Weekly Roundup #6

Housing | Tax policy, Rent controls, and more

EXECUTIVE SUMMARY

Welcome back to Boyd’s weekly roundup series. This week’s roundup includes:

Newsflow on:

Listings and time on market are up, while the gov’t shutdown impacts demand; and

The ROAD to Housing Act is on hold while the government remains shut down.

Academic research on:

The impact of US tax policy on housing prices and mobility; and

Evidence from San Francisco that rent control reduces rental supply, leading to higher prices

Additional reading on:

Evidence pointing towards home prices falling while rents remain stable;

Why squeezing homebuilders is a misguided approach; and

The history of credit driving homeownership in the US.

If you haven’t already, do check out this week’s articles on 15 different "ground truths” we've established as well as our video interview with the NYU Stern finance professor and housing expert, Arpit Gupta. Additionally, tune in to the Substack Live session Monday (10/20) where Peter and Will are going be discussing all of the below as well as engaging with comments/Q&A.

Now, the roundup.

COMMUNITY POLL

This week we’re asking readers to look around the housing market corner and put on their prediction hats. Only one of these four can credibly happen first, since the timing and causes differ. For example, a construction boom is unlikely to coincide with an immediate price drop; a mortgage rate collapse does not require a rent or price crash; a surge in transaction volume usually comes after price/rate changes.

So these four scenarios are somewhat mutually exlusive, while the probability of each is faily similar.

NEWSFLOW

Redfin: New listings of U.S. homes for sale rose 4.1% yr/yr, the biggest increase in over four months, as more sellers enter the market hoping lower mortgage rates — the weekly avg. mortgage rate is 6.3%, just shy of its lowest level in a year — and a small improvement in affordability will attract buyers. Pending home sales are moving in the opposite direction, though, falling 1.2% yr/yr, the biggest decline in over five months. Homes are also taking a week longer to sell than they did last year. “Buyers are hesitant because of concerns about job security and high mortgage rates,” said Jo Chavez, a Redfin Premier agent in Kansas City, MO. “Even though rates have come down from their peak, a lot of people are waiting for sub-6% rates before they buy.” Furloughs and potential layoffs from the government shutdown are also weighing on demand in certain markets that are home to many federal employees, like KC and DC.

Fox Rothschild: The ROAD to Housing Act — a wish list of 27 bills (with 23 enjoying bipartisan support) which passed the Senate 77-20 on Oct. 9 — targets systemic bottlenecks that have constrained affordable housing for years: antiquated zoning rules, bureaucratic delays, insufficient capital investment, and rigid program caps. If it becomes law, it could reshape how housing authorities, developers, lenders and local governments approach affordable housing development. But there’s a catch. The bill needs House approval, and Speaker Mike Johnson has vowed no votes until the Senate agrees on a spending bill to reopen the government.

