Let's actually fix the generational contract

Don't put the Peter Banks's in charge of everything

On the libertarian right, Social Security is something of a boogeyman. Part of that has to do with the program itself, but part of it is also a more general disdain for old-age entitlements. If you’ve been following us at all, you’ll know we think the government spends too much on consumption subsidies, of which Social Security is the largest, and too little on investment in the future.

And yet... I still think Social Security is a vital national program. Because America needs an old-age support system of some kind to support the many citizens who reach senility without sufficient savings, whether through negligence or through circumstances beyond their control. Even the payroll tax strikes me as broadly reasonable — 12.4% capped at $184,500 of income (although if I was designing it from first principles I would probably eliminate the cap altogether).

Not only do I think a program “like” Social Security is essential for “other” people; it also gives me more confidence in the future and increases my willingness to take risks, because I know that even if I stumble, I will not starve in my eighties. And — without revealing too much — one set of my grandparents has only been able to survive at all because of Social Security. In my own case, family could probably have intervened without it, but it would have been an extremely messy and financially difficult situation for everyone, one I am frankly glad Social Security foreclosed. It is to my memories of them, as much as to the thoughts of myself as an old man, that I find myself turning, half-involuntarily, whenever I get too resentful about payroll taxes. In short, I’ve never had an issue with a public pension system.

No — my problem with Social Security is that we have never approached it with either the maturity or the self-awareness it deserves. Figuring out how to balance the social contract between working-age people — who will produce the goods the elderly consume no matter how we structure society, since no one is buying cars built during the Carter administration — against the genuine claims of the retired is an extremely important question, and one we as a country have essentially ignored. The few times we have tried to openly discuss improving the system, as in 1999 or 2005, our republic did everything but cover itself in honor.

