Why do we have fiat money?

Debt claims another empire

On one hand, the answer to this question is very simple. Economists agree that fiat currencies are “best” because they allow the state to intervene more effectively in depressions and other “bad” or extenuating circumstances. But the truth is actually much messier and more complex, historically — and it is an interesting story that is informative for Americans as a warning on how we too could lose our status as the reserve currency.

Much like my article on the USSR the core claim here is that financial sustainability is based on trust in the solvency of a state. But that trust cannot be summoned from thin air and is always ultimately reliant on that actual state’s solvency.

In truth, monetary regimes aren’t really selected — in the sense that a society weighs the costs and benefits of a system from first principles — as much as inherited. The classical gold standard was coherent and a well-functioning system, on its own terms, that put different values at the center than we do today. It was not, as many people think, an archaic or myopic system with no advantages at all, even if its modern proponents often miss the forest for the trees.

I. The Classical Gold Standard and the Theory of Its Own Operation

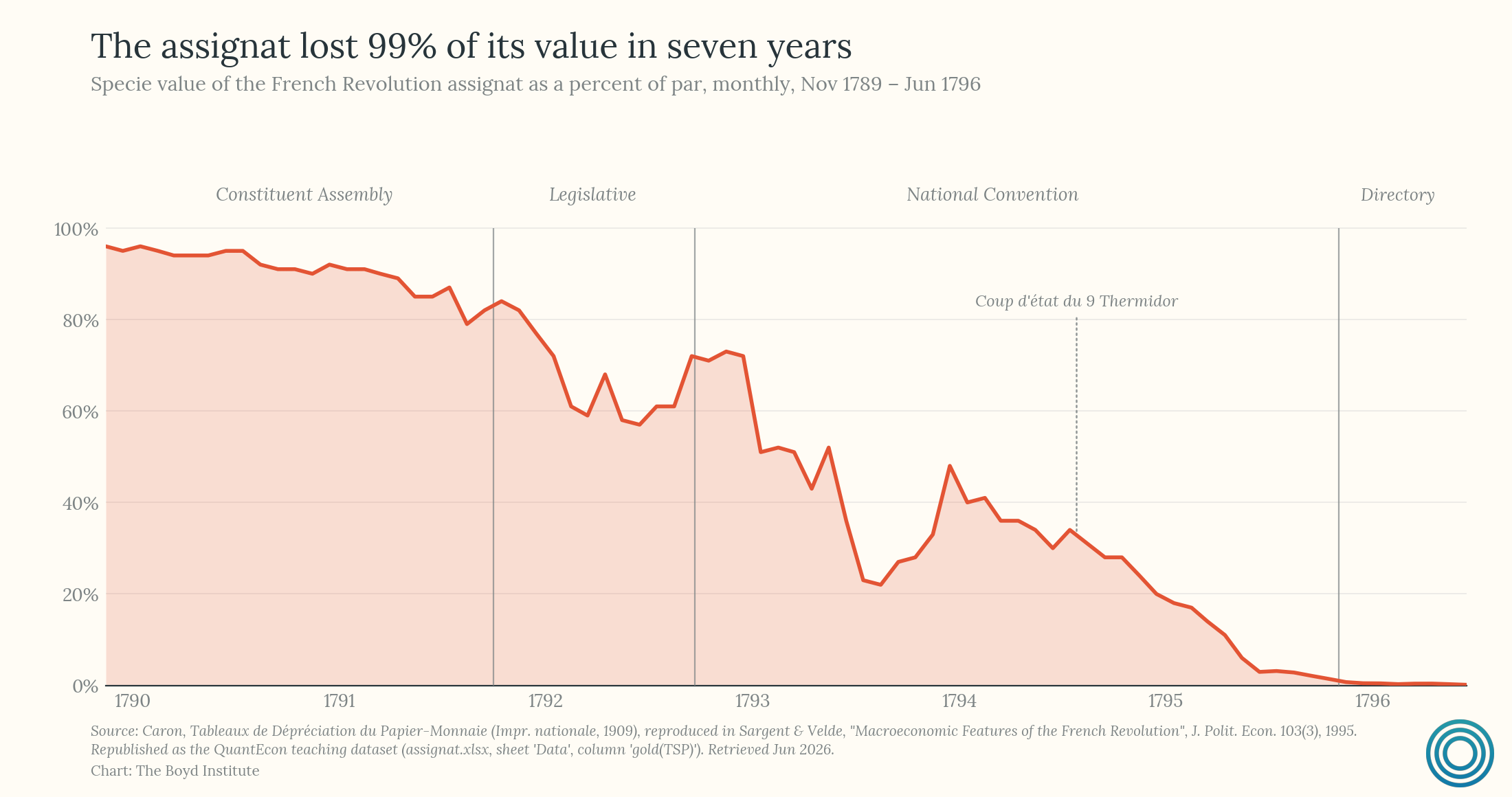

For most of human history, “gold” or other precious metals have acted as the de facto currency in most of Eurasia. However, when people talk about the “Gold Standard” what they are almost always referring to is the “classic” gold standard which emerged in the 18th century and is synonymous with the British Empire. It was largely as a refinement and rationalization of the older pre-existing system and much of it stood in reaction to the excessive money printing of the French Revolutionary regimes.

By the middle of the 19th century, though, it had taken on a life of its own, and the period in which it was hegemonic, roughly 1880 to 1914, combined rapid growth with large and substantially free movements of capital and labor. Perhaps most important to its architects at the time, the world was also defined by extraordinary price stability — and, through its first two decades, by persistent mild deflation on the order of 1-2% a year, as a fast-growing economy outran a money supply tied to a slowly expanding gold stock. Arguably, that era, referred to in France as the Belle Époque, was the most dynamic and innovative in human history.

So how did it actually work?

At the core of this system sat David Hume’s idea of the price-specie-flow mechanism outlined in “Of the Balance of Trade“ (1752) and was actually quite simple.