ACADEMIC RESEARCH

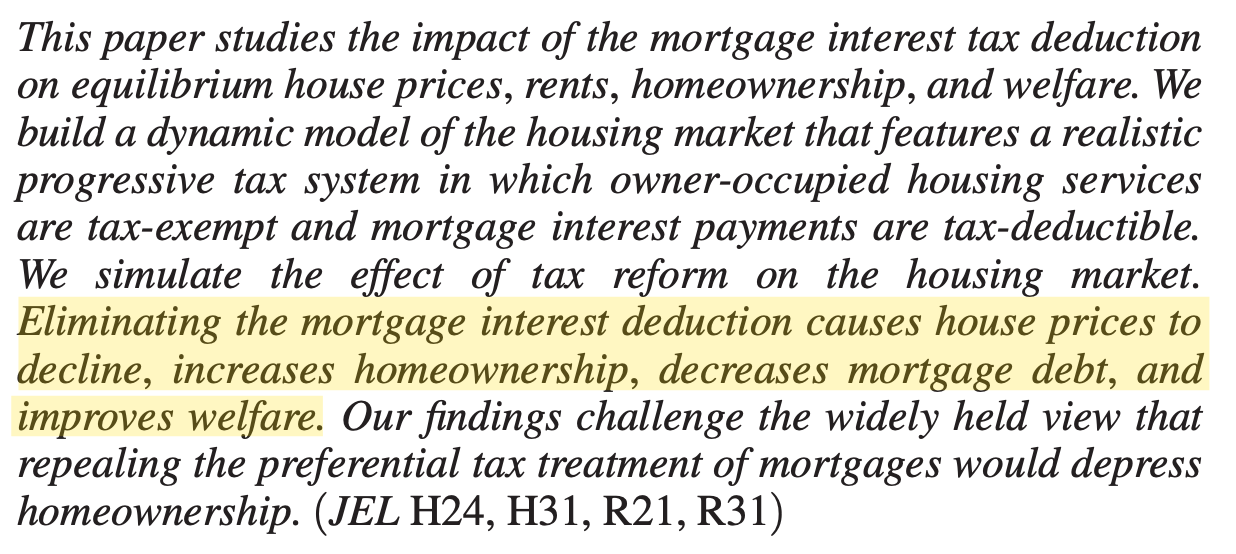

Implications of US Tax Policy for House Prices, Rents, and Homeownership

Sommer and Sullivan (2018)

This paper exploits cross‐state variation in mortgage interest deduction (MID) generosity to show that each additional dollar of tax subsidy raises house prices by $1.30 and reduces mobility by 4 percent relative, illustrating the large equilibrium effects of federal tax policy on housing markets.

Beyond Coven et al. (2024)’s work on property taxes (which we highlighted a previous roundup), there is substantial recent scholarly work that supports (and extends) the above findings:

Hilber & Turner (2014) provided crucial empirical support for the capitalization mechanism central to Sommer and Sullivan’s results — that is, that the MID boosts homeownership only for higher-income households in less regulated housing markets. More importantly, in places with restrictive land-use regulations (inelastic supply), they find an adverse effect on homeownership;

Gruber et al. (2021) conducted perhaps the most comprehensive long-run study of the mortgage interest deduction using Danish administrative data and a major tax reform — and their findings align remarkably well with Sommer and Sullivan (2018); and finally,

Rotberg and Steinberg (2024) provide an important counterargument that nonetheless supports the capitalization mechanism. They argue that renters actually benefit from the MID in general equilibrium because rental supply is relatively inelastic — when homeownership subsidies reduce rental demand, rents fall substantially. While they conclude the MID may improve overall welfare (contrary to Sommer-Sullivan), their model relies on the same capitalization mechanism where subsidies get priced into housing values. The key difference is their focus on rental market incidence rather than homeownership effects.

We feel it is important to highlight the prevailing academic consensus on the impact of both property taxes and other capitalization effects on housing prices as we will likely (eventually) be proposing some policy ideas on this front.

***

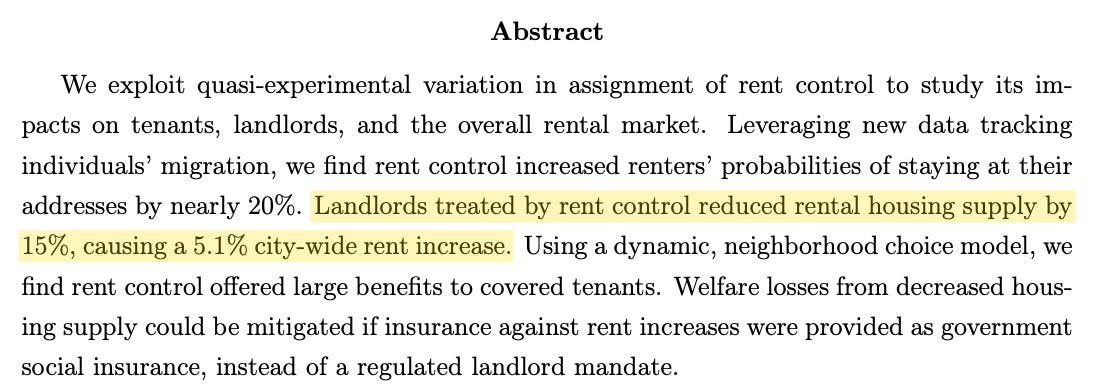

The Effects of Rent Control Expansion on Tenants, Landlords, and Inequality: Evidence from San Francisco

Diamond et al. (2019)

Using a 1994 San Francisco law change, this study demonstrates that while rent control prevents displacement of incumbent renters in the short run, the lost rental housing supply likely drove up market rents in the long run.

