Weekly Roundup #7

Housing | California Forever, urban redevelopment constraints, an exciting ConTech startup, and more

EXECUTIVE SUMMARY

Welcome back to Boyd’s weekly roundup series. This was a busy week as we had two great Substack Live conversations — be on the lookout for several more over the course of next few weeks. Guests we currently have booked include Jess Remington, Cameron Murray, Moses Sternstein, Jeff Fong, and a few others.

This week’s roundup includes:

Newsflow:

Pulte Homes reported better earnings than peers due to limited exposure to the entry-level single-family segment

The Fannie Mae CEO stepped down as privatization talks carry on

A revitalized effort behind the billionaire-backed new city buildout in California

Academic research:

The dynamics of urban redevelopment

The impact of shortening permitting approval times in Los Angeles

Additional reading:

Wells Fargo on whether lower rates will revive the housing market

Lance Lambert from ResiClub on a ConTech startup that hopes to streamline housing construction productivity

Catch Peter and Will’s debrief session Monday (10/27) where they’ll be discussing the roundup contents as well as engaging with comments/Q&A. Additionally, if you haven’t already, do check out this past week’s posts:

COMMUNITY POLL

This week we’re asking about a topic that we touched on in each of our last two live interviews: causes of the Great Financial Crisis of 2008/09. It of course happened as the result of a confluence of factors, but we want to know which one readers think was the most impactful.

NEWSFLOW

WSJ: Analysts say Pulte Homes, compared with other builders, has been better able to maintain pricing and margins despite the slowdown. The company has less exposure to entry-level homes, which have seen particularly slow sales. Some builders have had to offer increasingly generous incentives to offload their rising inventory of these homes before the end of their fiscal years. “We are encouraged to see that interest rates have moved lower, but continue to monitor buyer demand that has been impacted by weaker consumer confidence and ongoing affordability challenges,” said CEO Ryan Marshall.

WSJ: The Fannie Mae CEO stepped down as the Trump administration consideres selling stock in Fannie and Freddie, which bundle and sell mortages and have been under government conservatorship since the ‘08 financial crisis. It is unclear whether the companies would remain under government conservatorship if the White House went ahead with a public offering. In March, the Federal Housing Finance Agency, which regulates Freddie and Fannie, removed eight members of Fannie’s board and added four new ones, including FHFA director Bill Pulte as chair.

Gizmodo: The California Forever project, which was originally announced in 2023 and is backed by a variety of well-known Silicon Valley billionaires, seeks to create a brand new city in northern California. Last year it was pulled from consideration after ongoing local backlash, but it may have new life now, as its backers submitted a formal application for what it calls the Suisan Expansion Project. The plan would be to annex ~22,000 acres of land by expanding the city of Suisan, which is located adjacent to the massive Solano County land bundles previously purchased by the development group. The group aspires to turn the new city into “An industry and technology zone, and bringing advanced manufacturing jobs to Solano County,” with the expansion including a Solano Foundry, a new downtown, and over a 40-year build out with walkable neighborhoods and 175,000+ homes.

ACADEMIC RESEARCH

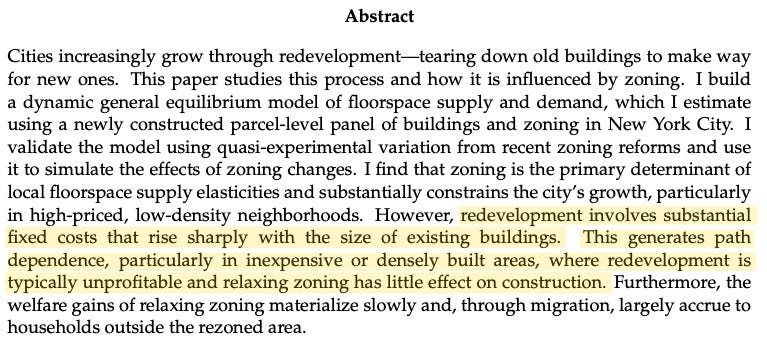

Can We Rebuild a City? The Dynamics of Urban Redevelopment

Rollet (2025)

Arpit Gupta brought this paper to our attention last week, and we found it to be important in that it fundamentally challenges the assumption that zoning reform alone can unlock housing supply, given that urban redevelopment faces structural economic constraints. It shows that the neighborhoods with the infrastructure, transit access, and urban form that are most suitable for “missing middle” housing cannot produce more of it merely through market mechanisms.

On the one hand, this would be bearish for the prospects of a comeback of the missing middle — duplexes, four-plexes, cottage courts, or moderate-density typologies once common in American cities — but only insofar as its comeback entails solely urban infill.

On the other hand, the study finds that zoning is the primary constraint in high-priced, low-density NYC neighborhoods like Western Brooklyn and Northern Queens. These areas — expensive single-family neighborhoods with good amenities — would see 39% of all additional floorspace from citywide upzoning despite representing only 10% of upzoned land. This is precisely where the “missing middle” can actually be built. But, evidently, because of exclusionary zoning, it hasn’t been.

Furthermore, Rollet (2025) finds that time horizons matter enormously — the benefits of zoning reform accumulate over 40+ years, meaning today’s reforms primarily benefit future residents rather than current ones. Perhaps this explains the NIMBY instinct to some extent?

***

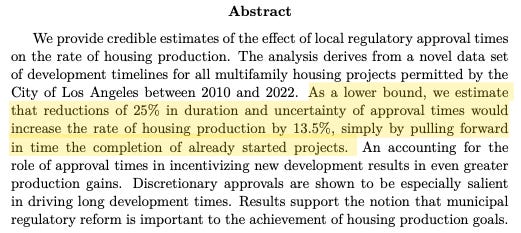

Development Approval Times and New Housing Supply: Evidence from Los Angeles

Gabriel and Kung (2025)

Joshua Coven mentioned this study in our conversation, and it paints a pretty clear picture that in LA specifically, the arduous permitting approval process — on its own — is a meaningful impediment to the construction and delivery of multifamily supply.