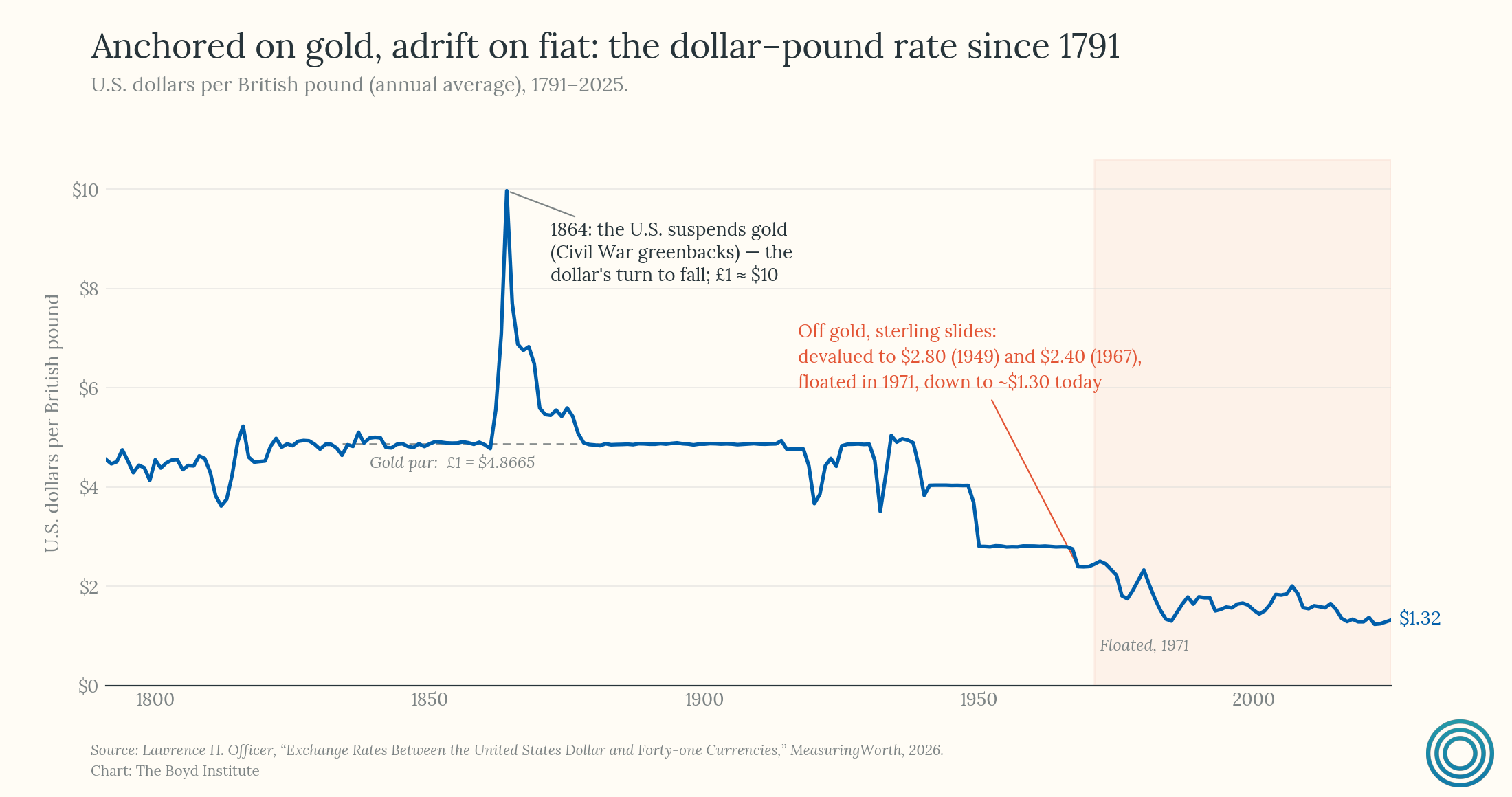

Each participating country defined its currency as a fixed quantity of gold and stood ready to convert notes into metal, and metal into notes, on demand and without limit. Thus the pound was not a thing with value in itself but a claim to a specific weight of gold. Since gold acted as a basis vector of value every currency was effectively pinned to the others and could drift only within the narrow band — the “gold points” — beyond which it became cheaper to ship bullion than to exchange currency.

The primary goal and consequence of the system was monetary discipline. A state could not expand its money supply at will, because anyone holding the surplus paper could present it for gold, and a government that issued beyond its reserves would simply watch them drain away. Money creation was tethered to the gold stock and therefore at the pace of mining1, which because of the economic growth at the time produced mild, persistent deflation.

Trade between nations was similarly rationalized by this system. If a country imported more than it exported, the difference in gold caused its money supply to contract and drive down prices until its goods grew cheap enough to pull demand — and the gold — back again. A surplus country experienced the reverse resulting in an upward pressure on the “real” economic value of their currency. As a result the trade (current) accounts of nations thus effectively balanced themselves, with no intervention.

Hume does a good job of basically describing the system as it was imagined conceptually among contemporaries. The argument turned on a thought experiment:

“Suppose four-fifths of all the money in GREAT BRITAIN to be annihilated in one night... Must not the price of all labour and commodities sink in proportion, and every thing be sold as cheap as they were in those ages? What nation could then dispute with us in any foreign market...? In how little time, therefore, must this bring back the money which we had lost, and raise us to the level of all the neighbouring nations?”

The reverse case completed the symmetry:

“Again, suppose that all the money of GREAT BRITAIN were multiplied fivefold in a night, must not the contrary effect follow? Must not all labour and commodities rise to such an exorbitant height, that no neighbouring nations could afford to buy from us... and our money flow out, till we fall to a level with foreigners...?”

From these cases, Hume drew the general principle and reached for the metaphor that would define the doctrine:

