Debt-and-Deficits Dictator for a Day

What real reform would look like (if politics were no object

Our debt and deficit sprint has, so far, mostly stayed on the descriptive side of the ledger. What we haven’t done yet is get prescriptive. That’s been deliberate: description is a necessary precondition for any serious conversation about solutions, and skipping past it is how so much deficit commentary fails to address the main drivers of the federal debt. But at some point, the descriptive work has to give way to the harder question: what would you actually do about it?

The honest answer is that almost nothing that would meaningfully bend the debt curve is politically survivable in anything like its effective form. This isn’t a failure of will so much as a structural feature of democratic politics. The costs of serious reform are concentrated and immediate: a farmer loses a subsidy check, a retiree sees a smaller cost-of-living adjustment, a community loses the economic activity generated by an obsolete military base. The benefits are diffuse and delayed: an averted, unseen fiscal crisis, more fiscal room to respond to the next emergency, modestly lower interest rates a decade hence that no voter will ever trace back to the vote that produced them.

Concentrated, immediate losses generate organized, well-funded opposition; diffuse, delayed gains generate approximately no political constituency at all. Layer onto that the fact that politicians operate on the timescale of the next election cycle: they bear the short-term electoral risk of deficit reduction without ever collecting the reward for its long-term benefits.

No wonder our debt-to-GDP ratio has grown on autopilot for the past half-century and now sits at its highest level since World War II. If we want to solve our debt crisis, we must find a way to override the political incentives that produced it and make fiscal responsibility electorally viable — ideally, electorally beneficial.

One caveat before the cutting starts. Some readers will object that the composition of what follows — heavy on spending restraint, light on rate increases — smuggles in a contested premise, namely that consolidating through the spending side is less damaging to growth than consolidating through taxes. If you would like a deep dive into the impacts of spending vs. tax-based austerity, I would recommend our recent article on austerity.

Assume No Political Constraints

An old joke goes as follows: an engineer and an economist fall into a hole in the ground. The engineer can’t figure out how to escape, but the economist says, “Easy, just assume a ladder.” For the rest of this piece, I’ll do the equivalent of assuming a ladder out by acting as if I’ve been made dictator for a day. In this exercise, I have unlimited authority to raise taxes, cut spending, and pass legislation with no need to win a vote, survive a primary, or ever face the electorate again.

This isn’t an endorsement of dictatorship as a policy-making method; it’s a deliberate thought experiment. If we strip away the political constraints entirely and ask what a purely technocratic fix would look like, we get a useful benchmark. The gap between that benchmark and what’s actually achievable is itself the measure of how hard this problem is.

First Order of Business: Eliminate Corporate and Agricultural Subsidies

As a staunch capitalist, I believe that firms either don’t need subsidies (because they would survive under market competition) or don’t deserve them (because they would not survive under market competition). Therefore, my first act as fiscal dictator is to zero out the $181 billion the federal government spends on corporate welfare each year.

Second Order: Reform and Cut Entitlements

It’s popular (if politically difficult) to get big business off Uncle Sam’s payroll, but it comes nowhere close to closing the gap between spending and tax receipts. The real money is in entitlements, so the second order of business targets the three largest line items in the federal budget directly: Social Security, Medicare, and Medicaid, which together account for close to half of all federal spending and are the single largest driver of the long-run debt trajectory.