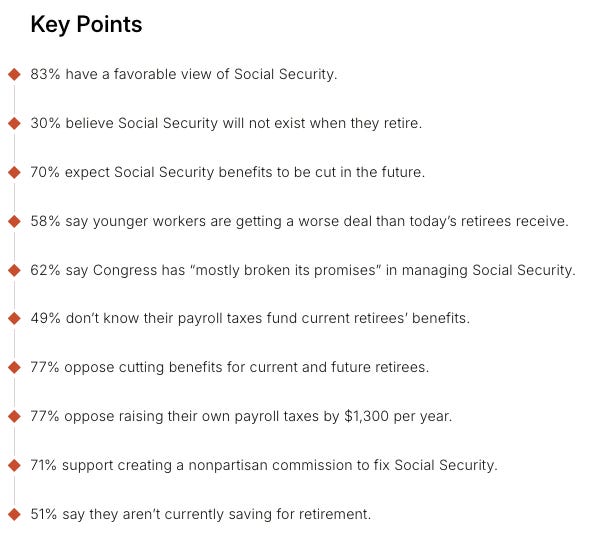

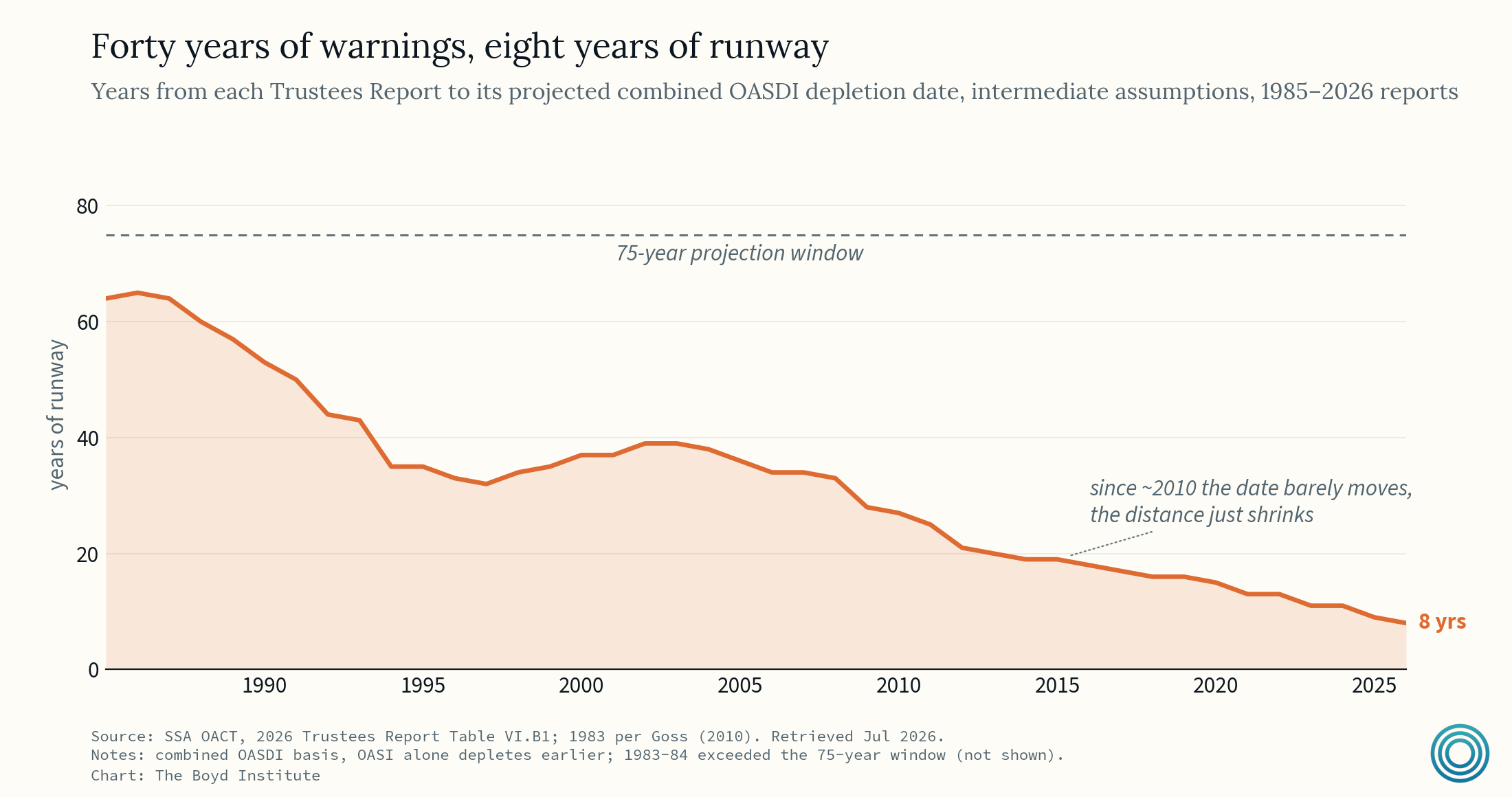

Even now, as we approach the program’s “insolvency” — the 2026 Trustees Report puts the date at the fourth quarter of 2032 — the vast majority of Americans don’t know even the basic facts of how our current social contract works. Just look at these key points from a recent Cato poll!

So this article is an attempt to think honestly about our generational contract: how we can fix it, and how we can make it more sustainable, so that when I retire some fifty-odd years from now I can do so in confidence, without the worming thought that I am robbing the future. My proposal is a bold, asymmetric one — I think that if it were implemented it would radically improve our long-run trajectory, but it is also necessarily early, and so what I want more than anything is for you to poke a million holes in it in search of the best possible solution.

We have known the solution for 50 years.

Since fertility dropped below replacement in 1972 — and arguably earlier because of how it structures payouts proportionally to income rather than prices1 — we have known that the Social Security system, as constituted, is not sustainable. This has been a mathematical certainty for over fifty years at this point, and although it has generated enormous amounts of discourse, it has yet to produce substantial action. You can see the degradation of the program in the simple ratio of workers to retirees, which has fallen from 5 in 1960 to only 2.9 today.

No one has ever thought the problem of solving this pension dynamic is, in some way, mysterious, which can make talking about it a little boring.

“Yes, we know it isn’t balanced!”

But it is worth talking about until we solve it! Because there has been a cornucopia of potential solutions. For example, we could have embraced the pay-as-you-go Italian model and just said that the plan for Social Security is to pay out what we can afford. In 1972, when fertility was below replacement but we still had a ton of young people, that meant a relatively large amount of money. Whereas in 2026, when there are fewer young people, it means a relatively smaller amount.

Or we could have invested the surplus in growth-linked assets. For essentially every year until 2010, Social Security brought in more in taxes than it paid out to recipients, but it was statutorily constrained to “invest” that money in Treasuries, effectively parking the money in the general fund. This meant we could spend the money on other programs, like Medicaid or the military, but it also hamstrung the returns the fund fetched.