“Now, it is evident, that the same causes, which would correct these exorbitant inequalities, were they to happen miraculously, must prevent their happening in the common course of nature, and must for ever, in all neighbouring nations, preserve money nearly proportionable to the art and industry of each nation. All water, wherever it communicates, remains always at a level.”

And much like water, the goal wasn’t so much to fight the inevitable flow, but to instead channel it productively.

“We need not have recourse to a physical attraction, in order to explain the necessity of this operation. There is a moral attraction, arising from the interests and passions of men, which is full as potent and infallible.”

…

“In short, a government has great reason to preserve with care its people and its manufactures. Its money, it may safely trust to the course of human affairs, without fear or jealousy.”

Thus the system was seen as requiring no discretionary management and admitting of none. Where management was acknowledged, it took the modest form of the “rules of the game” — a phrase popularized by Keynes and later given empirical content by Nurkse (1944) — under which a central bank losing gold was expected to raise its discount rate, and one gaining gold to lower it, thereby reinforcing the automatic adjustment.

Later scholarship has shown that central banks routinely violated the rules of the game without the system breaking down, because what sustained it was not mechanical adjustment but the credibility of the commitment to convertibility itself (Bordo and MacDonald 1997). This adherence functioned as what Bordo and Rockoff (1996) call a “good housekeeping seal of approval,” where states that remained on gold borrowed in international markets at materially lower rates. You can, roughly, analogize this to companies that receive a markup in the market from publishing their financial disclosures in a country like the US rather than China. Because investors knew that countries were financially constrained under the gold standard, they could lend with more faith in being repaid, creating a virtuous and self-fulfilling system.

What the contemporary theory omitted were the two conditions that made gold’s discipline functional. The first was that in London lay both the Bank of England, operating as what Keynes would call the “conductor of the international orchestra,” and also the heart of empire and military power. The second was political. This was a world before mass suffrage and organized labor, in which a government could impose the deflationary adjustment the system demanded.