Social Security

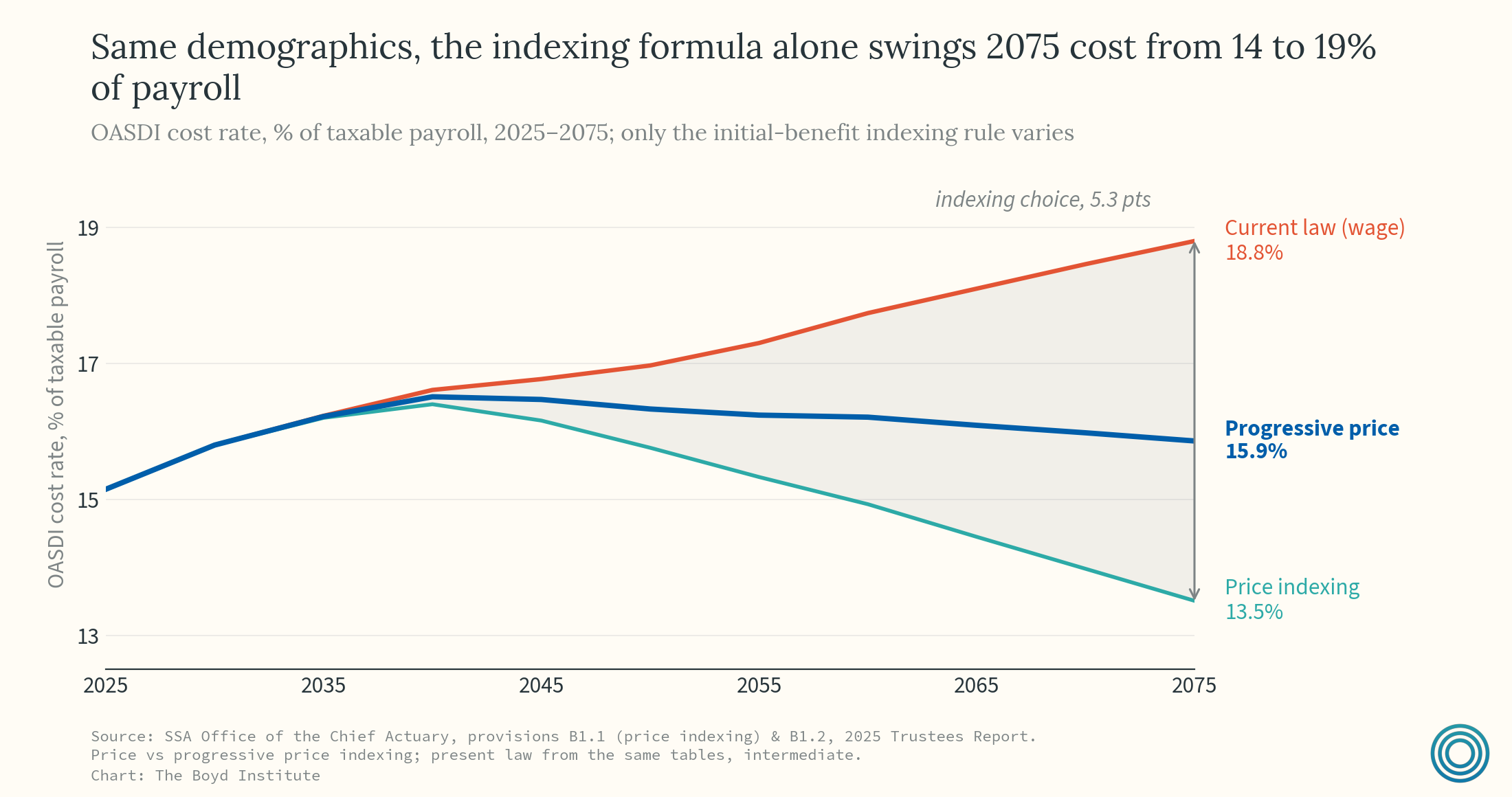

Three changes, layered together, do most of the work — and it’s worth being clear about which one is the workhorse. As the decomposition in our ground-truths piece showed, the indexing mechanics swamp the demographic lever: how initial benefits grow matters far more to the long-run cost curve than when people start collecting them.

So lead with the formula.

First, then, switch the initial benefit formula from wage indexing to a progressive price index: a blend that indexes benefits for lower earners to wage growth (as today) but indexes benefits for higher earners to the slower-growing CPI instead. Wages tend to outpace prices over time, so this alone bends the long-run cost curve substantially while leaving benefits for the bottom of the income distribution untouched. This is the heavy lifting.

Second — the minor knob, but still worth turning — raise the retirement age and index it to life expectancy going forward, so the program doesn’t have to be re-litigated every time Americans gain another few years of life. Social Security’s full retirement age was set when a 65-year-old had a fraction of the remaining lifespan they have today; letting the age drift upward automatically, the same way we’d want any other actuarial assumption to update, removes one recurring political fight from the calendar even if it does comparatively little of the fiscal work.

Third, layer in means testing at the top: high-lifetime-earners see their benefits taper down enough so that Social Security stops functioning as a middle-and-upper-class annuity subsidized by everyone else’s payroll taxes. None of this touches the program’s core promise for low- and middle-income retirees; it asks the people least dependent on the benefit to shoulder more of the adjustment.

Medicare and Medicaid

The core problem with these programs is that they are open-ended, cost-based reimbursements, which means the incentive on both sides of the transaction points toward more spending, not better outcomes. For Medicaid — the one program actually administered by the states — a block grant flips that dynamic: it caps the federal contribution and pushes states to genuinely manage costs and quality, rather than passing every marginal expense straight through to the federal balance sheet under the open-ended matching formula.