For a while there was hope that immigration would make the system sustainable. And I do think it postponed the deadline — without the massive migration of the late twentieth and early twenty-first centuries we would probably already have crossed into insolvency. But it didn’t solve anything on a structural level. In fact, it turned the program into a Ponzi scheme of sorts that required perpetually rising absolute numbers of immigrants just to keep the system afloat.

We have tried to implement these fixes before. First, in 1999, Clinton proposed committing budget surpluses to Social Security with a slice invested in equities, through an independent, non-political board contracting private index-fund managers by competitive bid. But pushback from economists like Alan Greenspan over the risk of the government holding private assets killed it. Next, Bush ran for reelection in 2004 on a Social Security reform built around voluntary personal accounts, but the plan died in Congress in 2005, as is so often the case with reforms.

In other words, the problem has never been one of understanding, or lack of academic consensus, or lack of anything like that. The problem has always been the lack of anyone having the power and agency, or, to put it another way, responsibility, to act.

We want Boyd’s funding to come from core supporters who want to be part of the conversation. For that to work, we need people like you to step up now, while it’s still early.

Here’s what we’re offering:

Supporter ($10/month or $120/year): Access to our private Discord community and a quarterly call, where you can talk directly with us and other members.

Founding Partner ($1,000/year): Everything above, plus a monthly one-on-one call with us.

The Boyd Institute is a 501(c)(3). All contributions are tax-deductible. If you’re able to give through a Donor Advised Fund or make a direct donation beyond a subscription, it would meaningfully extend what we can do. Reach out to [email protected] for more information.

Don’t let academics run firms.

Broadly, I think that we can split most government functions into two categories. The first is engineering tasks, where the objective function is known and we’re optimizing for it under uncertainty. The second is truth-seeking, where the objective function itself is what we’re trying to discover, and there will always be room for fundamental disagreement.

Dan Wang’s Breakneck — which we read for our sprint on problem-solving — basically makes this same argument with his conception of China as the engineering state and America as the lawyerly state. And once you take that presupposition seriously, a lot falls out of it, since these types of organizations are simply good at solving different types of problems.

The two task-types have each evolved their own machinery, designed for their comparative environments. For truth-seeking, the most effective form of social organization looks something like the Talmudic tradition: constant open discussion, everyone sort of pseudo-equals, everything perpetually open to debate and input, where even the “losers’” objections are recorded for posterity. In other words, we never come to a definitive conclusion and everything is always open to discussion.

Engineering objectives instead demand an alternative way of structuring an organization, and you can see it most clearly in the American corporation. What has come out of centuries of Darwinian selection in the corporate environment is something that basically approximates elective monarchy. There is a goal — profit — that is ambiguous and complicated to pursue but easily definable, easily measurable, and hard to game. That last property is the key one. Without committing fraud, a CEO can’t perpetually fake profit, meaning there is basically no way to honestly (or sustainably) misrepresent the outcome, aka “teach to the test,” or fall victim to Goodhart’s Law.

Nothing is legally preventing shareholders from making all the decisions in a company — every choice that crosses the CEO’s desk could be put instead to a majority vote. We don’t do this because it is an obviously absurd system. Some amount of delegation is required, and we have found that finding the best officer, putting them in trust, giving them broad objectives, letting them cook, and assessing them only on outcomes works best.

You can take monetary policy as another example of an engineering task done well. There is a broad consensus on what “good” outcomes from monetary policy are — stable growth and low inflation — but how you actually achieve it in any given country, or any given year, is ambiguous and hard to plan for in advance. So we entrust a single body to manage it independently, subject to review.

There is a large body of academic work supporting everything I’m saying above. The question of why some tasks get open-ended negotiation while others get a hierarchy and a boss is one of the oldest in economics, and the answer that eventually won the Nobel is that tasks get matched to the governance structures suited to their attributes. The same test has been run on government agencies directly: where outcomes are observable, an agency can operate like a firm; but where they aren’t, it can’t.

And so we should be willing to say something that people like me find uncomfortable: I don’t think the lawyers and the academics and the journalists should be in charge of everything. There are areas of human life that are better run by people who are not like Peter Banks. I’d be a decent academic in another universe. But temperamentally, I am not the kind of person who should run ExxonMobil. I would spend all my time theorizing, having open discussions, never really coming to a final conclusion, forever refining and integrating everybody’s perspective to surface as much of the Truth as possible. That is simply not what you need to do to run ExxonMobil. Much of America looks to me like what would happen if people like myself were in charge of everything.