II. The War and the Liquidation of British Capital

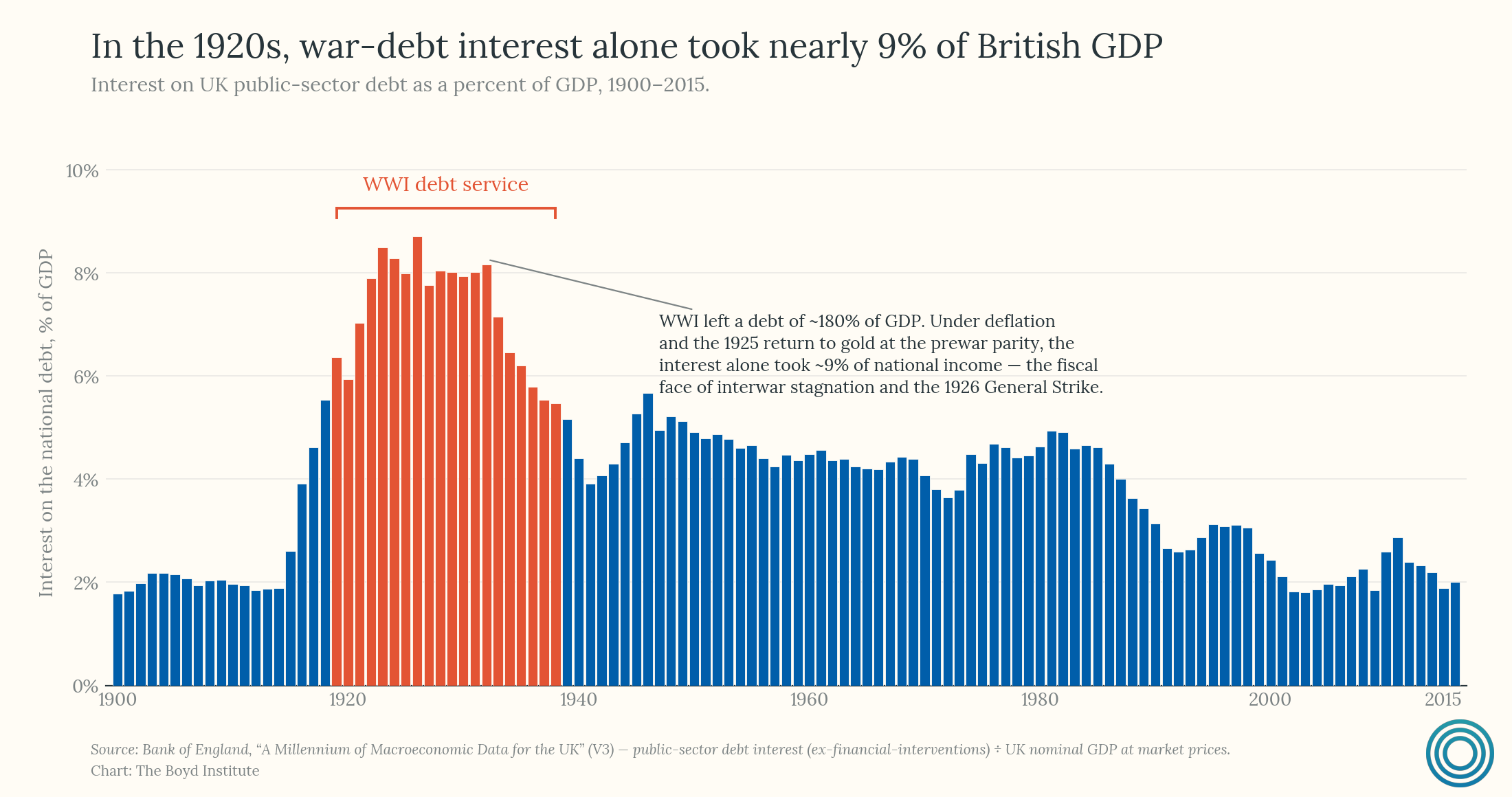

The First World War ended the classical system. Since it required there to be a long run “balance of trade” between countries, states had little room to maneuver in times of crisis. So as British imports soared on the back of war material and exports plunged from workers being sent to the frontlines, the government was forced to find new sources of gold to keep a semblance of a balance. To do this they passed a series of laws designed to force investors to liquidate their foreign capital, converting them into hard currency that could then be taken by the government in exchange for treasuries. Between 1914 and 1918 Britain largely sold off their capital stock and by the conclusion of the fighting was financially exhausted at every level.

