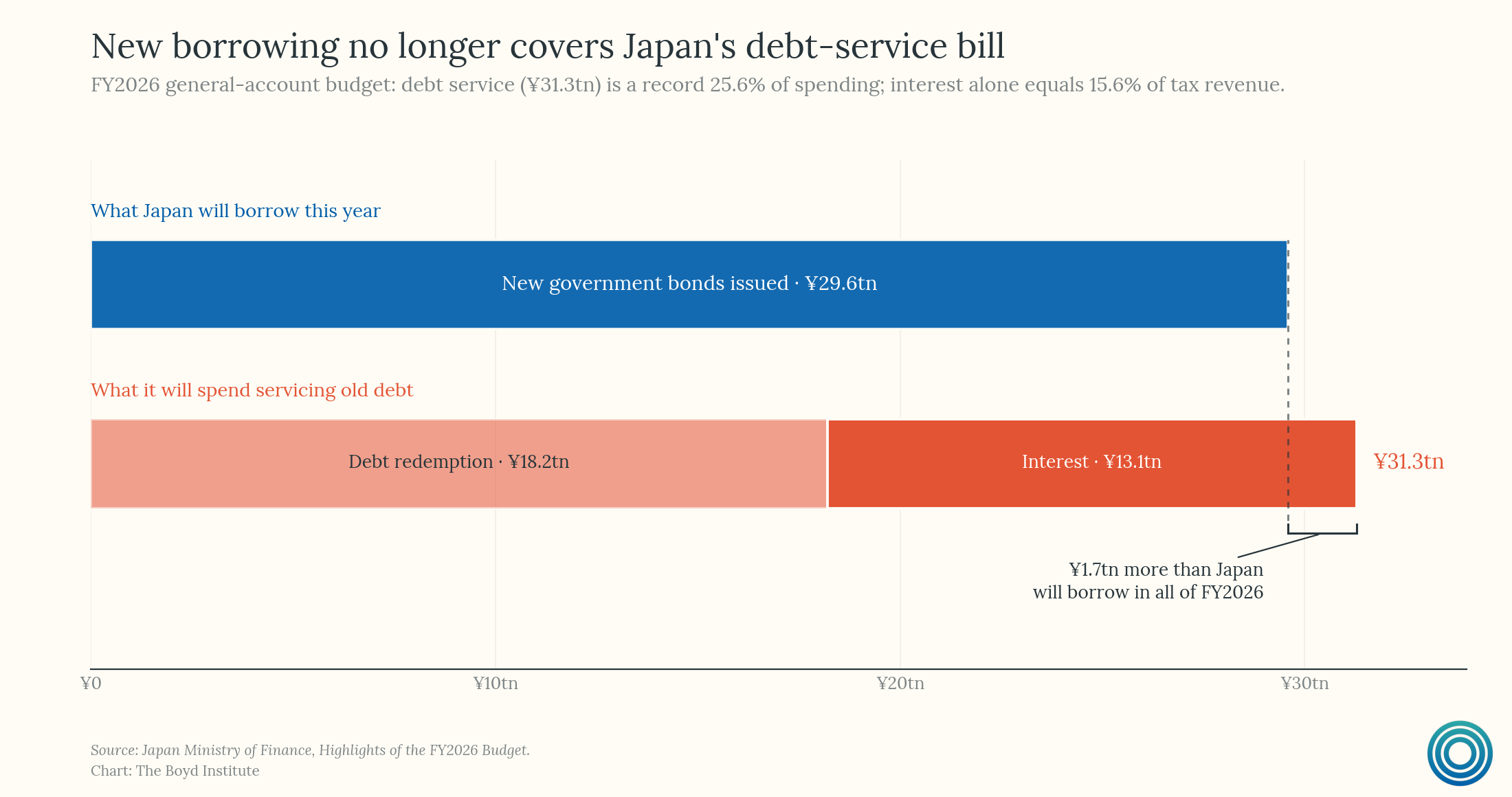

Nevertheless, on the fiscal side the Takaichi government — in office since October 2025 having run on subordinating the primary-balance target to growth — is pressing the accelerator, with a record ¥122.3 trillion budget financed by ¥29.6 trillion in fresh issuance. The fiscal-2026 budget assumes a 3% funding rate, the highest in twenty-nine years, with debt-servicing costs at a record ¥31.3 trillion, over a quarter of total expenditure. (Market practitioners named the ‘Takaichi trade’ months ago: stronger Nikkei, weaker JGBs and yen.)