The proposal

Take pensions away from the lawyers and give them to the engineers by chartering an independent Social Security Trust under two plain mandates: keep the system solvent for the long run, and keep retirees’ standard of living as high as that solvency allows.

Here is how it would actually work. Just as now, the Trust collects the payroll taxes — but rather than being forced to park its reserves in Treasuries, the Trust has full agency over how it invests. Critically, it also holds the payout parameters: benefit levels, the retirement age, the formulas.

Congress and the President would provide oversight by appointing the Trust’s board and retaining removal powers, while the Trust would manage all aspects of Social Security finance and benefits other than the payroll tax rate. In governance terms, it would resemble something like the Federal Reserve’s framework — an independent body operating under a statute that sets clear objectives. Similar to the Fed’s dual mandate of maximum employment and stable prices2, the Trust should face a real tradeoff between two competing goals: namely, 1) long-run solvency, and 2) benefit adequacy. This dynamic would optimize for sustainability because a board that maximized solvency alone would simply cut benefits, while a board that maximized benefits without regard to financing would risk insolvency. The advantage of such a framework is that both goals could be measured, tracked, and audited publicly using standard actuarial and program‑performance metrics.

But for any of this to work, the Trust would need to have a surplus, meaning that it is bringing in more in taxes than it pays out — a precondition for building a reserve. Which naturally raises the question of “how?” Ultimately the options would be either to raise taxes, cut benefits, or some combination of both.