As the gold supply passed from London to New York, the fortuitous combination of empire, finance, and military strength passed also.

Part of the bargain had been that the investors who had transformed their capital stock into pounds expected to be able to use them at the pre-war valuation. In fact, the idea that Britain would always honor its debts at their face value, without inflating at all, was emotionally central to the old system. After the Napoleonic wars Britain had been saddled with enormous debts, and rather than inflate them away or negotiate them down honored them in full, running primary surpluses and paying the bonds down over the better part of a century.

In the aftermath of WW1 there was an attempt to repeat this and honor the war debts at their real economic value. To do this the government implemented financial austerity and returned to gold in 1925 at the old exchange rate. However, the political dynamics — namely dominance of London by financial capital — that had made it possible after the Napoleonic wars were no longer in place and the state’s policies were met by the General Strike of 1926, and political outrage. A similar dynamic played out across most of Europe.

Ultimately, it was abandoned again after the Depression because the mechanisms required to balance a metal-based currency — raising interest rates into the deflationary shock — were too politically costly to maintain. This phenomenon, known as Golden Fetters (1992), propagated the downturn internationally and disabled policy response, since no country could ease monetary conditions without losing gold. It is plausible that, given enough time, capital would have regained trust and the international system could have been put back together again, but domestic pressure to bring back consumption overwhelmed the old monetary elite.

Still the widespread belief in the necessity of the gold standard as a check on printing continued to exist, and after the war it was once again put back together. The Bretton Woods system, as it is known, was a gold-exchange standard under which the dollar was convertible to gold, but only by foreign official holders, with other currencies pegged to the dollar.