Medicare presents the same underlying pathology in a different institutional wrapper. Because the program is run directly by the federal government, there is no state intermediary to discipline. Moreover, while Medicare Advantage has already moved a majority of beneficiaries into capitated private plans, the federal contribution to those plans remains benchmarked to costs in traditional Medicare, so the open-ended spending commitment persists beneath the capitated surface. The analog to a block grant here is premium support: the federal government makes a fixed, defined contribution toward each beneficiary’s coverage; plans bid competitively against that amount; and beneficiaries who want richer coverage pay the difference. That converts Medicare from an open-ended entitlement into a defined contribution, putting plans — and to a degree beneficiaries — on the hook for marginal costs rather than the federal balance sheet.

Third Order: Tax Shift

Replace the existing income tax system with an X-tax. The X-tax, developed by economist David Bradford, is a form of progressive consumption tax implemented through two linked pieces: a flat-rate cash-flow tax on businesses (revenue minus wages and investment) and a progressive wage tax on individuals’ labor income (with exemptions for income from savings and investments).

Because investment is expensed immediately rather than depreciated over years, and because the tax falls on consumption rather than on the return to saving and investment, the code stops penalizing the choice to save and invest relative to the choice to consume. Because the business side has few deductions to fight over, most of the corporate tax code’s lobbying surface — the accelerated depreciation schedules, the interest deductions, the industry-specific credits — disappears along with the subsidies from the first order of business.

The individual side keeps the progressivity that makes an income tax politically and morally defensible; you’re not moving to a flat consumption tax, you’re moving to one with graduated rates on wages. The appeal of the X-tax is efficiency without regressivity: a flatter, simpler, more growth-friendly structure that doesn’t ask low earners to shoulder proportionally more of the burden.

Fourth Order: Pro-Growth Reforms

Eliminate all trade protections (except those for national security), massively expand migration, and slash regulatory bloat. None of these are deficit-reduction measures in the narrow accounting sense: they don’t show up as a line item cut or a new revenue source.

But debt sustainability isn’t just a function of the numerator (how much we owe); it’s a function of the denominator too (how fast the economy underlying our capacity to service that debt is growing). Tariffs raise consumer prices and invite retaliation while undermining the productivity gains from specialization. A more open migration system expands the labor force and the tax base at a moment when an aging native-born population is already straining the ratio of workers to retirees.1

And regulatory reform lowers the cost of building things — homes, energy infrastructure, factories — which is disinflationary and growth-enhancing in a way that shows up, eventually, in higher tax revenue without a single rate increase.

Final Order: Fiscal Rules

I am only dictator for a day, which means the entire point of this exercise evaporates the moment I hand power back. Cuts, reforms, and a new tax code mean nothing if the next Congress reverses them within a term.