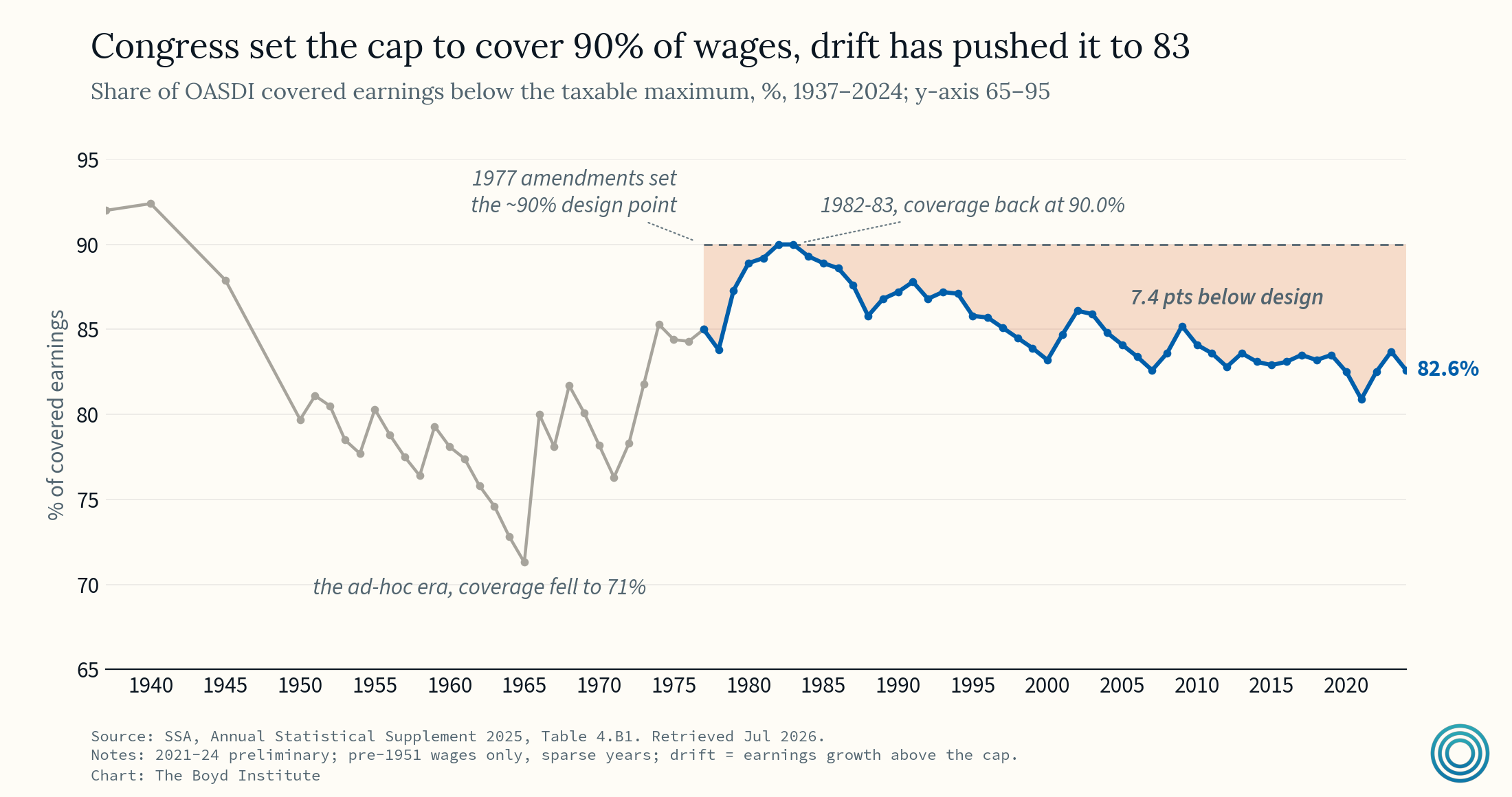

If I was in charge, and in this hypothetical I am, I would remove the payroll tax cap, turning it into a flat tax on all payroll income. Or even just raise it to cover ~90% of national wages as it did in 1983, rather than ~83% today.

In addition to this, I would follow the technocratic consensus and cut payouts for high-income recipients by changing the payout formulas. At the end of the day someone has to foot the bill, and wealthy retirees are the ones most poised to foot it. These people are some of the richest in the country and don’t “need” Social Security to survive — I’m thinking here of my other set of grandparents.