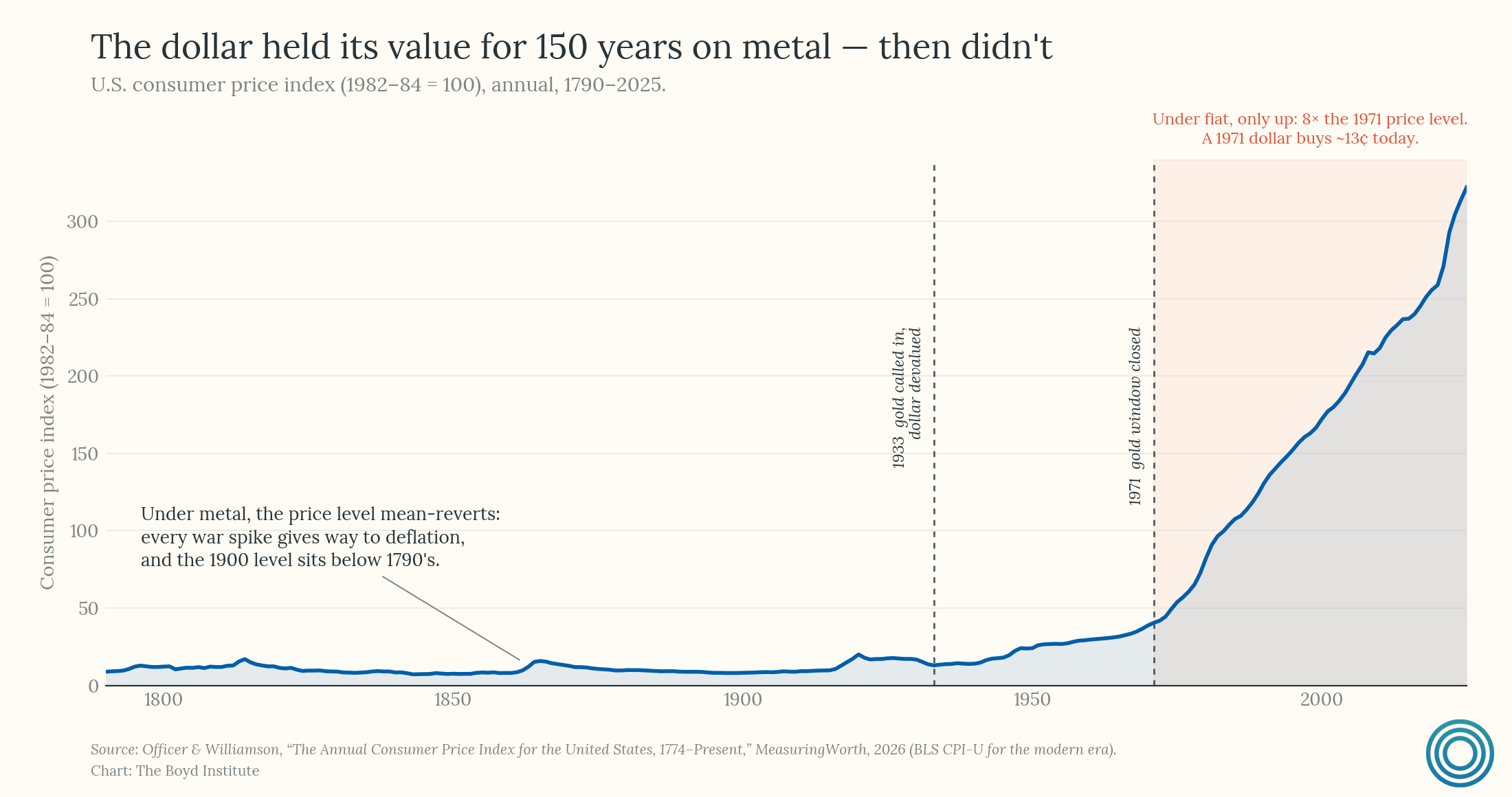

This system was not a true gold standard, for a number of reasons. The most basic is that ordinary citizens were already off it. Already in 1933, Executive Order 6102 had ordered citizens to surrender their gold to the Treasury at $20.67 an ounce to avoid “hoarding.” Under the classical system there was no reason to hoard gold, because holding currency was functionally identical to holding a certificate to a bank vault — but once the state was printing far more money than it could honor with gold, citizens holding bullion on the expectation of inflation risked exposing the central bank to a currency run. You can see this at play in the policy directly. After having compelled Americans to hand in their gold at $20.67, the Gold Reserve Act of 1934 promptly devalued the dollar by roughly 40% against gold, at the direct expense of the people who had just surrendered theirs.2