The majority of recent research continues to validate Diamond et al.’s core conclusions about rent control’s negative spillover effects: Konstantin Kholodilin’s Meta-Analysis (2024) found that of 16 studies examining rental supply, 12 found negative effects, 3 found no effect, and only one unpublished outlier claimed positive effects. His conclusion was that rent control “results in a number of undesired effects, including, among others, higher rents for uncontrolled units, lower mobility and reduced residential construction.”

ADDITIONAL READING

Evidence suggests U.S. house price/rent ratio, real home prices to decline

J. Scott Davis | Federal Reserve Bank of Dallas

U.S. house prices and rents are generally closely aligned, with only two significant deviations since 1984—in the early 2000s and following the pandemic. […]

Divergence between house prices and rents in the early 2000s and again in the recent period followed a significant increase in real (inflation-adjusted) house prices and stable real rents.

Housing, rents and owner-occupied equivalent rents (the amount of a homeowner’s outlays required to rent equivalent housing), make up 16 percent of headline PCE inflation (the Federal Reserve’s preferred measure) and nearly one-third of Consumer Price Index (CPI) inflation.

House prices do not directly impact inflation. Rather, it’s an indirect effect. The Bureau of Labor Statistics estimates homeowner equivalent rent based on the market rent for similar houses. Thus, the housing component of inflation is closely tied to market rents in the economy. […]

If this divergence between house prices and rents is resolved through larger rent increases, the housing component of inflation would follow suit and rise. […]

The only example of a sustained fall in the house price/rent ratio in the U.S. data was in 2006. Two years after this ratio started declining, there was a global recession and financial crisis that depressed housing and asset prices. It’s unclear whether these patterns from 2006 will hold today.

***

Squeezing Builders Isn’t the Way to Lower Housing Costs

Connor Sen | Bloomberg Opinion

Read between the lines and there’s the implication that the nation’s big developers represent a cartel colluding to generate windfall profits rather than build the homes Americans need. Homebuilder earnings suggest the opposite.

Lennar Corp., the second-largest US homebuilder, offers a window to understanding this dynamic. Lennar has been operating more or less the way the Trump administration would want and is on track to deliver around 80,000 homes this year. Instead of cutting production when demand weakened, the company increased buyer incentives at the expense of profitability.

In response to investor and analyst concerns, Lennar’s management finally relented in the most recent quarter, saying they’d more carefully manage the pace of their production to match demand for the time being.

To use an analogy from another industry, if you want gasoline stations to offer cheaper gasoline, you have to address oil and refining costs.

Building more homes in states including Florida and Texas that are already dealing with pockets of excess supply and falling prices could turn the relatively orderly normalization in their housing markets into something more disorderly.

***

Credit Drove 125 Year of Homeownership Gains

Home Economics

The GI Bill (1944) offered veterans zero-down mortgages at below-market rates. By 1955, it had issued 4.3 million loans totaling $33 billion. The numbers are striking: homeownership surged from 43.5% in 1940 to 55.0% in 1950—an 11.5 percentage point jump in a single decade. It reached 61.9% by 1960 and 62.9% by 1970. […]

Subprime lending and exotic mortgage products pushed homeownership to 69.0% by 2004. “No income, no asset” loans proliferated. Again, policy focused on expanding credit access rather than housing supply. The same tool that had lifted millions into homeownership—easier financing—now became the instrument of its destruction. The collapse revealed the dark side of subsidized demand: home values dropped 26% from 2006 to 2010. Over 4 million families lost homes to foreclosure between 2008 and 2012. Homeownership fell to 63.4% by 2016. […]

Homeownership stabilized around 65%, roughly the mid-1990s level. COVID-19 temporarily pushed rates to 67.9% in Q2 2020 through rock-bottom interest rates. We’ve since returned to 65.0%. […]

The century-long expansion of American homeownership was achieved almost entirely through financial engineering—making it easier to borrow rather than cheaper to build. As that lever reaches its limits, the prospects for maintaining even current ownership rates is growing increasingly uncertain.

REMINDER

If you or someone you know is interested in competing in the Boyd Essay Contest for a chance at $2,500 cash and a Boyd fellowship, the submission window is open through the end of October. Details here:

Boyd Essay Contest: Call for Submissions

We’re looking for essays that answer one simple question: What’s an actionable, outside-the-box solution to America’s housing crisis?