But what the MMT-friendly “decades of calm” reading blatantly misses about exorbitant debt and duration is that the pain also arrives even when holding yields constant. As the ever-rising debt stock reprices, each maturing low-coupon bond is replaced by a higher-coupon one causing debt-servicing costs (interest payments) to rise even if yields stop climbing.10

It is telling that the central bank has stopped pretending. In a February 2026 speech, BoJ Policy Board member Hajime Takata attributed the rise in long-end yields to “a rise in the risk premium, known as the term premium.” This is, in no uncertain terms, the monetary authority acknowledging that the jig is up the market is now pricing fiscal risk into Japanese debt.11

Honest engagement with the dovish rebuttal survives all of this. An economist at Dai-ichi Life puts the rebuttal cleanly: in an era of inflation, rising debt-service costs come bundled with rising nominal GDP and tax revenue, so a bigger interest bill is not automatically a solvency problem. The IMF makes the same point structurally — nominal growth that exceeds the effective interest rate is precisely what has pulled Japan’s ratio down from its 258% pandemic peak toward 230%, even as gross debt stays the highest among major economies. This is also the Blanchard point, and it is correct as arithmetic.

A parallel rebuttal runs on the debt itself: net of the government's vast financial-asset holdings, Japan's net debt drops to around 130% of GDP. Consolidate the BoJ's JGB holdings as the intragovernmental claim they economically are, and the figure falls to on the order of three-quarters of GDP — lower than the US on the same measure.

Furthermore, Sumner’s “never reason from a price change“ rule says that rising stocks beside rising yields signal stronger expected growth, not panic, and Japanese thirty-year yields still sit more than a hundred basis points below the US counterpart. On the narrow question of whether Japan is experiencing something like the 2022 gilt rout, he is right — it unequivocally is not.

But the favorable arithmetic is a harder bet than it sounds. It requires nominal growth to durably exceed the marginal funding rate as the entire debt stock reprices, and Japan’s structural real growth runs near half a percent against a long-end now yielding 3 to 4%. Brooks’s framing cuts underneath the arithmetic entirely: a monetary sovereign can run out of fiscal space long before inflation forces the issue, because the constraint shows up first in the currency and the term premium rather than in a missed payment.

Markets, as Brooks wrote in January, are therefore telling Japan that it has run out of fiscal space. And the cost is very real, even if it gets paid through subtler channels than a sovereign-default headline would suggest — through captive savings, an eroded currency, the financial repression of negative real returns on deposits. Others have described this kind of erosion of creditors’ claims as a “stealth default.”

So while the dovish case on debt-and-deficits isn’t necessarily foolish or misinformed, it is unresolved. Japan, given the ambitiousness of its monetary experimentation, is doubtlessly where it gets resolved over the next several years. The harder question, and the one that matters for Washington, is whether the structural conditions that let Japan run the experiment in the first place are at all replicable.

Why Washington Can’t Copy Tokyo

Strip out the short-term rates set by central banks, and the long end of the yield curve is telling a similar story across the developed world at once: the same term-premium widening shows up in the United States, the United Kingdom, France, even Germany, the safe haven of old. None of this is unique to Japan in direction, only in degree.

Brooks’s frame is that this is a single synchronized event — the world used up its fiscal space during the pandemic, and markets now demand to be paid for holding long-dated debt everywhere. Japan is simply the leading edge, with a central bank that ran the suppression experiment longest and is unwinding it first, which makes it the diagnostic case. The question for Washington is not whether it faces the same debt-repricing pressures — it does — but whether it faces those pressures in the same way as Japan does.

The conditions, however, diverge sharply, for three main reasons.

1) What made Japan’s debt sustainable (for as long as it was) doesn’t translate to the US.