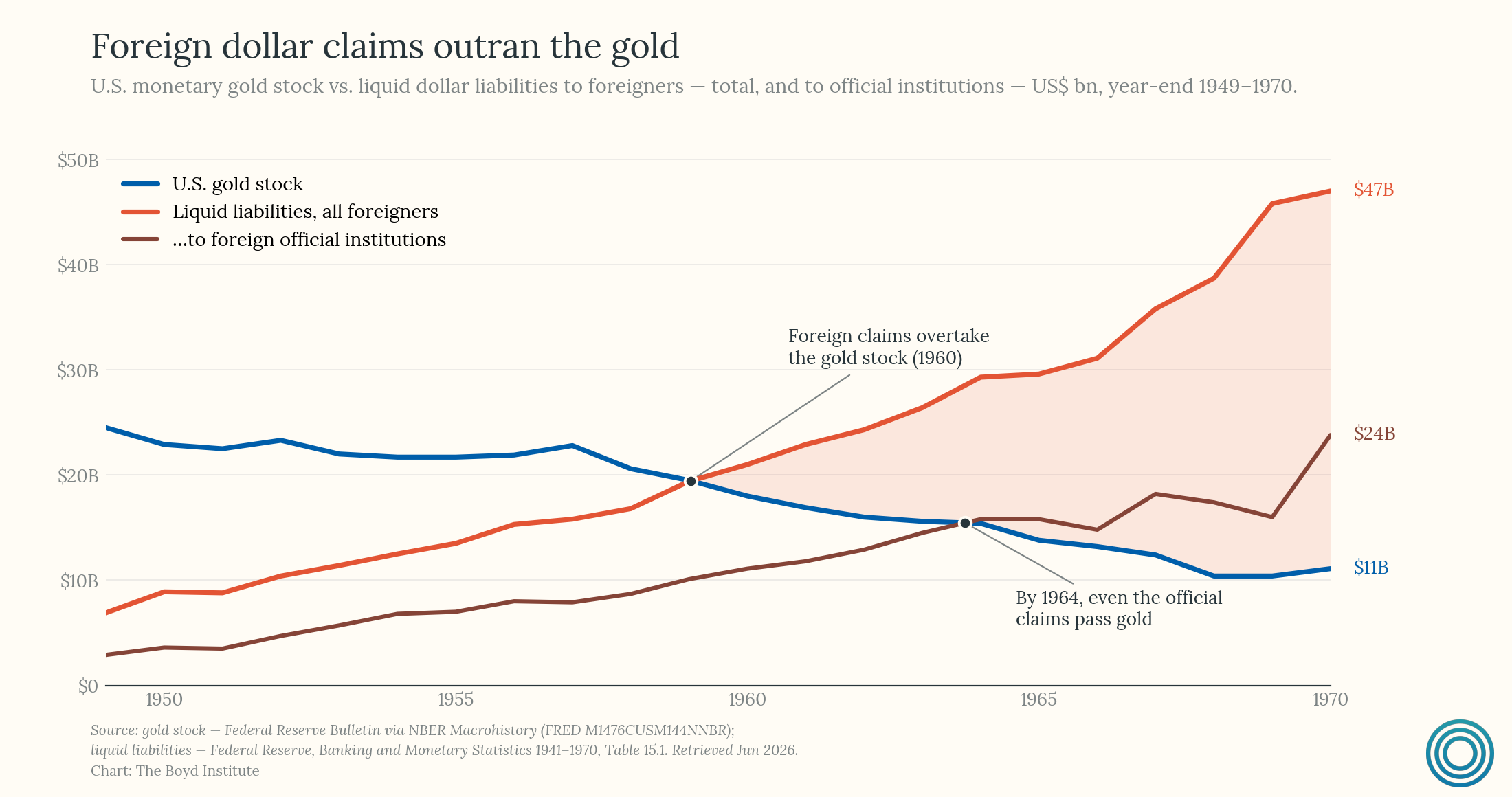

Nor was the promise to foreign governments much sturdier. For the system to work, the United States had to supply the world with dollars by running deficits — and those dollar claims accumulated abroad faster than the gold behind them, further pressuring the credibility of its promise to redeem them.