It provides the first empirical proof (using comprehensive administrative data) that lengthy permitting processes directly suppress housing production in major cities. Unlike theoretical arguments or anecdotal evidence, the authors tracked every single multifamily housing project permitted in Los Angeles from 2010-2022, creating an unprecedented dataset that definitively quantifies how bureaucratic timelines strangle supply.

This strongly supports the implementation of permitting shot clocks, a pillar of the YIMBY policy prescription. Among the recently-enacted legislation in California, two such measures were passed:

AB 1308: 10-day shot clock for final inspections on projects of 10 units or fewer

AB 253: 30-day shot clock allowing third-party permit review if local government doesn’t complete review

California (specifically Los Angeles) represents the extreme case of regulatory sclerosis, but the pattern is widespread. Multifamily construction timelines have nearly doubled nationwide since 2000, rising from 9.8 months to 17.0 months by 2022.

ADDITIONAL READING

Will Lower Rates Revive the Housing Market?

Wells Fargo Economics Team

So will lower interest rates inject more energy into the residential sector? A lower fed funds rate should strengthen the macroeconomic backdrop and add support to housing demand. In our view, however, mortgage rates are likely to remain within a range of 6.2%-6.4% over the next few years as fiscal pressures and higher inflation expectations prevent a material decline in long-term rates. Although affordability conditions may improve around the margins, high mortgage rates and elevated home prices will likely continue to limit activity and prevent a full-fledged recovery.

[…]

Reductions to the funds rate are positive for the residential market in that they should help shore up the labor market, promote stronger income growth and boost consumer confidence, thereby supporting housing demand. In addition to affordability constraints, we believe that soft labor market fundamentals have become a strong headwind to home buying. The unemployment rate, though not skyrocketing, has drifted higher in recent months. Even though layoffs do not appear to be accelerating, the sluggish hiring environment is extending the time it takes for unemployed workers to find a new job and dimming consumer perceptions of the labor market. All told, these factors are weighing on real income growth and diminishing consumers’ expectations for income growth in the year ahead.

[…]

Unfortunately, we are skeptical that a lower fed funds rate will lead to a significant easing in terms of mortgage rates. Mortgage rates do not typically move in lockstep with the federal funds rate. Instead, mortgage rates tend to follow the 10-year Treasury yield, which is influenced by fiscal policy as well as long-run interest rate and inflation expectations.

[…]

Despite recent weakness, we expect existing annual home price appreciation to remain positive in the years ahead alongside limited supply, a modestly better pace of sales from slightly lower financing costs and a stronger macroeconomic environment. In terms of the new home market, inventory remains elevated relative to the pace of sales, which means builders will likely continue to reduce the pace of construction and offer price incentives to support demand. Consequently, we anticipate median new home prices to contract modestly this year with a better balance between supply and demand, leading to firmer price appreciation in 2026 and 2027.

***

The product is the factory: Cuby’s radical shift in how homes get built

ResiClub | Lance Lambert

Residential construction remains heavily reliant on scarce skilled labor, with productivity that has lagged other sectors for decades. Cuby’s co-founder, Aleksandr Gampel, puts it bluntly: “Construction is the world’s most broken industry… It’s the only industry that hasn’t industrialized. It’s the only industry that hasn’t automated.” He argues that reducing skilled labor hours; often a dominant cost component, is the most reliable way to bring down total build costs.

Cuby’s approach, inspired by the Toyota Production System, is to atomize assembly into granular and discrete checks such that four unskilled workers can progress from foundation through finishes in roughly 45 to 60 days. Each step is verified before the next begins, with standardized tools and site setups intended to reduce variability. The company’s ambition is a turnkey, move‑in‑ready product assembled with less dependence on specialty subcontractors.

[…]

Cuby frames cost parity with incumbent builders as the threshold for adoption. The company targets a self‑cost in the $100–$110 per‑square‑foot range, contending that it can match or undercut traditional delivery while offering tighter process control and speed. Management characterizes the potential as ~20% lower costs than top “product” builders on comparable specifications.

The argument is straightforward: compress schedules, standardize tasks, and cut idle time between trades to reduce both direct labor hours and carrying costs. The kits and SOPs are engineered to comply with the International Building Code (IBC), with local calibrations for climate and jurisdictional requirements accounted for in the MMF’s service radius.

[…]

One of the key components that enable Cuby’s capital-efficiency while utilizing high-performance materials is through a vertical integration of all systems. Procurement, manufacturing, building, even minutia such as janitorial services are standardized processes within Cuby’s operating ecosystem.

[…]

Earlier attempts often shipped finished volumetric modules from distant plants or invested heavily in centralized off‑site fabrication. Cuby’s differentiation is its decentralized, near‑site production with on‑site assembly of standardized kits. By keeping factories smaller and geographically closer, the company hopes to avoid the utilization whiplash that plagued larger facilities when orders dipped.

REMINDER

If you or someone you know is interested in competing in the Boyd Essay Contest for a chance at $2,500 cash and a Boyd fellowship, the submission window is open through the end of October. Less than a week left!!!

Details here:

Boyd Essay Contest: Call for Submissions

Submissions are now open for the Boyd Institute Housing Essay Contest! We’re looking for essays that answer one simple question: What’s an actionable, outside-the-box solution to America’s housing crisis?