Japan financed thirty years of deficits out of a vast domestic institutional balance sheet: on the order of 90% of its government debt has been held at home, by patient, price-insensitive institutions — the BOJ, life insurers, banks, the postal system — with yen liabilities and nowhere to flee. Formerly the world’s largest net creditor for most of the period, running persistent current-account surpluses throughout, Japan lost its top-creditor spot in 2024.12

Now, price-sensitive marginal buyers exist where there predominantly used to be captive domestic ones: foreigners are now roughly 65% of monthly cash JGB turnover. In short, the conditions that made Japan’s exception possible — including a thirty-year deflationary window — are rapidly closing.

Crucially, the captive domestic creditor base is the single most important fact about what made Japan’s tolerance for debt so high for so long, and it’s just not something the US can manufacture. The US is the mirror image: the world’s largest net debtor, running structural current-account deficits, financing itself from abroad with foreigners holding a substantial share (albeit down to nearly a third) of marketable Treasuries.

2) The standard rejoinder is that the US has something better than domestic savers: the dollar.

The reserve currency commands a deeper, more durable bond‑demand base than the yen ever did: the dollar still accounts for close to 60% of global FX reserves versus only a few percent for the yen. The dollar’s “exorbitant privilege” is real, but it doesn’t rest only on market depth or network effects. A large majority of official dollar reserves and other “safe” U.S. assets are held by countries inside the U.S. security perimeter, and Eichengreen, Mehl, and Chiţu (2019) shows that military alliances boost the dollar share of a partner's reserves by about 30 percentage points. In a 2025 follow-up, the same authors estimate that credibly withdrawing those alliances would cause roughly 6% of US marketable public debt to be liquidated and long-term rates to rise by up to 80 basis points — adding around $115 billion a year to Treasury interest costs."

Thus a significant part of the reserve premium — over and above depth and network effects — is the alliance system. Pulling on the security architecture is pulling on the ballast of America’s borrowing position. The dollar’s role also brings its own asymmetric failure mode. Because it anchors global reserves, trade invoicing, and cross‑border funding, a disorderly dollar adjustment would not only hit US consumers via higher import prices, it would also propagate as a global shock through funding and credit channels.

Japan, by contrast, can endure a slow, grinding, decades‑long yen depreciation (painful for its own households but far less systemic) precisely because the yen is a much smaller reserve and funding currency.

3) Interest on the debt in the US isn’t merely a “distributional issue.”

Let’s assume that Mosler is right and that rising interest costs on Japan’s debt are merely a distributional issue — meaning that those higher interest payments amount to government transfers to domestic asset-holders (who skew higher in wealth and income). Whereas the vast majority of Japan’s public debt is held by domestic creditors, this would not hold true for the US, whose public debt is held by a significant contingent of foreign investors. In the US, instead of merely being a distributional issue, a meaningful portion of such debt‑servicing costs are transferred to bondholders abroad rather than recycled within the domestic private sector.

Final Takeaways From Japan

The right lesson from Japan is neither the dovish one nor its hawkish caricature — not “we have decades, relax,” nor “we are one auction from a Greek crisis.” Japan financed its reckoning in foregone growth, a captured monetary policy, and a currency now doing the adjusting, and it is making the payments in a compressed window with a government still pressing the accelerator.

Sumner makes the monetarist version of the warning — that the recent run of 6%-of-GDP US deficits arrived in unusually good years, with no recession, war, or pandemic. To read that calm as sustainable is to “miss the dog that didn’t bark.”

That leaves a narrow menu. Monetization is what Japan exhausted; it works until inflation returns, then inverts into the currency crisis now playing out. Consolidation exists on paper and dies in politics (in Tokyo and Washington alike) for reasons Buchanan and Wagner identified: democracies overspend on benefits that accrue to identifiable voters while the taxes are diffuse and deferred. Cutting those benefits concentrates pain on groups that vote, so the rational political move is to just avoid the pain to ultimately avoid the blame. In other words, the off-ramp exists but the politics necessary to take the off-ramp don't.

What then remains is the only exit that is neither austerity nor a currency-and-inflation event. And that is growing the denominator (GDP) faster than the bond market reprices the numerator (the debt). Productivity, as we’ve argued previously, is the only plausible path that makes the fiscal arithmetic survivable. Importantly, it requires investing in productive capacity underneath the debt stock rather than leaning further into mandatory spending.