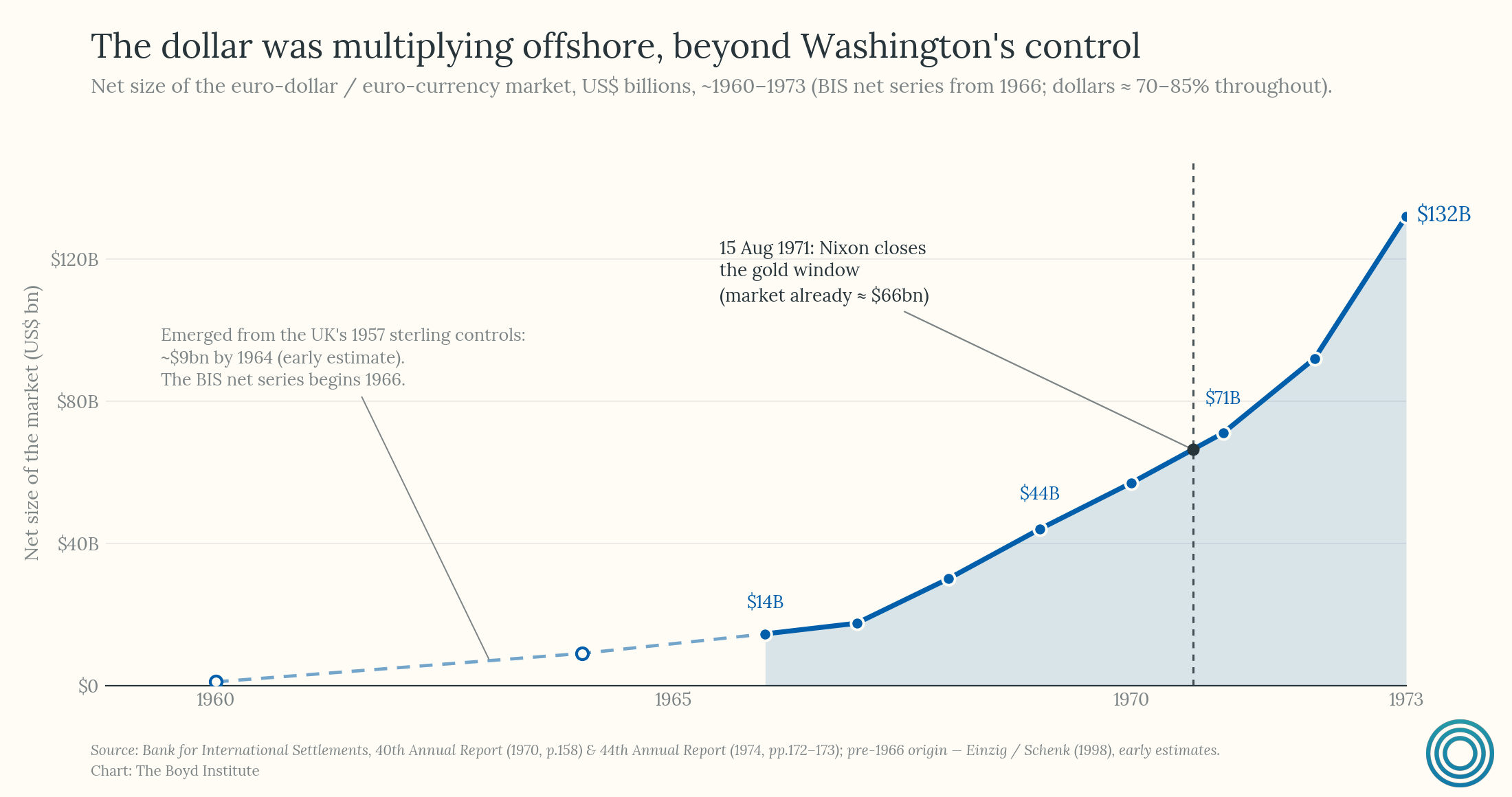

Then there was the eurodollar market. Through the 1950s, the swaths of dollars deposited in banks outside the United States and beyond the reach of American regulation gave rise to a synthetic-dollar market. The eurodollar grew up almost organically, conjured into being by London merchant banks and, fittingly, by Soviet holders who wanted dollars without keeping them in New York.

By the 1960s, France, under de Gaulle and advised by Jacques Rueff, began systematically converting its depreciating dollars into gold and moving the metal to Paris. That, paired with the eurodollar overhang drove Washington, on 15 August 1971 to formally close international convertibility and so begin our current — post–Bretton Woods — system.

III. The Dollar Order and Its Analogues

The question with which this essay began — why we have a fiat money system today — admits of the easy answer offered at the outset: inconvertible money gives the state room to act in depressions and emergencies that a metal standard forecloses. That answer isn't wrong, but it only explains why we tolerate the system, not why we have it.

In truth it was war, and the associated fiscal excesses, that destroyed the gold standard and liquidated the conditions necessary for its survival.

What the gold standard and the dollar order share ultimately what is most informative to us today thought. Both rest on trust, and trust rests, in the end, on solvency. Under gold the link was extremely salient since a state that issued beyond its means watched its reserves disappear. But under a fiat system the dynamic is just as binding, if not as automatic. Ultimately nothing can abolish the underlying bet that the state will honor its commitments. As a result, the dollar's exorbitant privilege is still, at bottom, a belief in its capacity to buy real goods at a stable price, if you destroy that — to fund a war, or a pension system — the dollar’s value goes with it.

We want Boyd’s funding to come from core supporters who want to be part of the conversation. For that to work, we need people like you to step up now, while it’s still early.

Here’s what we’re offering:

Supporter ($10/month) and (Annual $120/year): Access to our private Discord community and a quarterly call, where you can talk directly with us and other members

Founding Partner ($1,000/year): Everything above, plus a monthly one-on-one call with us.

The Boyd Institute is a 501(c)(3). All contributions are tax-deductible. If you’re able to give through a Donor Advised Fund or make a direct donation beyond a subscription, it would meaningfully extend what we can do. Reach out to [email protected].

Which is to say the system's vaunted discipline was, in the end, a matter of geology. So long as growth outran the mines, prices fell, and they did for a generation. But when the Witwatersrand opened in 1886 and the Klondike followed a decade later, and the new cyanide process wrung more metal from every ton of ore, the gold stock surged and the same disciplined system tipped quietly into mild inflation right up to the war. South Africa did what no central banker was permitted to.

Private citizens would not legally own monetary gold again until 1974.

Great work!

I used to look down on the gold standard. Conventional economic wisdom, as Banks discussed here, holds that Gold was more a liability than an asset; most countries didn't exit the great depression until they ditched the gold standard.

Still, its amazing that humans decided to peg their currencies, essentially informational mechanisms, against gold atoms, the “waste” product of prehistoric supernovae.

Of course, gold was chosen because of its rarity; unlike many elements that course be fused in stellar furnases, gold had to wait for rare supernovae events.

Gold also is fairly inert. It doesn't rust or corrode, making it a permanent store of value.

In this new, debt-laden, inflationary world, it might be time to revisit the gold standard, our at least the idea of pegging currency to something scarce.

Perhaps the 21st century equivalent would be bitcoin; the encoded output of energy consumption.

A very useful article. The gold standard was terrible, but no one has come up with a replacement mechanism to restrain the political urge to do everything.

Permanent familial bonds can be terrible too, so we've largely done away with them without coming up with a replacement mechanism for raising children. Irrelevant to the discussion, I was just reminded.