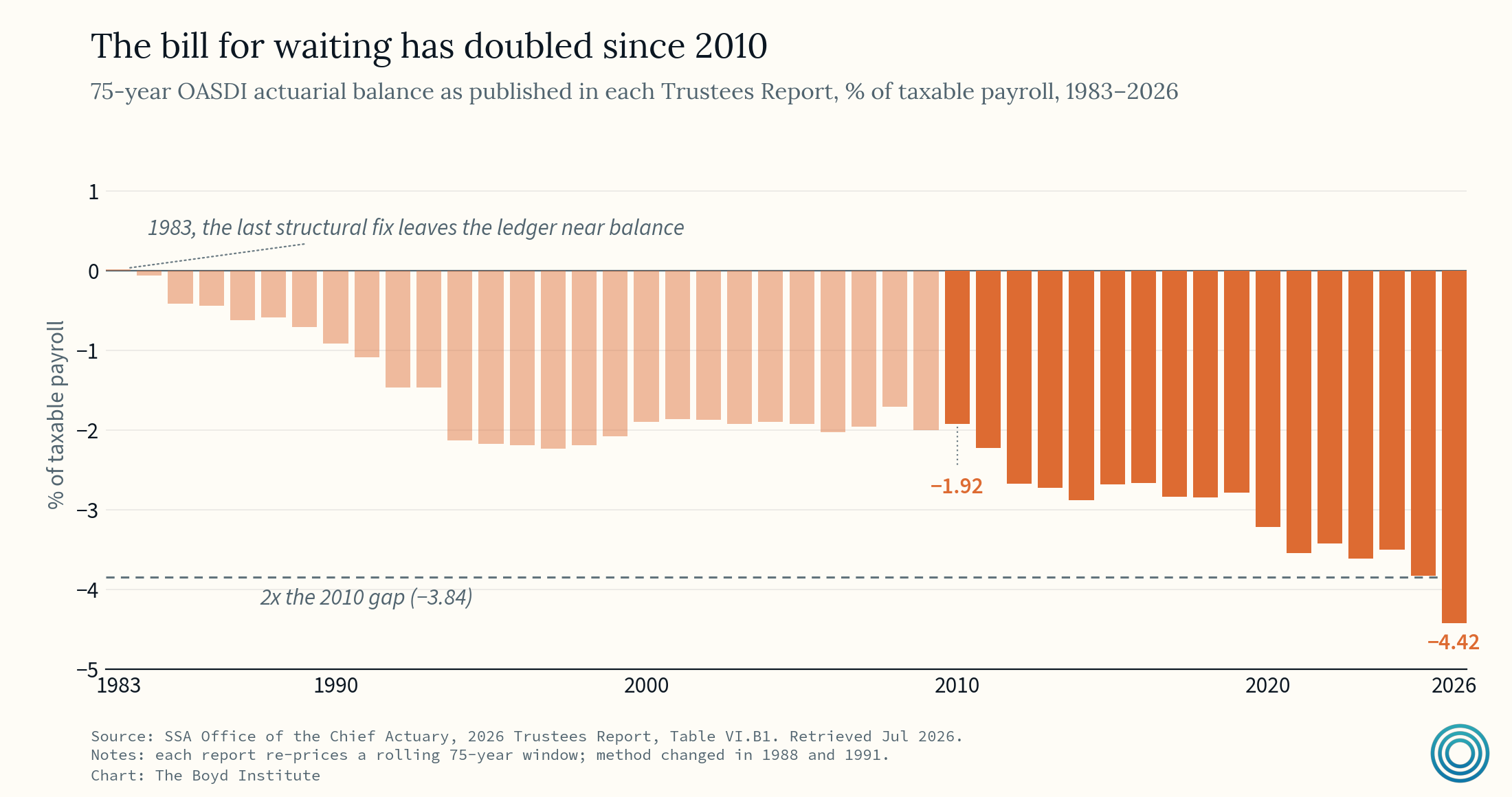

It is true that my generation will have to pay twice — covering today’s retirees while pre-funding our own retirement. But alas this is the heavy burden created by postponing a known problem. A burden which will only grow heavier with every year that we delay.

Corporate governance is a solved field.

In America we are culturally primed to prefer the lawyerly arrangement in our government but I would claim that the question of how to run large organizations well has largely been “solved”, at least when outcomes are measurable.

To see why, the place to start is “moral hazard,” because Social Security is itself a textbook case. When people form contracts, the contract can change how the person behaves after signing. If Social Security did not exist, people would save more — this is trivially obvious. Since if you thought that failing to save meant dying in a ditch, or your kids taking care of you, saving would be worth more to you than it would be in a world with Social Security. The classic estimate of the savings displacement was enormous, but probably overstated. The true size is still argued over, but the direction follows from the logic, and even a small effect is reason enough to design the contract well.

In order to address this problem, the solution is writing a better contract. We approximate this already with things like people who earn more, get more; or if you retire early you get less. The whole idea of this is to try and reduce some of the “perverse incentive” created by a public pension. As I said this is a well trodden area.

My PhD program was, nominally, Accounting — “information economics” — and most of what I studied was corporate governance. The running joke in that field is that it is de facto solved. Being into it is a little like arriving in a physics program really excited about Newtonian mechanics. If you want the whole subdiscipline in great detail, the book Corporate Governance Matters is the place to begin.

What that solved field has found is that when a principal must delegate execution under ambiguity, the best possible design is to entrust a single agent with simultaneous power and simultaneous responsibility — full control rights over the organization — while the principals retain complete and total impeachment control, and nothing else. Then the principal should assess the agent exclusively on outcomes. You don’t go to the agent and say: man, how are you doing? You’re a pretty sick guy, you have some interesting ideas. That is the philosopher-academic-lawyer approach to life, and it is precisely how you must not assess an executive. Instead shareholders should be laser focused on if outcomes improved or not, and nothing else.

Two design details fall straight out of that literature. The Trust must never control its own revenue — an agent that sets its own budget maximizes itself — which is why the tax rate stays with Congress. And the theory also explains, with no appeal to stupidity or villainy, why the current owner, Congress, never acts. Since the cost of fixing the pension is concentrated, immediate, and easily traceable to them, while the benefit is diffuse, decades away, and credited to no one, deferral is the only rational strategy today — as it was in 1972, and as it will be right up to the point of disaster.

To reiterate, monetary policy is the clearest case of this model already working in practice. It has been shown again and again that when politicians run the state's printing press, they run the currency into the ground — you can watch it happen wherever they lean on the central bank, as in Turkey, where a stretch of pliant policy bought a short-term sugar high and then inflation touching 85%. Handing that lever to an independent body of technocrats instead — still under the careful supervision of our elected representatives in Congress — is a big part of what has kept inflation stable across the developed world without sacrificing real growth.3

Since pensions have the identical disease, they need a similar cure. Fine for money, you might say. Has anyone actually done it to a pension?