The captivity of JGB demand ultimately flowed from household balance sheets. Japan’s postwar financial system steered household savings into guaranteed deposits — especially via the state‑run Postal Savings System and its successor institutions — which then funded JGB‑heavy balance sheets at banks, insurers, and public funds.

As the IMF notes, Japan’s “large pool of household assets, strong home bias, risk averseness, and large and stable institutional investors” meant that the household sector directly or indirectly financed about half of all JGBs, helping keep yields low even as debt ratios climbed.

Flow‑of‑funds data from the Bank of Japan show that Japanese households have consistently allocated an unusually high share of their financial assets to cash and deposits — well above comparable shares in the US and eurozone — which reinforces this structural channel from precautionary savings into government paper via domestic intermediaries.

The market-monetarist stance of monetary policy is defined by the gap between what the central bank is delivering and what it has committed to deliver. A central bank that targets 2% inflation and gets 0% is, in that frame, running a tighter policy than its target requires — full stop. This is the "never reason from a price change" principle Sumner inherits from Friedman and applies relentlessly. Low rates ≠ loose money. Deflation = tight money, by definition, if your target is positive.

Japan, as Sumner puts it, “ran some of the largest deficits in human history, and got basically zero growth in aggregate demand as a result.”

The Paul Krugman-style counter is that the BoJ was bumping the zero lower bound and the fiscal expansion was filling a demand gap that monetary policy couldn't close on its own. Sumner's response is that this concedes the wrong premise — central banks have additional tools (NGDP level targeting, explicit overshoot commitments, currency depreciation) they choose not to use, and not using them is itself the policy choice.

The debate is genuinely unresolved, but this essay’s argument doesn't require resolving it. Whether the previous calm reflected monetary failure or monetary success at the ZLB, the conditions are reversing regardless.

As Brookings puts it, yen depreciation is “really about Japan’s large debt burden, which forces the Bank of Japan to cap long-term government bond yields…In effect, this transfers weak debt dynamics from the bond market to the currency.”

With policy rates kept near zero long after other central banks tightened, and long‑end yields capped for years under YCC, defending the yen with aggressive hikes would have risked a domestic bond‑market and fiscal shock. Analyses of YCC show that keeping 10‑year yields pinned near zero while the Fed and ECB hiked hard made yen depreciation a mechanical consequence of BoJ’s choice to prioritize low yields over FX.

Estimate based on consolidating major public‑sector portfolios rather than any single official “sovereign fund” figure. We combine (i) the Bank of Japan’s bond and ETF holdings, which have reached roughly 100% of GDP when measured against the size of the economy, (ii) the Government Pension Investment Fund (GPIF) and other public pensions, whose strategic allocation splits equity almost evenly between domestic and foreign stocks, and (iii) central‑government foreign‑asset holdings described in Chien, Du, and Lustig’s work on Japan’s “sovereign wealth fund from borrowed money.”

National Survey on Securities Investment (via the FSA/MUFG summary) shows that only 13.6% of Japanese households hold stocks and 10.8% hold investment trusts, versus more than 90% holding deposits.

Even after ending YCC and starting tapering, BoJ is still running regular purchases across the curve (specifically across the 20-40y tenors). Furthermore, both BoJ’s own work and the academic literature on QQE/YCC find that high BoJ holdings and fixed‑rate operations distort the yield curve and affect transaction volumes and bid‑ask spreads, especially when its share passes certain thresholds.