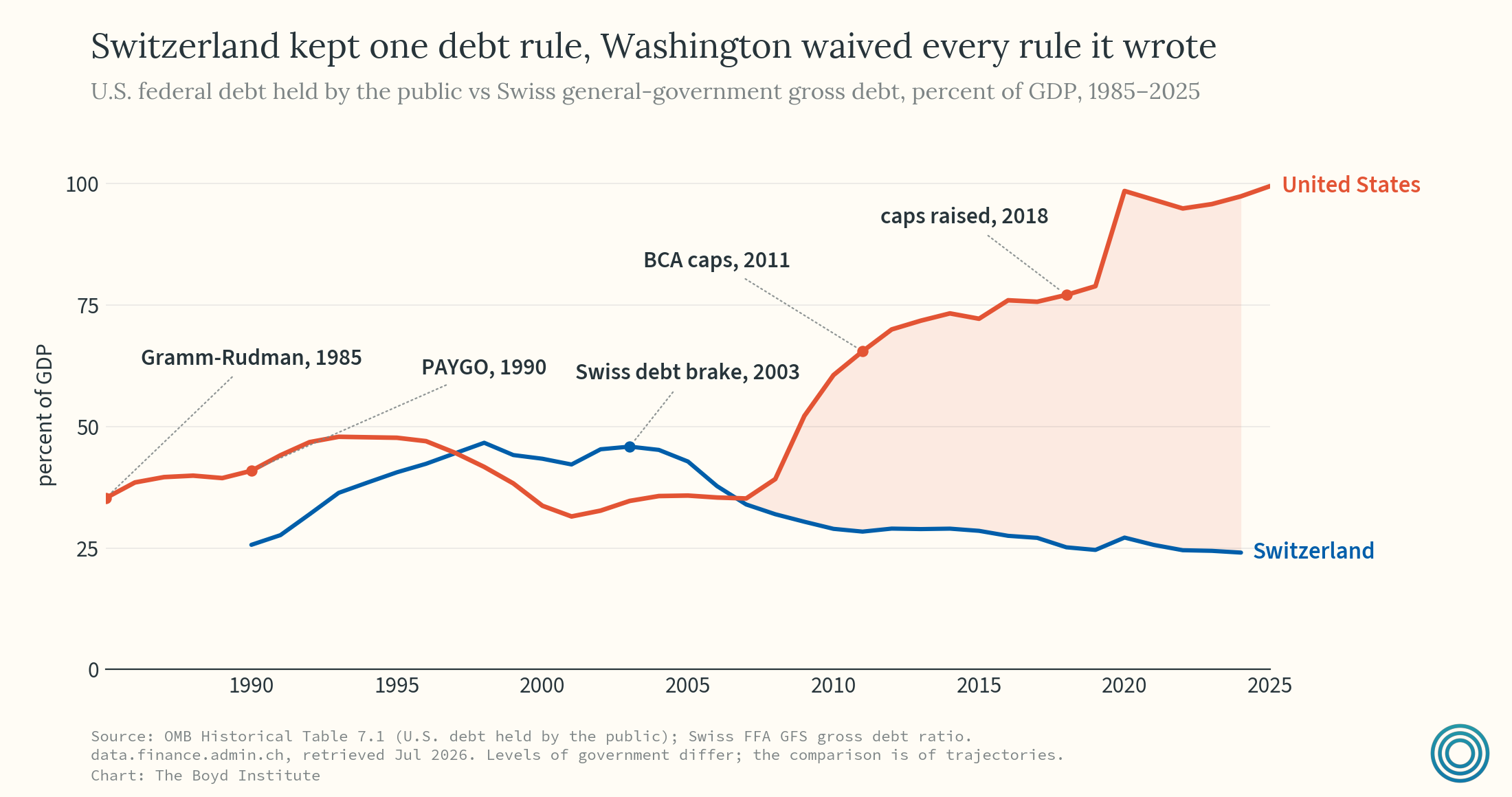

The American track record here is a graveyard of paper promises. PAYGO has been waived whenever it threatened to bind. The Budget Control Act’s spending caps were blown past by bipartisan agreement, repeatedly. Automatic cuts get switched off more or less every time they actually bite. A statutory fiscal rule is exactly as durable as the next majority’s willingness to keep it, which is to say: not durable at all. This is the trap the opening of this piece described, and a clever statute doesn’t escape it: it just relocates it.

The model that has escaped it is Switzerland’s debt brake, which I covered in detail in our eight-countries piece, so I’ll only sketch the mechanics here: a cyclically adjusted ceiling on expenditure — deficits allowed below trend, surpluses required above it — with deviations tracked in a compensation account that must be worked off through lower future ceilings, automatically, with no committee empowered to waive the correction. In force since 2003, it has driven Swiss federal net debt down to roughly 16 percent of GDP, among the lowest in the developed world, with some of the cheapest sovereign borrowing anywhere.