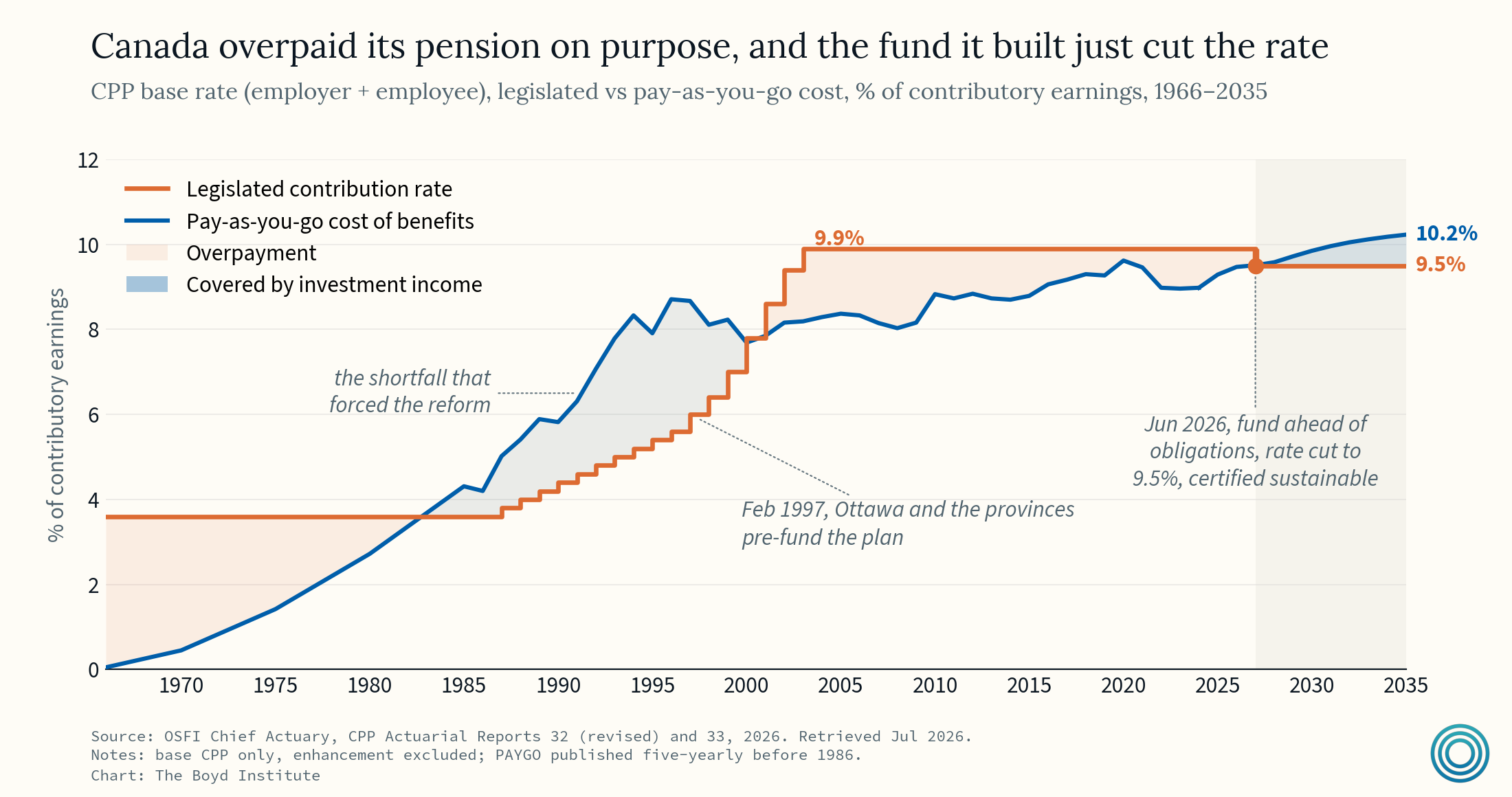

Canada already did it.

In 1996 the Chief Actuary projected the Canadian pension fund would be exhausted by 2015, and pay-as-you-go costs were marching toward 14% of wages. To avoid this cliff, Ottawa and the provinces struck the deal in February 1997 which effectively solved the problem we are now facing.