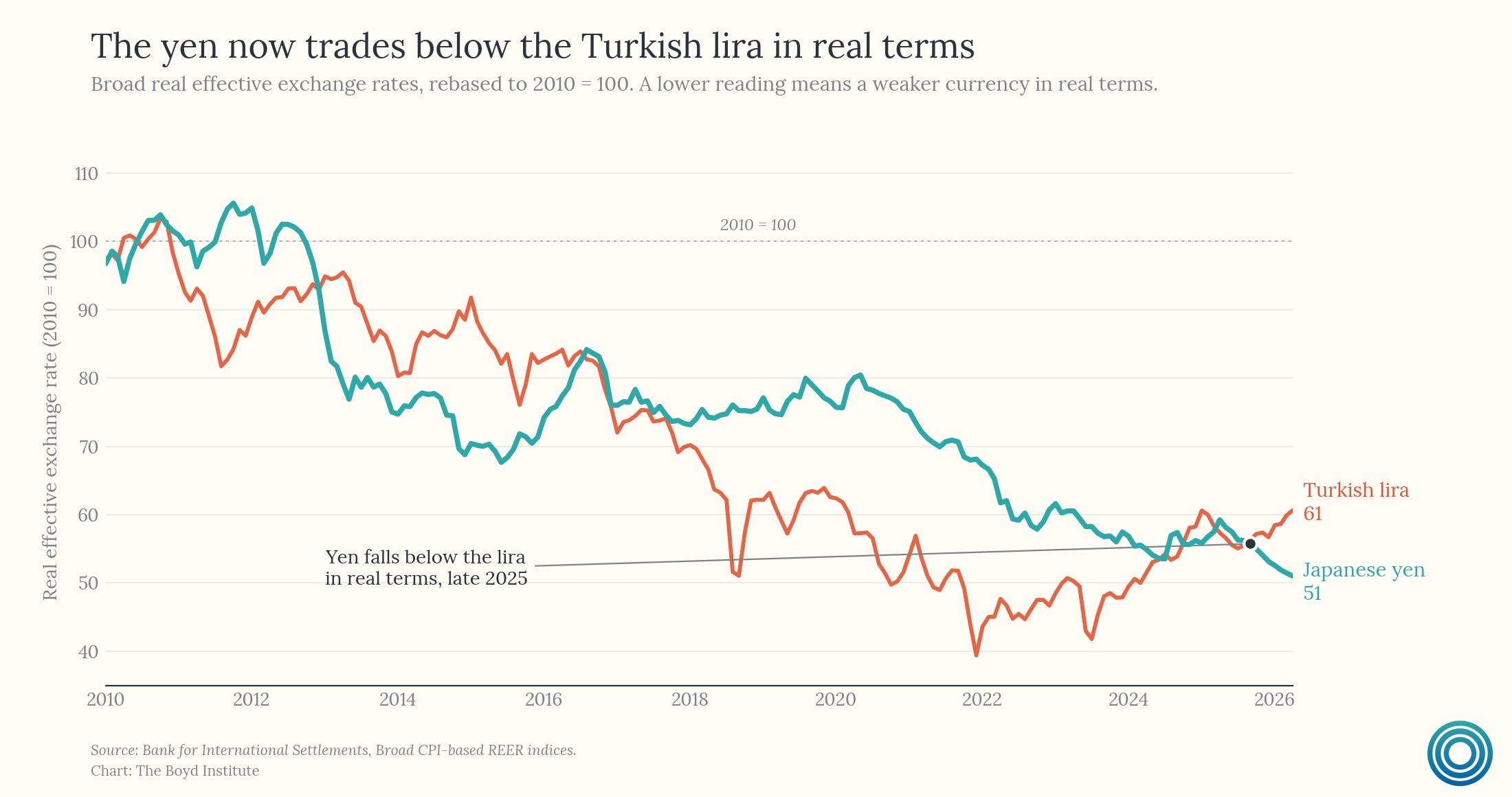

Brooks highlighted this interesting comparison: in real effective terms, the yen fell below the Turkish lira in April 2026. That is a developed creditor nation’s currency — considered for decades by global investors as the safe-haven currency — trading, in real terms, below a currency tied to one of the world’s most fiscally disastrous regimes in recent history.

It is also true that overseas investors now account for ~65% of monthly cash JGB transactions, up from 12% in 2009 — a structural shift from “captive” domestic buyers to more volatile foreign flows.

Early-on in the current sprint, we wrote on this dynamic playing out similarly in the US.

They also noted the term spread over the policy rate was approaching pre-QQE levels above 2% — the precise thing yield-curve control existed to prevent happening.

Japan's net international investment position has long been strongly positive, with net external assets in the ¥470–560 trillion range (roughly $3–3.5 trillion) — 70–80% of GDP in recent years. Japan held the world's largest-net-creditor title for 34 years before surrendering it to Germany in 2024.