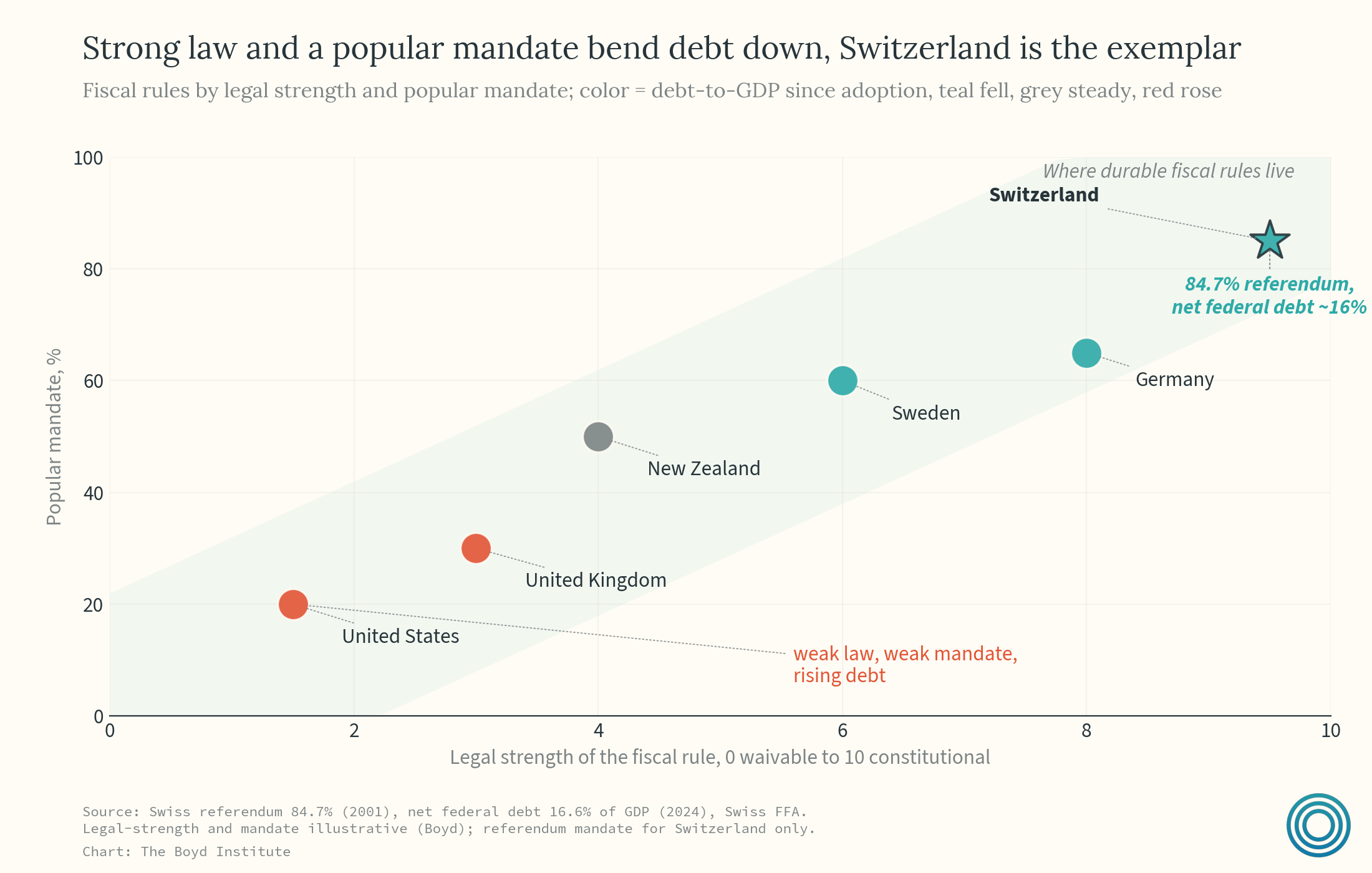

But here’s the thing to take from the Swiss case (and the point the eight-countries piece made that bears repeating): the compensation account is clever engineering, and it is not why the rule holds. The rule holds because it’s written into the Swiss constitution, and because it got there by referendum with roughly 85 percent of the vote.

A politician who wants to bust the Swiss brake isn’t quietly amending a statute; he’s asking voters to repeal something they overwhelmingly and personally ratified. The bindingness is in the mandate, not the formula.

So the last act of my dictatorship is to entrench the rule constitutionally by decree: a cyclically adjusted expenditure ceiling, an automatic compensation account, and a supermajority — not simple-majority — exception clause for genuine emergencies. I’m dictator for a day; I don’t need a referendum, and within the four corners of the thought experiment, decreeing the amendment is enough.

But notice what the decree cannot manufacture. The Swiss brake doesn’t hold because the text happens to sit in the constitution; it holds because 85 percent of voters put it there themselves. A rule imposed by fiat has the words without the mandate, and the mandate is the enforcement: it’s what turns repeal from a routine act of amending a statute into an act of defying the public. That’s the ingredient no dictator can decree, and it’s what the opening of this piece said we were missing: a constituency for solvency. The real-world version of this program has to be built the hard way by persuading an electorate to ratify the constraint, converting the diffuse, delayed benefit of fiscal responsibility into an explicit public commitment that politicians defy at their peril.

Which is the honest place to end the exercise. The economist in the joke assumes a ladder; the dictator in this one can decree everything except the thing that matters most. The real ladder out of the hole is a popular mandate for a binding rule and unlike the assumed one, it has actually been built.

How big that gain is depends on who comes: a system weighted toward working-age, higher-earning migrants is a clear net contributor, while large low-skill inflows can run a near-term fiscal drain at the state and local level — so selecting for skills and age captures most of the upside.