Their fix had three parts. First, they raised rates from 5.6% to 9.9% by 2003 — deliberately above pay-as-you-go cost, to pre-fund the plan — alongside modest benefit trims. Second, they set up the CPP Investment Board, which is an arm’s-length Crown corporation with an investment-only mandate — maximum return without undue risk of loss. Third, they made it so that the independent Chief Actuary has to re-certify the plan, and if the numbers slip below an acceptable threshold while politicians can’t agree on a fix, a statutory default fires raising contributions by half the gap, freezing benefit indexation until the next review.

The result has been unambiguously good. With the fund growing from a C$12 million initial transfer in 1999 to C$793 billion in fiscal 2026, earning 8.8% annualized over the past decade; the Chief Actuary has certified the plan is sustainable for the next 75 years; and the contribution rate actually required is now below the rate on the books because of capital gains compounding. From the 2030s onward, investment income will carry a growing share of every pension cheque, lifting that burden off taxpayers. Already this June with the fund running so far ahead of its obligations, Canada cut the base contribution rate from 9.9% to 9.5%, effective 2027.

Canada has split my Trust into three organs, rather than consolidating this into a single agent with comprehensive responsibility, which falls short of my principal-agent ideal but is still much better than what we have today in America.

But won’t it create new problems?

Yes. And it would be naive to pretend otherwise. The question in policy debates is always about balancing tradeoffs — but in this case I think the tradeoffs are visible, and so as a result easily monitorable, in a way that slow-moving solvency dynamics are not. Most objections I can think of essentially collapse into the same point. You cannot depoliticize trillions of dollars in investments.

Here are two versions of the same basic argument.

Politicians will abuse it.

This is Greenspan’s 1999 objection: government ownership of private assets, he warned, would risk sub-optimal capital markets and political direction of investment. He was of course right that the risk is real. But two counter points of sorts. First, we already face this problem on a smaller scale with the federal government’s own Thrift Savings Plan which holds ~$1.1 trillion of federal workers’ retirement money, as well as state and local pensions. Broadly this has produced only limited distortions, to the point it may come as a surprise to you it exists already. Second, the risk of political abuse is a reason for, not against, taking control away from Congress. Since although the Trust has the risk of being politically captured, Congress is by construction a political body. Ultimately if you want to invest a public pension in capital markets, an obvious improvement, any system will face this same problem.

The payout function is too important to leave to technocrats.

Perhaps. Most technocrats like to avoid redistribution questions, instead leaving them to politicians. But Congress has had an exclusive monopoly over this value question for ninety years and has, simply, refused to answer it. An automatic system like the Canadian one would also be fine but in my opinion it would needlessly constrain the Trust’s ability to act. By construction something like the Canadian system still takes power from representatives and gives it to technocrats, but in this case it assigns that power to only the technocrats of 1997, rather than the ones of today.

However, even if they make the best possible set of choices, it is quite possible people will simply not trust them. Personally, I think a Trust that clearly communicates its objectives, and both has and takes real responsibility, could genuinely win the public’s trust. It would, of course, require Congress and the President standing behind it during the initial difficult years, as with any pension reform — but legitimacy of this kind is earned in arrears, accruing to any body that spends long enough proving it can be handed something important and not wreck it. In brief, I suspect it would have the same trust arc as the Fed, which is also forced to make important distributional determinations without regard for political economy.

Conclusion: a calm decade, or the blistering sprint

Like I’ve said, this is an asymmetric idea, though it is mostly a synthesis of programs already running elsewhere. And ultimately, we will do something — because when a pension system finally hits the wall, the options left are ugly: outright insolvency, or hauling in a team of technocratic economists to rebuild the thing in a hurry. It has happened over and over. Italy in 1995, and again in 2011. Brazil in 2019. Greece after the financial crisis. In every case, a neutral, expert body ends up holding the lever anyway — just at the last possible moment, with no room left for anything but austerity.

We are on the same track. If we do nothing, we will hand the redesign to the same people I’m saying should be in charge anyway. The only real choice we actually get is whether we do it calmly, over a decade, with the full menu of options still open — or in the blistering, histrionic sprint, after the cuts have already landed.

I know which option I prefer.

The system indexes initial benefits to wages rather than prices, so every gain in productivity automatically widens what it owes, with no matching rise in what it takes in. In other words, the better the economy does, the faster the promises outrun the funding.

“Historically, there has often been some trade-off between inflation and unemployment” — this trade-off is the so-called Phillips curve relationship.

The rejoinder is always Japan: enormous debt, a central bank that has swallowed much of the bond market, and still no currency crisis. But as we've argued before, Japan is not the counterexample it looks like.